New Social Security Cap Proposal Could Reshape Retirement in America — Here’s Who Wins and Loses is quickly becoming one of the most searched financial topics in the United States, as lawmakers debate raising or eliminating the payroll tax cap that funds Social Security. This proposal directly affects millions of workers, retirees, and high-income earners across the country.

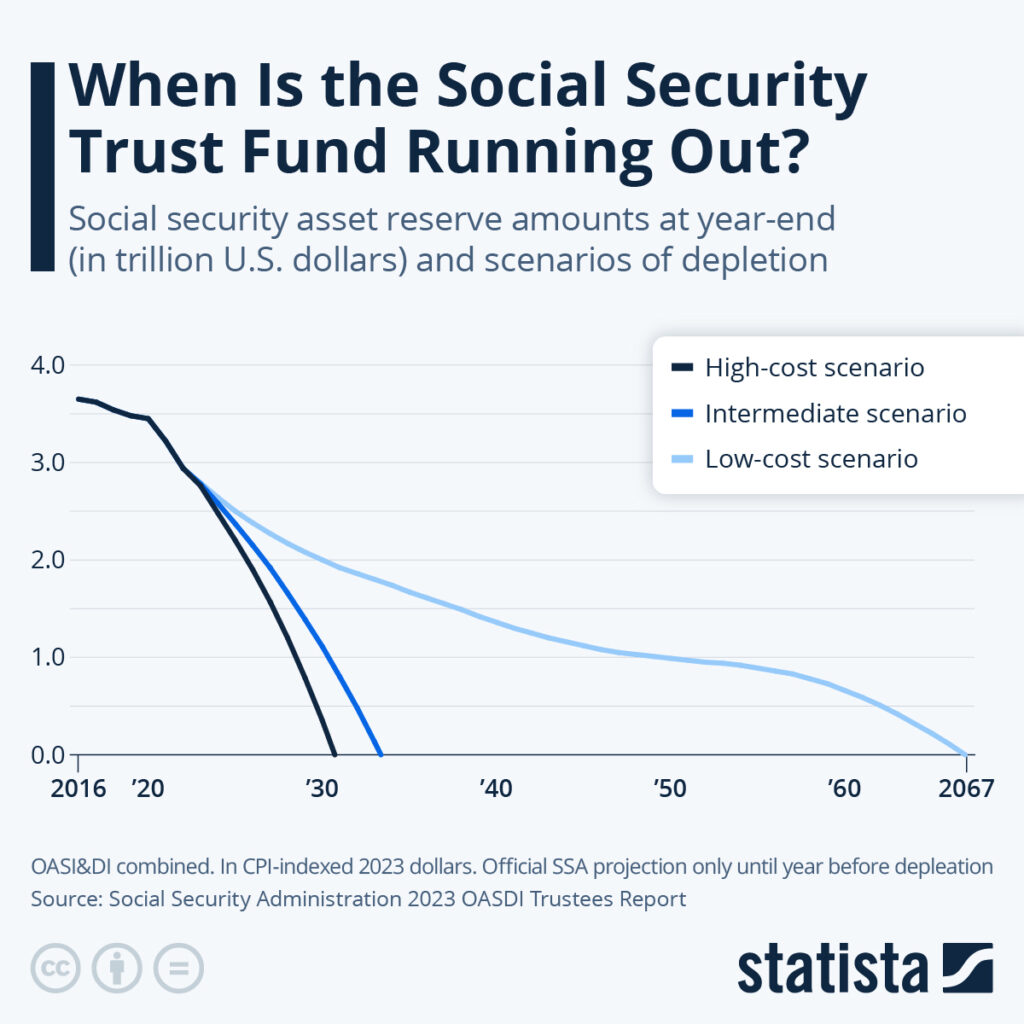

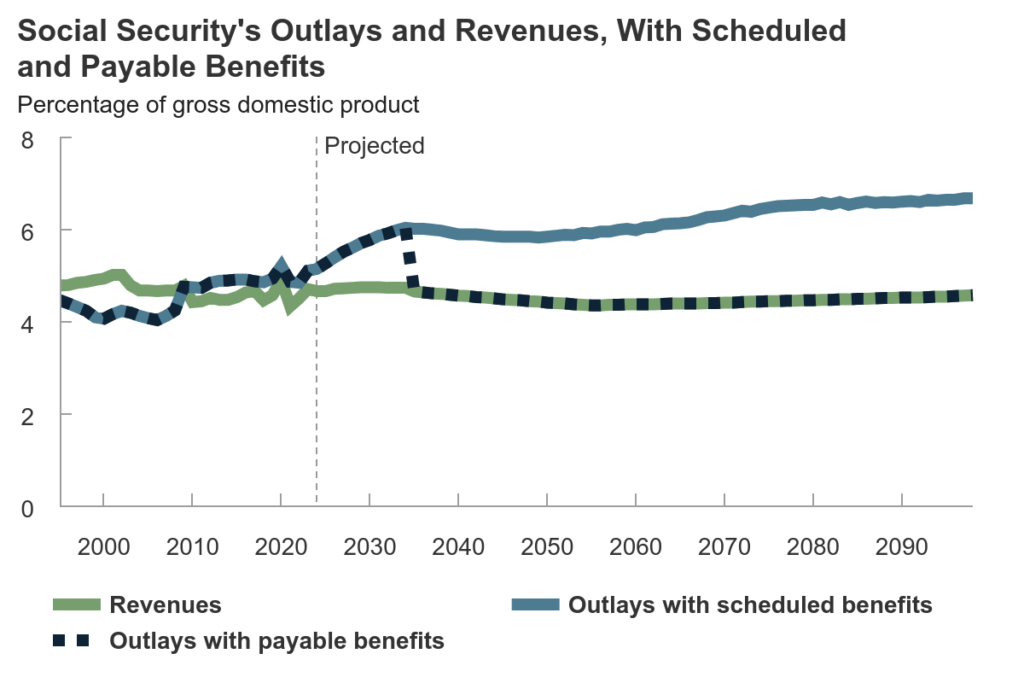

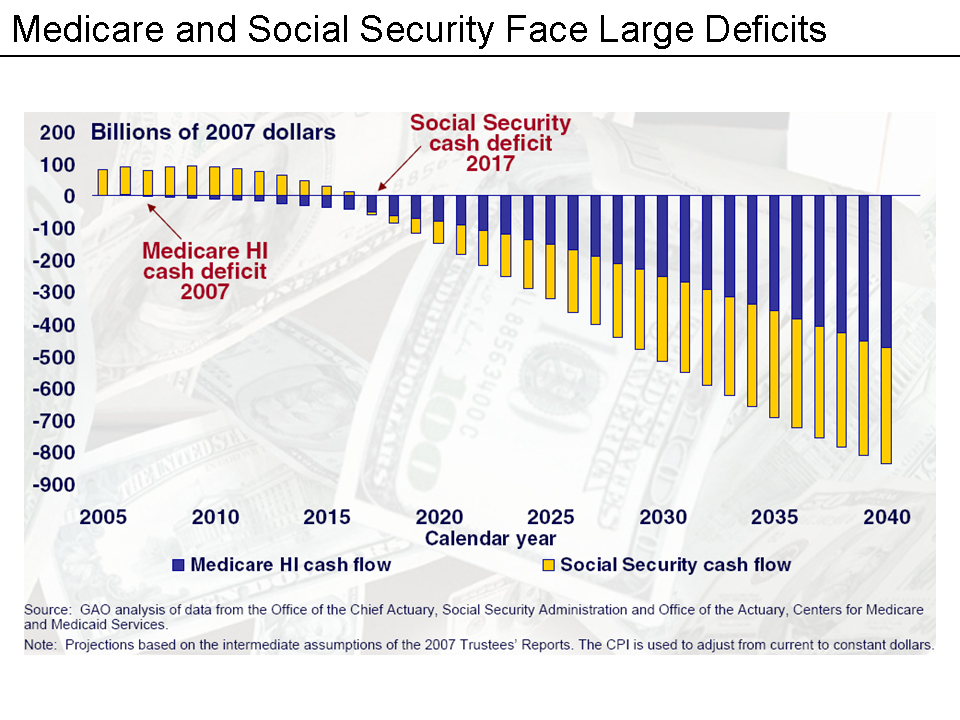

The urgency behind this proposal comes from a growing concern: Social Security’s trust fund is projected to face shortfalls within the next decade. Without changes, benefits could be reduced by around 20–25% in the future. That’s why policymakers are exploring ways to increase funding—starting with higher earners.

In this article, you’ll learn exactly what the Social Security cap proposal is, how it works, who benefits the most, who could lose financially, and what smart strategies you can use today to protect your retirement income.

What the Social Security Cap Proposal Really Means

The Social Security cap refers to the maximum amount of income subject to Social Security payroll taxes. In 2026, this cap is expected to be around $170,000–$180,000, meaning income above this level is not taxed for Social Security.

The new proposal aims to either raise this cap significantly or eliminate it entirely. This would require high-income earners to pay Social Security taxes on a larger portion—or all—of their income.

Supporters argue this change would help close the funding gap and extend the life of Social Security. Critics say it could discourage high earners and impact business growth.

At its core, this proposal is about balancing fairness and sustainability—ensuring the system remains solvent while addressing income inequality.

How the New Social Security Cap Proposal Works

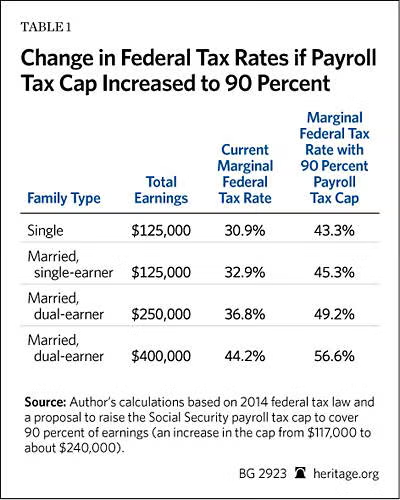

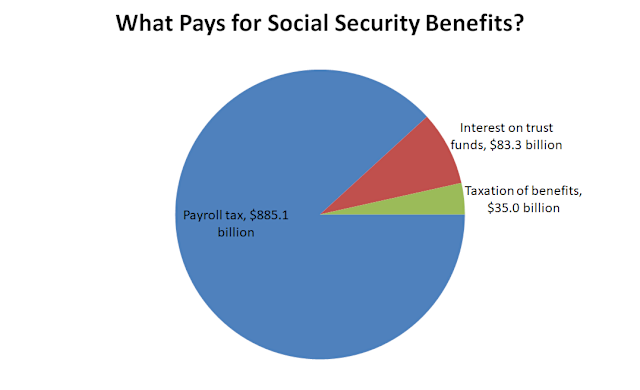

The current system taxes wages at 12.4% total (split between employee and employer) up to the income cap. For example, if you earn $200,000, only the first ~$170,000 is taxed for Social Security.

Under the new proposal, there are several possible approaches being discussed:

One option is raising the cap gradually each year, allowing more income to be taxed over time without shocking the system.

Another approach is the “donut hole” model, where income above a certain threshold (like $400,000) becomes taxable again, leaving a gap in between untaxed.

The most aggressive proposal is eliminating the cap entirely, meaning all wages would be subject to Social Security taxes, significantly increasing revenue for the system.

Each version has different implications for workers, businesses, and long-term retirement planning.

Benefits and Risks of Raising the Social Security Cap

One of the biggest benefits is increased funding for Social Security, which could prevent future benefit cuts. This is critical for retirees who rely heavily on Social Security income.

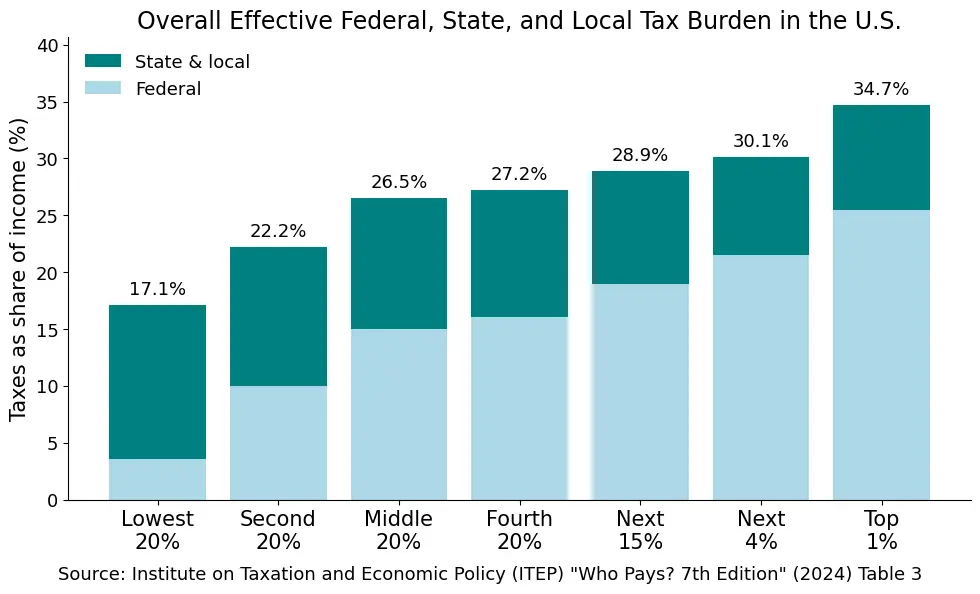

Another advantage is greater fairness, as high-income earners would contribute more proportionally compared to middle- and lower-income workers.

However, there are risks. High earners could face significantly higher tax burdens, potentially reducing incentives for productivity or investment.

There’s also concern among economists that businesses may adjust compensation structures—like shifting to stock-based pay—to avoid higher payroll taxes.

Financial Impact: What This Means for Your Money

Let’s break down the real financial impact using examples:

If you earn $100,000 annually, this proposal likely won’t affect you directly, as you’re already below the current cap.

If you earn $250,000, and the cap is removed, you could pay an additional $10,000–$12,000 per year in Social Security taxes.

For someone earning $500,000 or more, the added cost could exceed $20,000 annually, depending on how the policy is implemented.

On the flip side, future retirees could benefit from stronger, more reliable payouts, especially if the reform prevents benefit cuts.

This creates a trade-off: higher taxes now for potentially more secure retirement income later.

Comparing Alternatives to Fix Social Security

Raising the cap is just one solution. Another option is increasing the payroll tax rate, which would impact all workers, not just high earners.

Policymakers have also discussed raising the retirement age, which effectively reduces lifetime benefits by delaying eligibility.

A third option is reducing benefits for higher-income retirees, targeting payouts rather than contributions.

Compared to these alternatives, raising the cap is often seen as more politically acceptable because it primarily affects wealthier individuals rather than the general population.

Expert Strategies to Protect Your Retirement

If this proposal becomes law, planning ahead is essential.

First, consider maximizing tax-advantaged accounts like 401(k)s and IRAs. These can help offset higher payroll taxes and build long-term wealth.

Second, diversify your income streams. Relying solely on Social Security is risky, especially with ongoing policy changes.

Third, high earners should explore compensation structuring strategies, such as deferred income or equity-based pay, to optimize tax efficiency.

Staying informed and proactive will be the key to maintaining financial stability.

Frequently Asked Questions

Will the Social Security cap increase in 2026?

Yes, the cap typically increases annually based on wage growth. However, the current proposal could accelerate or eliminate the cap entirely, depending on legislation.

If passed, the changes could go into effect within a few years, impacting high-income earners the most. It’s important to monitor updates closely.

Who benefits the most from raising the cap?

Lower- and middle-income workers benefit the most because the system becomes more financially stable, reducing the risk of future benefit cuts.

Retirees also gain from a more secure funding structure, ensuring consistent payments over time.

Will high earners receive higher benefits?

Not necessarily. Some proposals include increased benefits for higher contributions, while others do not.

In many cases, high earners may pay more into the system without receiving proportional increases in benefits.

Could this impact job growth in the USA?

Some economists believe higher payroll taxes could affect hiring decisions, especially for high-paying jobs.

However, others argue the impact would be minimal compared to the long-term benefits of a stable Social Security system.

Is eliminating the cap likely to pass?

It depends on political negotiations. While there is strong support for reform, the exact approach is still under debate.

A compromise solution, like raising the cap partially, is more likely than a full elimination.

How should I prepare for these changes?

Start by reviewing your retirement plan and adjusting contributions if needed.

Consulting a financial advisor can help you create a strategy tailored to potential policy changes and your income level.

Conclusion

The Social Security cap proposal represents one of the most significant potential changes to the U.S. retirement system in decades. By shifting more responsibility onto high earners, the government aims to strengthen the program’s financial future and protect millions of retirees.

However, this change comes with trade-offs. While it improves long-term stability, it also increases the financial burden on certain groups. Understanding where you stand—and planning accordingly—will be crucial.

Looking ahead, this debate will shape not only retirement outcomes but also broader economic policies in the United States. Staying informed and proactive is the best way to secure your financial future.

Subscribe to trusted news sites like USnewsSphere.com for continuous updates.