Mortgage rates surge again as the Iran war reshapes US housing in 2026, sending shockwaves across homebuyers, investors, and policymakers navigating an already fragile real estate market. What was once expected to be a year of gradual housing recovery has now turned into a period of renewed uncertainty, driven by geopolitical tensions, rising oil prices, and shifting Federal Reserve expectations.

The connection between global conflict and US mortgage rates may not seem obvious at first—but in today’s interconnected financial system, war-driven inflation, energy shocks, and investor fear are tightly linked to borrowing costs. As a result, millions of Americans are facing higher monthly payments, reduced affordability, and a rapidly changing housing landscape.

Mortgage Rates Surge, Rising Mortgage Rates Reflect Global Shockwaves

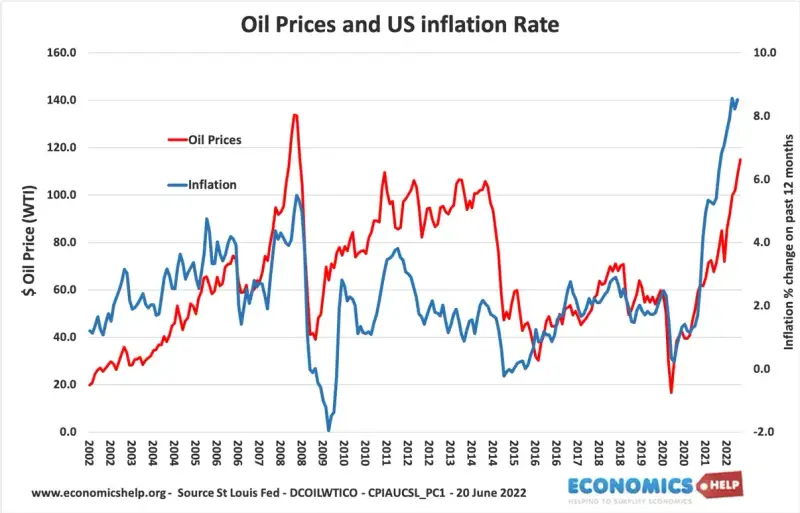

The recent surge in mortgage rates is closely tied to rising global instability. As tensions linked to the Iran conflict intensify, energy markets have reacted sharply, pushing oil prices higher. This has reignited inflation concerns, forcing investors to reassess expectations for US interest rates.

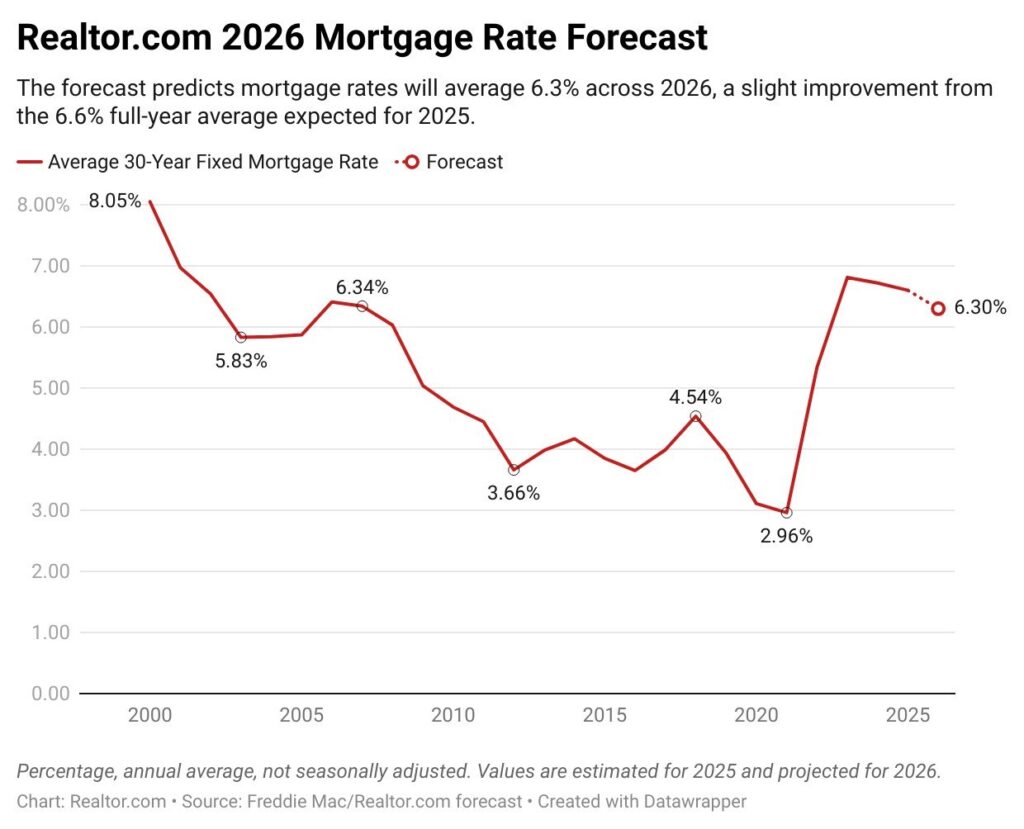

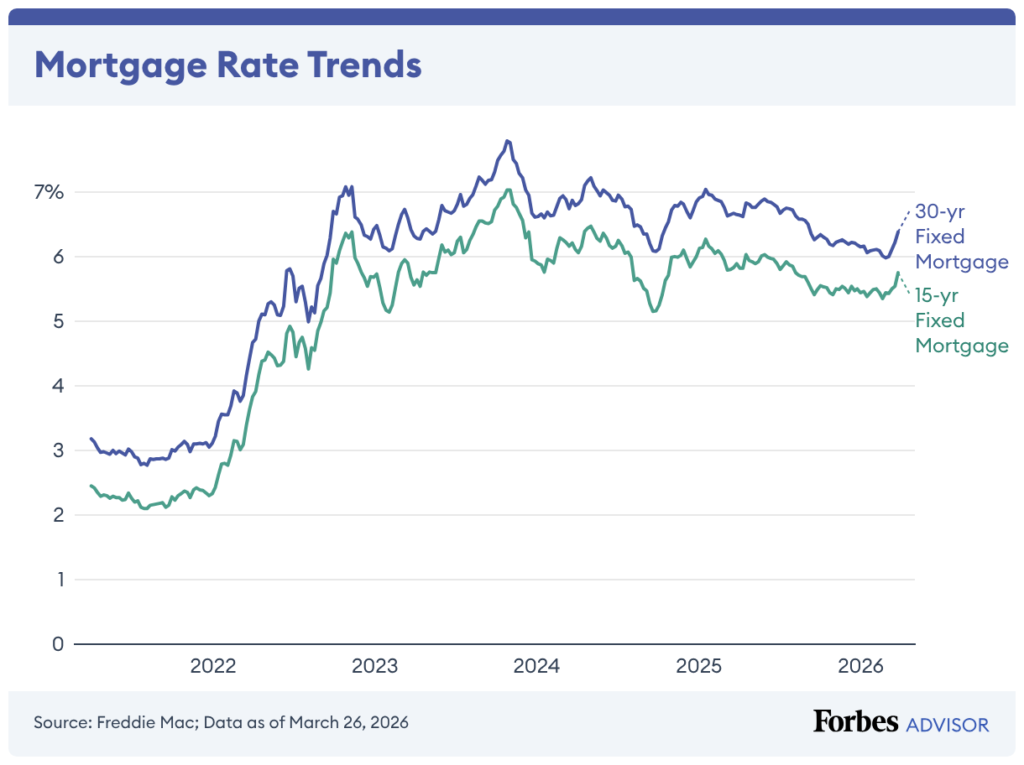

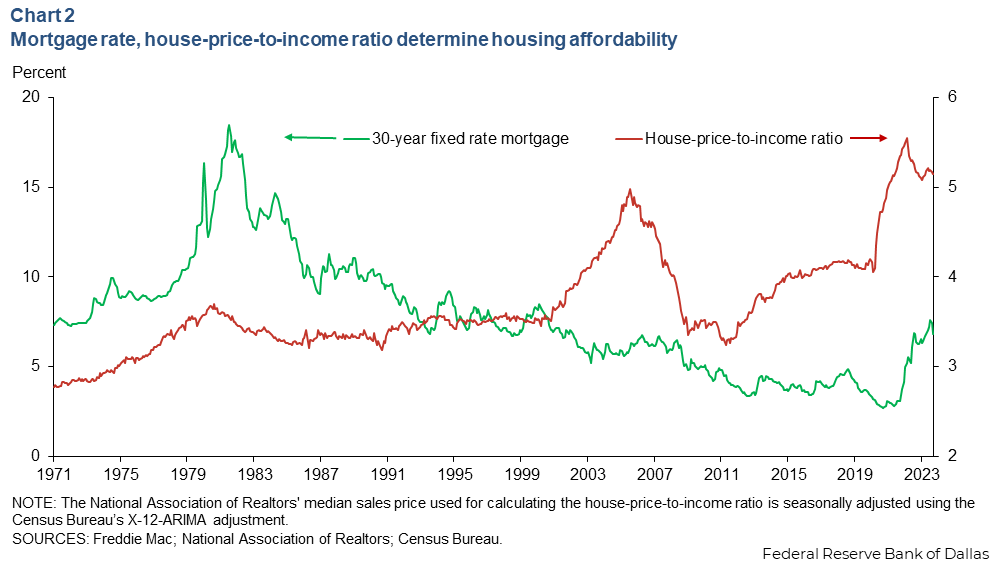

Mortgage rates, which are heavily influenced by the US 10-year Treasury yield, have climbed again as bond yields rise. In recent weeks, average 30-year fixed mortgage rates have moved back above 7%—a level that significantly impacts affordability for the average American household.

This increase is not happening in isolation. It reflects a broader shift in financial markets where investors demand higher returns to compensate for risk. When uncertainty rises globally, borrowing costs follow, and housing becomes one of the first sectors to feel the pressure.

The Iran Conflict’s Impact on Energy and Inflation

One of the most direct ways the Iran war is influencing US housing is through energy prices. Oil markets are highly sensitive to geopolitical tensions in the Middle East, and any disruption in supply can quickly lead to price spikes.

As oil prices rise, transportation and construction costs increase. Builders face higher expenses for materials and logistics, which are often passed on to buyers in the form of higher home prices. At the same time, rising gasoline prices reduce disposable income for consumers, making it harder to afford higher mortgage payments.

Inflation expectations are also rising again. When markets anticipate higher inflation, long-term interest rates tend to increase. This directly affects mortgage rates, making home loans more expensive even if the Federal Reserve does not immediately change its policy.

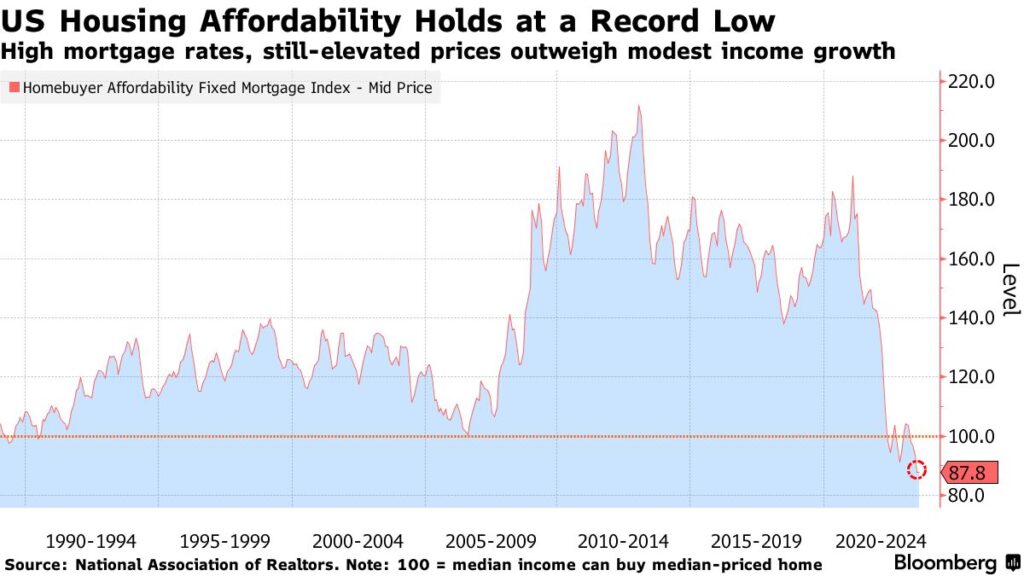

Housing Affordability Hits a New Low in 2026

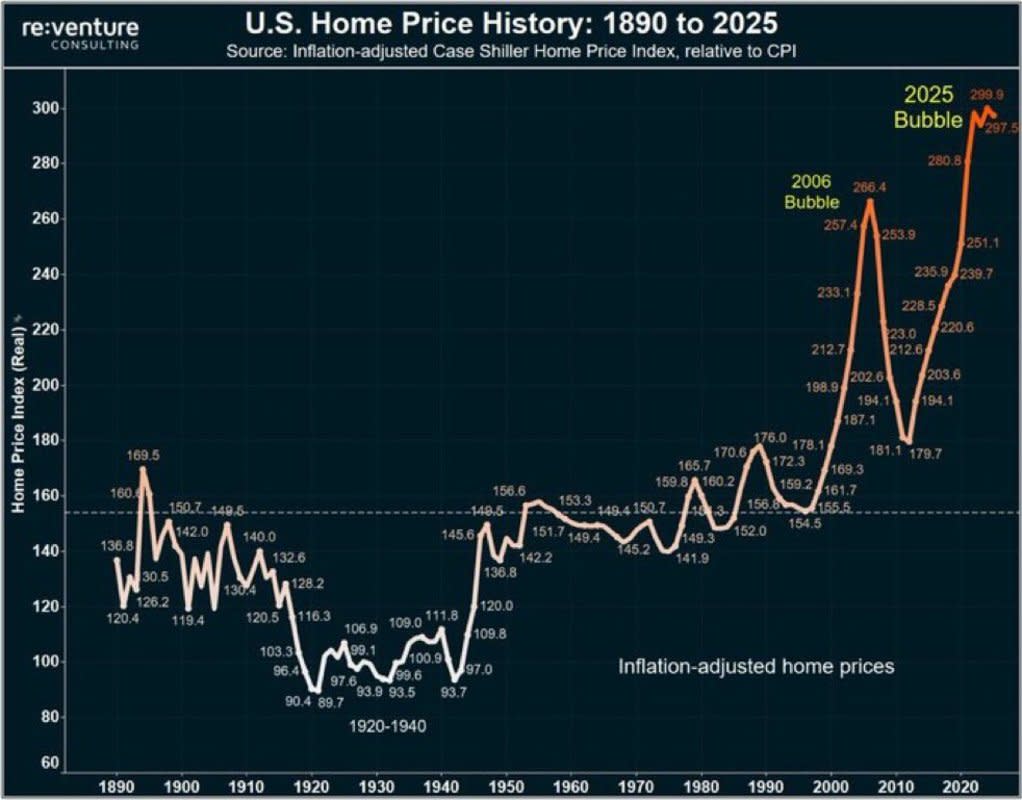

Affordability has become one of the biggest challenges in the US housing market. With mortgage rates climbing above 7% and home prices remaining elevated, the cost of buying a home has reached levels not seen in decades.

Data suggests that the average monthly mortgage payment for a median-priced home is now significantly higher compared to just a few years ago. This has pushed many first-time buyers out of the market entirely, while others are delaying their purchase decisions.

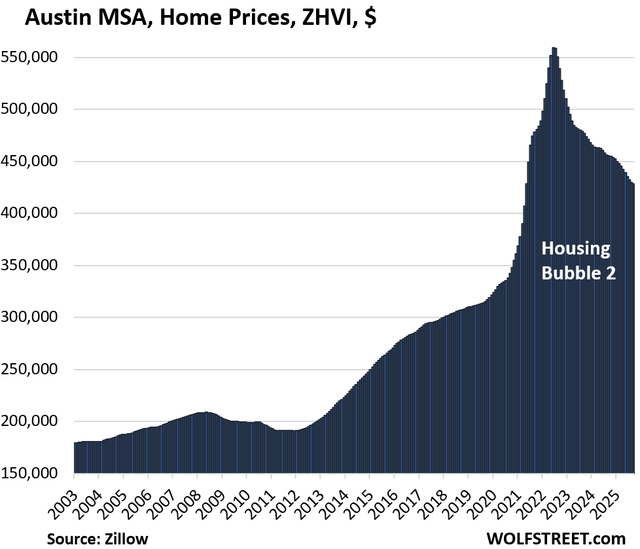

The affordability crisis is also impacting regional markets differently. High-cost areas like California and New York are seeing sharper declines in buyer activity, while some Midwest and Southern markets remain relatively resilient. However, the overall trend is clear: higher rates are cooling demand.

Market Reactions: Buyers, Sellers, and Investors Adjust

The surge in mortgage rates is changing behavior across the housing market. Buyers are becoming more cautious, often waiting for rates to stabilize before making major financial commitments. This has led to a slowdown in home sales and increased inventory in some areas.

Sellers, on the other hand, are facing a new reality. Homes are staying on the market longer, and price reductions are becoming more common. In some regions, bidding wars have disappeared entirely, replaced by more balanced negotiations.

Investors are also adjusting their strategies. Real estate investment, which was highly attractive during the low-rate era, is now being reevaluated. Higher borrowing costs reduce profit margins, leading some investors to shift toward alternative assets such as bonds or dividend-paying stocks.

Federal Reserve Policy and Future Rate Outlook

The Federal Reserve plays a critical role in shaping the direction of mortgage rates. While the Fed does not directly set mortgage rates, its policies influence the broader interest rate environment.

With inflation risks rising due to global tensions, the Fed may adopt a “higher for longer” approach to interest rates. This means keeping rates elevated for an extended period to ensure inflation is brought under control.

Market expectations currently suggest that rate cuts may be delayed further into 2026. If inflation remains persistent, the Fed could even consider additional tightening measures. This uncertainty is a key reason why mortgage rates are rising again.

What This Means for the Future of US Housing

The combination of higher mortgage rates, rising inflation, and global uncertainty is reshaping the US housing market in profound ways. While demand has cooled, supply constraints continue to support home prices, preventing a sharp decline in most areas.

Looking ahead, several scenarios are possible. If geopolitical tensions ease and inflation stabilizes, mortgage rates could gradually decline, providing some relief to buyers. However, if conflicts persist and energy prices remain elevated, rates may stay high for longer.

For buyers, this environment requires careful planning and financial discipline. Locking in a rate at the right time, exploring adjustable-rate mortgages, and considering less competitive markets are all strategies that can help navigate the current landscape.

For policymakers, the challenge is balancing inflation control with economic growth. The housing market is a critical component of the US economy, and prolonged weakness could have broader implications.

A Defining Moment for Housing and Interest Rates

The surge in mortgage rates driven by global tensions and the Iran conflict marks a defining moment for the US housing market. What began as a hopeful year for recovery has turned into a complex and uncertain environment shaped by forces far beyond domestic control.

As inflation fears return and interest rates remain elevated, both buyers and investors must adapt to a new reality. The path forward will depend not only on economic data but also on geopolitical developments that continue to influence markets worldwide.

Staying informed, flexible, and financially prepared will be essential for navigating this evolving landscape.

Subscribe to trusted news sites like USnewsSphere.com for continuous updates.