Mortgage Incentives Surge as Housing Slows: Is the US Real Estate Market Entering a New Phase? This question is now at the center of the American housing conversation in 2026, as builders, lenders, and buyers react to a rapidly shifting market. After years of strong price growth and tight inventory, the housing sector is showing clear signs of cooling. In response, developers and lenders are rolling out aggressive incentives—from rate buydowns to closing cost assistance—to keep demand alive.

This shift marks a potential turning point for the US real estate market. For investors, homebuyers, and policymakers, understanding what’s driving these changes—and what comes next—is critical for navigating the evolving economic landscape.

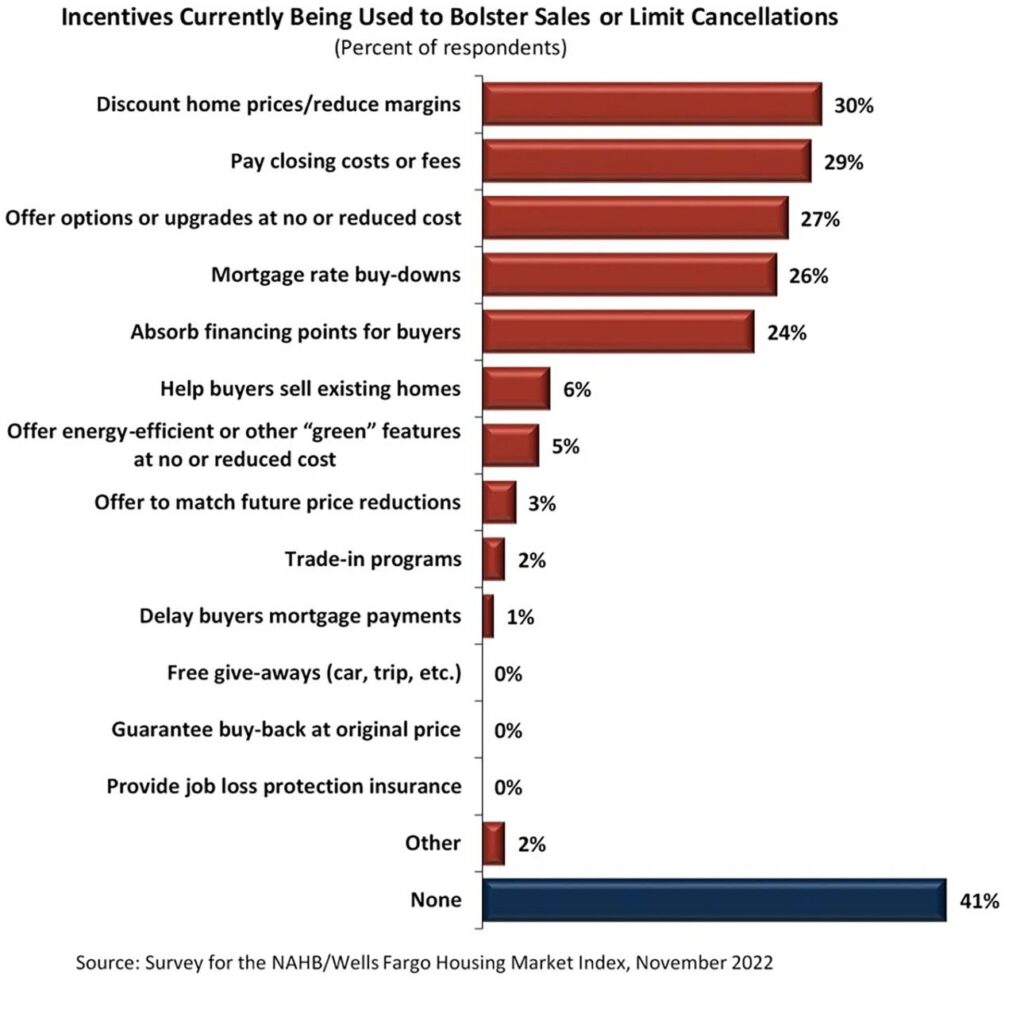

Why Mortgage Incentives Are Surging Across the US

In 2026, mortgage incentives are becoming one of the most powerful tools used by homebuilders and lenders to maintain sales momentum. As borrowing costs remain elevated compared to previous years, affordability has become a major barrier for many potential buyers.

To address this, builders are offering incentives such as interest rate buydowns, reduced closing costs, and even direct price discounts. These strategies are designed to lower monthly payments and make homes more accessible without significantly cutting headline prices.

This trend reflects a broader adjustment in the market. Instead of sharp price declines, the housing sector is adapting through incentives that quietly improve affordability. For buyers, this creates opportunities—but also requires careful evaluation of the true value of these offers.

The Role of Interest Rates in Shaping Housing Demand

Interest rates remain one of the most important drivers of housing activity. Decisions by the Federal Reserve have kept mortgage rates relatively high, even as inflation has moderated from earlier peaks.

Higher mortgage rates increase the cost of borrowing, reducing purchasing power for many buyers. This has led to a slowdown in home sales, particularly in markets that experienced rapid price growth in recent years.

However, the relationship between rates and housing demand is not straightforward. While high rates can suppress demand, expectations of future rate cuts can encourage buyers to enter the market early. This dynamic is creating a complex environment where sentiment plays a key role alongside economic fundamentals.

Housing Supply and Builder Strategy in a Cooling Market

Another key factor shaping the current market is supply. After years of underbuilding, the US housing market is still facing structural shortages in many regions. However, new construction activity has increased, adding more inventory to the market.

Builders are adjusting their strategies to align with changing demand conditions. Instead of focusing solely on price increases, they are prioritizing sales volume and cash flow. This shift is driving the widespread use of incentives as a way to attract buyers.

At the same time, existing homeowners are often reluctant to sell, particularly if they have locked in lower mortgage rates in previous years. This creates a unique supply dynamic where new homes play a larger role in meeting demand compared to resale properties.

Market Signals: What the Data Is Telling Investors

Recent data points to a market that is neither booming nor collapsing, but rather transitioning. Home price growth has slowed in many areas, while inventory levels are gradually increasing. At the same time, mortgage applications have shown volatility, reflecting uncertainty among buyers.

Investors are closely watching these trends as indicators of broader economic conditions. The housing market has historically been a leading indicator of economic cycles, making it a key area of focus.

In addition, changes in housing activity can influence other sectors, including construction, retail, and financial services. This interconnectedness means that shifts in real estate often have ripple effects throughout the economy.

Hidden Risks Beneath the Surface of the Housing Market

While incentives are helping sustain activity, they also highlight underlying challenges. One of the main risks is affordability. Even with incentives, high home prices and interest rates can limit access for many buyers.

Another concern is the potential for regional imbalances. Some markets may experience sharper slowdowns than others, depending on factors such as job growth, population trends, and local economic conditions.

There is also the question of long-term sustainability. If incentives become the primary driver of demand, it could signal that the market is struggling to stand on its own. This raises important questions about future price stability and overall market health.

Is the US Real Estate Market Entering a New Phase?

The current environment suggests that the housing market is moving into a new phase—one defined by moderation rather than rapid growth. Instead of the intense competition and rising prices seen in previous years, the focus is shifting toward balance and affordability.

This transition is not necessarily negative. A more stable market can provide opportunities for buyers who were previously priced out, while also reducing the risk of speculative bubbles.

However, the path forward will depend on several factors, including interest rates, economic growth, and consumer confidence. As these elements evolve, they will shape the trajectory of the housing market in the years ahead.

What this means for you

For homebuyers, the current market offers both challenges and opportunities. Incentives can make homeownership more accessible, but it is important to evaluate the long-term affordability of any purchase.

For homeowners, the shift in market dynamics may affect property values and selling strategies. Understanding local market conditions can help you make informed decisions.

Investor takeaway

For investors, the housing market in 2026 presents a mixed outlook. While opportunities exist, particularly in areas with strong fundamentals, risks related to affordability and demand cannot be ignored.

Careful analysis of market trends, regional dynamics, and economic indicators is essential for identifying potential opportunities and managing risk.

Future outlook

Looking ahead, the US housing market is likely to remain in a state of transition. Interest rate movements, policy decisions, and economic conditions will all play a role in shaping its future.

If rates begin to decline, demand could strengthen, supporting price stability. However, if economic uncertainty persists, the market may continue to adjust through incentives and slower growth.

A Market in Transition

The surge in mortgage incentives is a clear sign that the US housing market is evolving. While challenges remain, this transition also creates opportunities for those who understand the changing landscape.

By staying informed and analyzing key trends, buyers and investors can navigate this new phase with greater confidence.

Subscribe to trusted news sites like USnewsSphere.com for continuous updates.