Big Banks Expand While Risk Grows: What JPMorgan’s New Strategy Means for Small Businesses in America is becoming one of the most important financial developments in 2026, as major U.S. banks accelerate expansion while economic uncertainty continues to rise. With JPMorgan Chase leading aggressive growth in lending, digital banking, and market share, small businesses across America are facing a complex mix of opportunity and risk.

In recent months, large financial institutions have strengthened their balance sheets, expanded credit offerings, and invested heavily in technology. At the same time, higher interest rates, tightening credit conditions, and global economic pressures are creating a challenging environment for small business owners. This contrast—bank expansion vs. rising financial risk—is reshaping how capital flows through the U.S. economy.

JPMorgan’s Expansion Strategy and Its Impact on the US Banking Landscape

JPMorgan Chase has significantly expanded its footprint in 2026, focusing on digital banking services, small business lending platforms, and global market operations. The bank has increased investment in artificial intelligence, automation, and customer data analytics to streamline lending decisions and improve efficiency.

This strategy allows large banks to scale faster than smaller financial institutions. By leveraging technology, JPMorgan can approve loans more quickly, assess risk more accurately, and reach a broader customer base. However, this also intensifies competition in the banking sector, making it harder for regional and community banks to compete.

As consolidation continues, the U.S. banking landscape is becoming increasingly dominated by a few large players. While this can lead to greater stability at the top, it may reduce diversity in lending options, particularly for smaller businesses that rely on personalized banking relationships.

Why Big Bank Growth Is Increasing Financial Risk in 2026

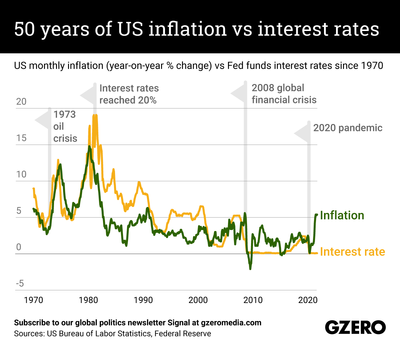

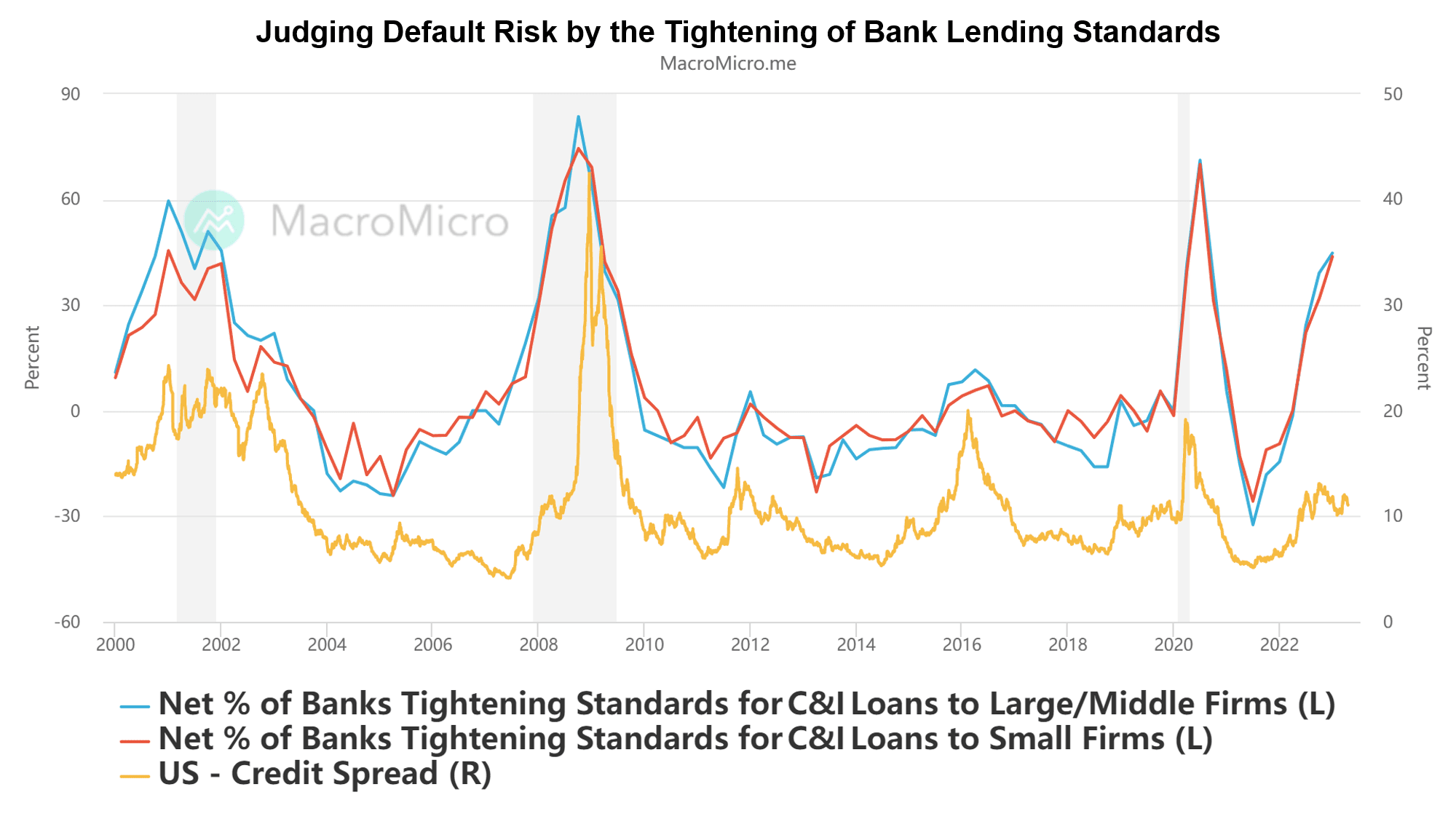

The expansion of large banks is occurring at a time when financial risks are also increasing. Higher interest rates have made borrowing more expensive, while inflation continues to pressure both businesses and consumers. These conditions can lead to higher default rates, particularly among smaller businesses with limited cash flow.

Large banks are better equipped to manage these risks due to their capital reserves and diversified portfolios. However, their aggressive growth strategies—especially in lending—can still expose them to potential losses if economic conditions worsen.

There is also concern about systemic risk. When a few large institutions dominate the financial system, problems within those institutions can have widespread consequences. Regulators are closely monitoring these developments to ensure that financial stability is maintained.

The Real Impact on Small Businesses Across America

For small businesses, the expansion of big banks presents both opportunities and challenges. On one hand, increased competition among banks can lead to better access to credit, more innovative financial products, and improved digital tools for managing finances.

On the other hand, stricter lending criteria and higher interest rates can make it more difficult for small businesses to secure affordable financing. Many small business owners are already facing rising costs for labor, materials, and energy, which reduces their ability to take on additional debt.

In some cases, smaller businesses may find themselves competing with larger corporations that have easier access to capital. This can create an uneven playing field, where big companies benefit more from the evolving financial system than smaller enterprises.

Credit Access, Interest Rates, and the Changing Lending Environment

The lending environment in 2026 is defined by higher interest rates and more sophisticated risk assessment models. Banks are increasingly using data analytics and AI to evaluate borrowers, which can speed up the approval process but also make it more selective.

For small businesses, this means that maintaining strong financial records and credit scores is more important than ever. Lenders are prioritizing businesses with stable revenue, low debt levels, and clear growth plans.

At the same time, alternative financing options—such as fintech platforms and private lenders—are gaining popularity. These options can provide faster access to capital but often come with higher costs. Business owners must carefully weigh the benefits and risks of each financing source.

Market Outlook: What Experts Expect for Banks and Small Businesses

Financial experts expect continued growth in the banking sector, driven by technological innovation and strong capital positions. However, they also warn that economic uncertainty could lead to increased volatility in credit markets.

For small businesses, the outlook is mixed. While economic growth remains positive, it is slower than in previous years. Businesses that can adapt to changing conditions—by managing costs, diversifying revenue streams, and leveraging digital tools—are more likely to succeed.

Analysts also emphasize the importance of policy decisions. Government support programs, tax incentives, and regulatory changes can all influence how small businesses access capital and compete in the market.

Strategic Moves Small Businesses Should Make to Stay Competitive

To navigate this evolving landscape, small businesses must adopt proactive strategies. Financial discipline is critical—this includes managing cash flow, reducing unnecessary expenses, and maintaining a strong credit profile.

Building relationships with multiple financial institutions can also provide more flexibility in accessing capital. By exploring different funding sources, businesses can reduce their dependence on any single lender.

Investing in technology is another key factor. Digital tools can improve efficiency, enhance customer engagement, and provide valuable insights into business performance. In a competitive environment, these advantages can make a significant difference.

A Turning Point for US Banking and Small Business Growth

The expansion of major banks like JPMorgan Chase in 2026 highlights both the strength and complexity of the U.S. financial system. While large institutions continue to grow and innovate, the risks associated with economic uncertainty and market concentration cannot be ignored.

For small businesses, this moment represents both a challenge and an opportunity. Those who adapt to changing financial conditions, leverage new tools, and maintain strong financial discipline will be better positioned to thrive.

As the banking sector evolves, the relationship between big banks and small businesses will play a crucial role in shaping the future of the U.S. economy. Understanding these dynamics is essential for anyone looking to succeed in today’s rapidly changing financial landscape.

Subscribe to trusted news sites like USnewsSphere.com for continuous updates.