Mortgage Rates Hit 7-Month High — What It Means for US Homebuyers and Investors in 2026 is now one of the most searched financial topics in the United States as rising borrowing costs reshape the housing market, investor behavior, and affordability across the country. With 30-year fixed mortgage rates recently climbing above 7% for the first time in seven months, both buyers and investors are facing a dramatically different landscape compared to the low-rate environment of previous years.

This surge is not happening in isolation. It reflects broader economic forces, including persistent inflation concerns, strong labor market data, and expectations that the Federal Reserve will keep interest rates elevated longer than previously anticipated. As a result, mortgage rates have followed Treasury yields upward, creating new challenges—and opportunities—for anyone involved in real estate.

Mortgage Rates Hit 7-Month High: Why Mortgage Rates Are Rising Again in 2026

The primary driver behind the recent spike in mortgage rates is the continued strength of the US economy, combined with inflation pressures that have not fully subsided. Even though inflation has cooled compared to its peak, it remains above the Federal Reserve’s target of 2%, forcing policymakers to maintain a cautious stance.

Another major factor is the rise in the 10-year Treasury yield, which directly influences mortgage rates. In early 2026, yields moved closer to 4.5%–4.8%, pushing mortgage rates above 7%. Investors are demanding higher returns due to inflation risks and uncertainty around future rate cuts.

Additionally, global factors such as geopolitical tensions, oil price fluctuations, and strong consumer spending in the US have contributed to market volatility. These elements collectively signal that borrowing costs may remain elevated for a longer period than many expected at the start of the year.

Current Mortgage Rate Data and Market Trends

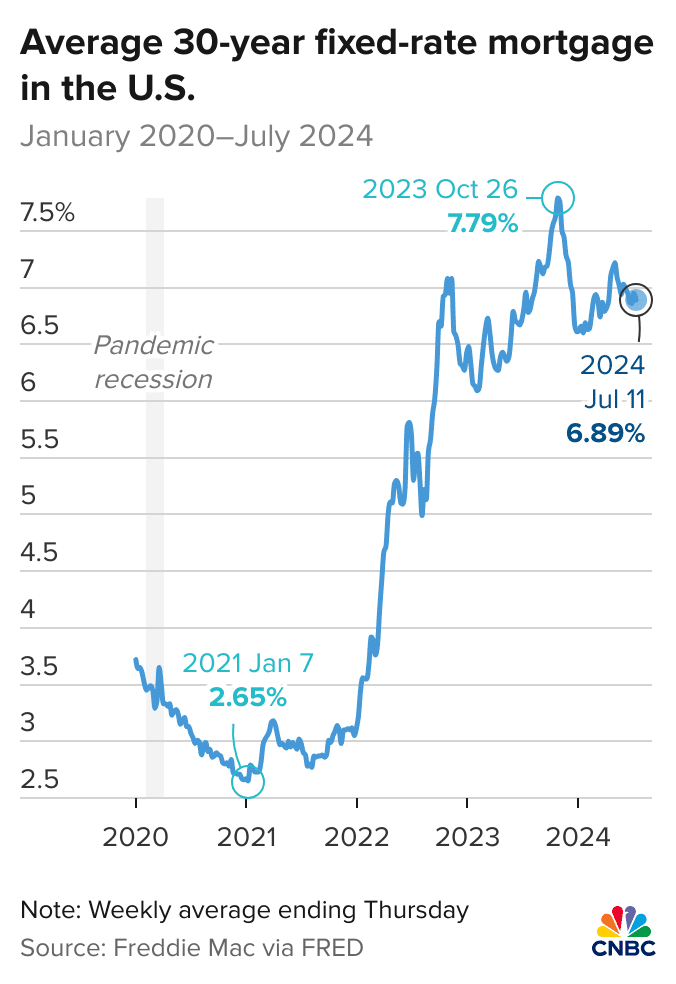

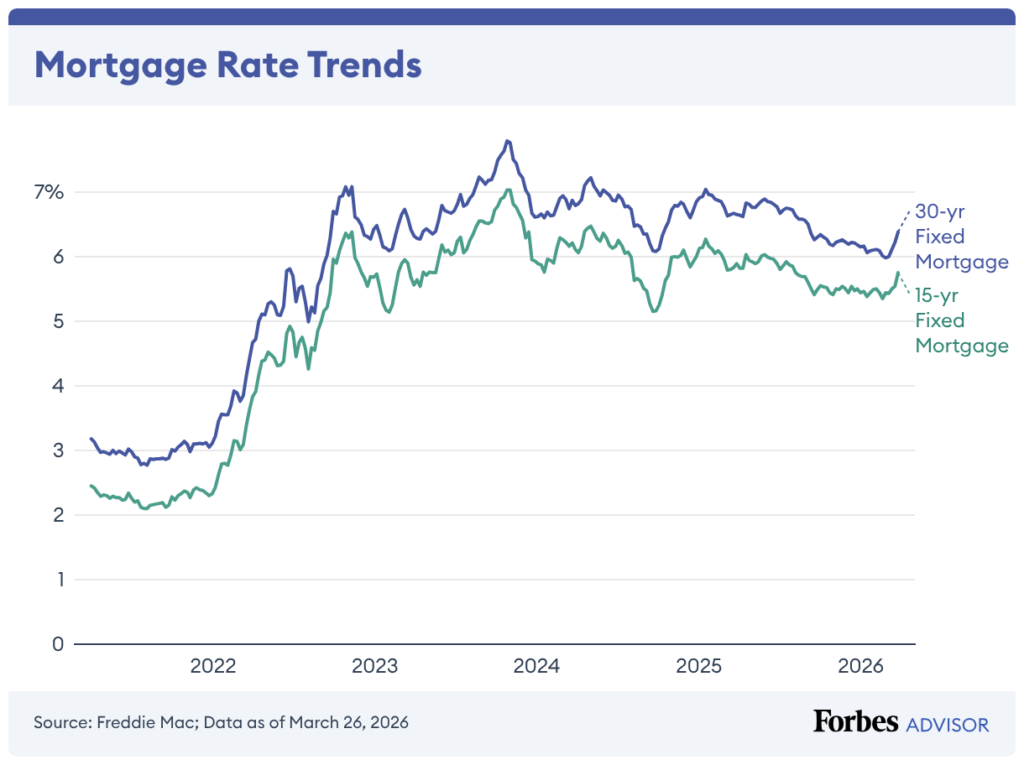

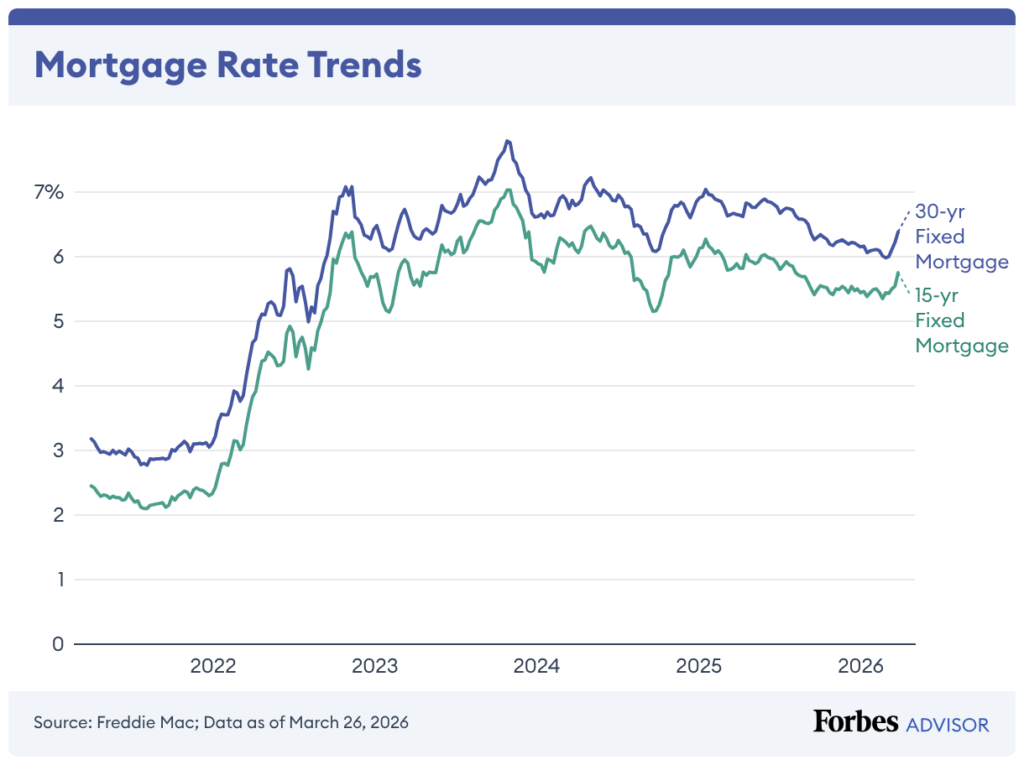

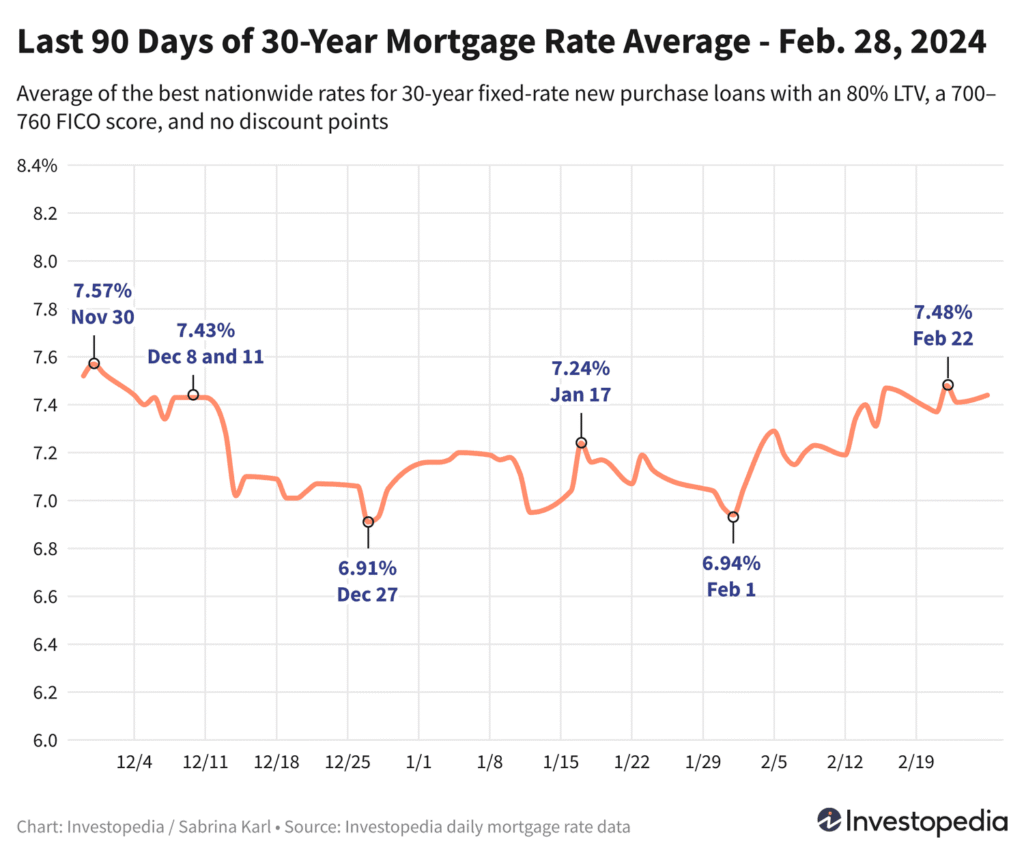

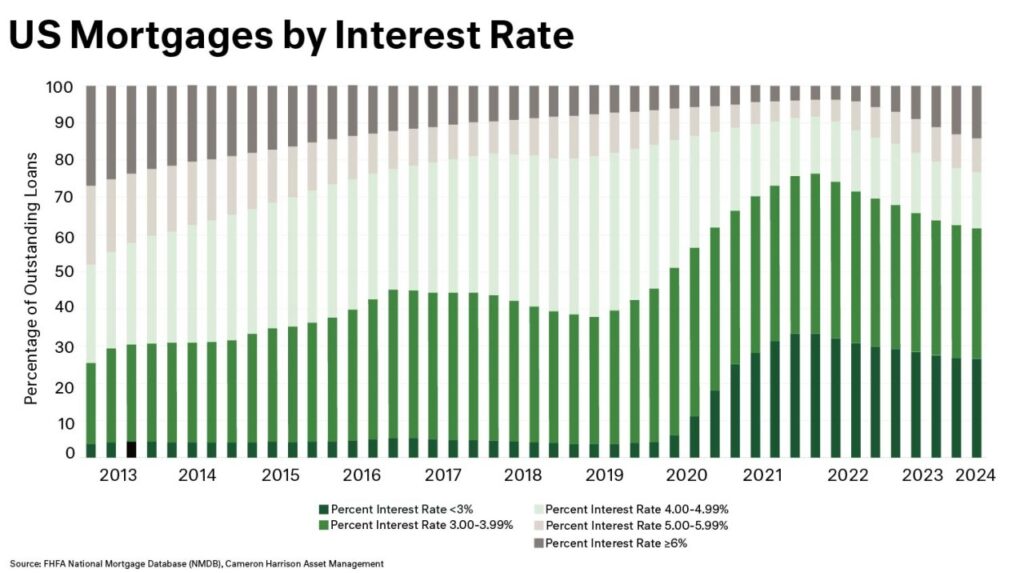

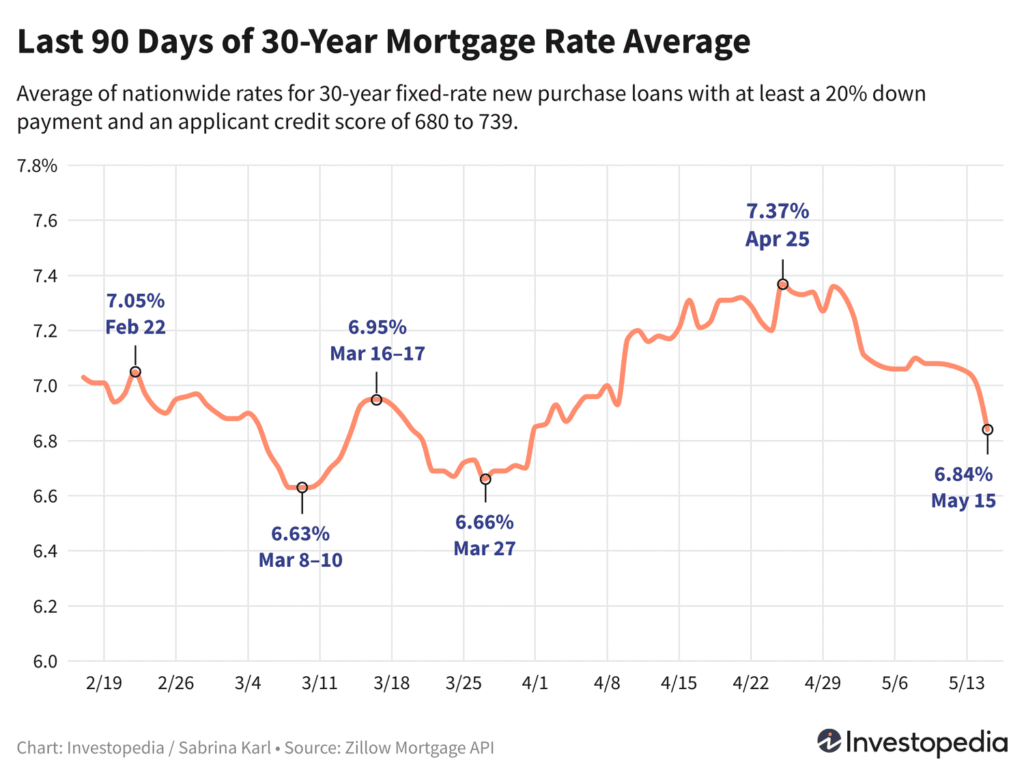

Recent data shows that the average 30-year fixed mortgage rate has climbed to approximately 7.1%–7.3%, compared to around 6.2% just a few months ago. This marks the highest level since mid-2025 and represents a significant jump in borrowing costs for homebuyers.

To understand the impact, consider this:

- A $400,000 home loan at 6.2% results in a monthly payment of about $2,450

- The same loan at 7.2% increases the payment to roughly $2,720

That’s a difference of nearly $270 per month, or more than $3,000 annually, which significantly affects affordability for middle-income buyers.

At the same time, housing inventory remains tight in many parts of the US. Many homeowners who locked in ultra-low rates below 4% during 2020–2021 are reluctant to sell, creating a supply shortage that continues to push home prices higher despite rising borrowing costs.

What This Means for US Homebuyers

For homebuyers, the current environment is a mix of challenges and strategic opportunities. Higher mortgage rates mean reduced purchasing power, forcing many buyers to either lower their budget or delay their purchase altogether.

First-time buyers are particularly impacted. With affordability already stretched due to high home prices, the additional burden of higher interest rates makes it harder to qualify for loans. Many are now exploring alternatives such as smaller homes, different locations, or adjustable-rate mortgages.

However, there is a silver lining. As rates rise, demand tends to cool slightly, which can reduce bidding wars and give buyers more negotiating power. In some markets, sellers are offering concessions such as closing cost assistance or price reductions—something rarely seen during the housing boom.

Buyers who can afford higher payments may find this period less competitive, allowing them to secure better deals compared to the aggressive market conditions of previous years.

Impact on Real Estate Investors and Rental Markets

For real estate investors, rising mortgage rates create a complex scenario. On one hand, higher borrowing costs reduce profit margins, especially for leveraged investments. Cash flow becomes tighter, and returns on new property acquisitions may decline.

On the other hand, rental demand is expected to increase. As homeownership becomes less affordable, more people are choosing to rent, driving up rental prices in many urban and suburban areas. This creates an opportunity for investors focused on rental income.

Institutional investors and large real estate funds are also adjusting their strategies. Many are shifting toward build-to-rent projects or focusing on markets with strong population growth and job expansion.

Another emerging trend is the increase in all-cash buyers. With higher financing costs, investors with liquidity have a competitive advantage, enabling them to negotiate better deals and close transactions faster.

Housing Market Outlook for 2026 and Beyond

Looking ahead, the housing market in 2026 is expected to remain dynamic but stable. Most experts predict that mortgage rates will stay in the 6.5%–7.5% range for much of the year, depending on inflation trends and Federal Reserve policy decisions.

Home prices are likely to grow at a slower pace compared to previous years, with some regions experiencing price stabilization or slight declines. However, a major crash is unlikely due to strong demand, limited supply, and relatively low levels of distressed properties.

Key trends to watch include:

- Increased use of adjustable-rate mortgages (ARMs)

- Growth in suburban and secondary markets

- Continued demand for affordable housing

- Expansion of rental housing developments

If inflation declines more rapidly than expected, mortgage rates could ease later in the year, providing relief to buyers. However, any unexpected economic shocks could push rates even higher.

Risks and Opportunities in a High-Rate Environment

The current high-rate environment presents both risks and opportunities for different market participants.

Risks include:

- Reduced affordability leading to lower home sales

- Increased financial pressure on borrowers

- Potential slowdown in construction activity

- Higher default risk for overstretched buyers

Opportunities include:

- Less competition for buyers entering the market

- Strong rental demand is benefiting investors

- Potential refinancing opportunities if rates decline

- Long-term appreciation in high-demand regions

For buyers and investors alike, the key is to focus on long-term value rather than short-term rate fluctuations. Real estate remains a fundamentally strong asset class, especially in a growing economy like the United States.

Strategic Advice for Buyers and Investors in 2026

Navigating this market requires careful planning and informed decision-making. Buyers should prioritize affordability and avoid stretching their budgets, while also exploring options such as rate buydowns or adjustable-rate loans.

Investors should focus on cash flow, location, and long-term demand drivers rather than speculative price appreciation. Markets with strong job growth, population increases, and infrastructure development are likely to outperform.

It is also essential to stay updated with economic trends, Federal Reserve policies, and housing data. Timing the market perfectly is nearly impossible, but making informed decisions based on data can significantly improve outcomes.

A Turning Point for the US Housing Market

Mortgage Rates Hit 7-Month High — What It Means for US Homebuyers and Investors in 2026 highlights a critical shift in the real estate landscape. While higher rates create challenges, they also bring balance to a market that was previously overheated.

For buyers, this is a time to be strategic and patient. For investors, it is an opportunity to adapt and identify new income streams. The housing market is entering a more sustainable phase, where fundamentals matter more than momentum.

As the year progresses, staying informed and flexible will be key to success in this evolving environment.

Subscribe to trusted news sites like USnewsSphere.com for continuous updates.