Goldman Sachs raises Q4 oil price outlook after OECD stocks fall short of expectations, driving a significant recalibration in global crude price forecasts and raising questions about supply-demand balance through 2026. This fresh outlook, now widely discussed across leading energy news sources, suggests stronger prices ahead even as the bank maintains a forecast of a global surplus next year. Why this matters now: as traders, producers, and policymakers react to tighter inventory conditions and shifting geopolitical drivers, the oil market could see renewed volatility and investor focus well into 2027 and beyond.

What Goldman Sachs Revised and Why

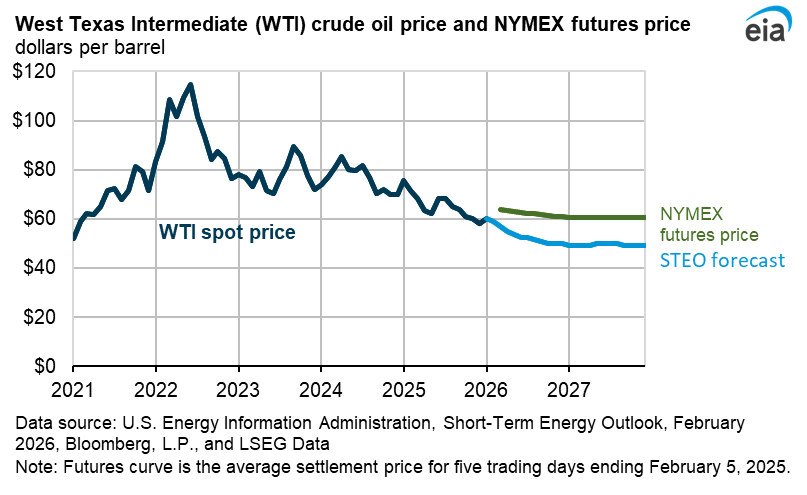

Goldman Sachs boosted its fourth-quarter 2026 crude oil price forecasts by approximately $6 per barrel, lifting Brent crude projections to about $60 and WTI to around $56 by year-end. This revision stems primarily from lower-than-expected crude and product inventories in OECD countries, signaling a tighter physical market cushion than previously assumed.

At the same time, the bank maintained its broader view that the world oil market will still register a surplus in 2026 — roughly around 2.3 million barrels per day (bpd) — provided no large supply disruptions occur. This paradox of a surplus forecast alongside higher prices highlights how inventory dynamics are increasingly shaping traders’ expectations.

The inventory drawdown in OECD nations is seen as a signal of global balance tightening, even if aggregate supply still outpaces demand. These developments have attracted global energy investor attention and are now trends tracked by major financial platforms.

Deeper Into Oil Market Fundamentals

Goldman’s decision to lift price forecasts reflects a shift in how inventory and geopolitical risk are weighted in price models. Lower commercial stocks suggest that even modest demand growth could quickly absorb existing supply, tightening the margin of inventories that traders consider safe against disruptions.

Although Goldman assumes no major supply shocks related to Iran or Russia in its base case, it nevertheless warns that sanctions relief or political shifts could quickly add barrels to the market, exerting downward pressure on benchmarks. For example, relieving Iran or Russia sanctions could potentially trim Brent prices by about $5 and WTI by roughly $8 in the fourth quarter of 2026 if additional supply hits the market quicker than expected.

What matters here is not just the forecast shift itself, but how these dynamics influence investor decisions, refinery planning, and national energy policies. As Goldman’s view has changed, so too has market positioning in futures and options markets globally.

Geopolitical and Demand Drivers in the Oil Forecast

The backdrop to Goldman’s latest forecasts includes heightened geopolitical developments, such as ongoing U.S.–Iran nuclear negotiations and broader Middle East tensions. These scenarios have periodically pushed benchmark oil prices higher due to risk premiums tied to possible supply disruptions, even as diplomatic progress has sometimes eased fears and slightly dampened prices in the short term.

Global demand patterns — especially in Asia and emerging markets — remain central to long-term price trends. Even though some Asian economies are seeing slower growth, solid global fuel consumption still supports baseline demand, which in turn underpins price stability expectations for 2027 and beyond.

These forces, combined with the structural shift toward renewable energy and slower upstream investment in traditional oil sectors, suggest that oil markets may remain more sensitive to supply shocks and inventory shifts than they have been in past years.

Long-Term Oil Price Projections and Market Impact

Looking beyond 2026, Goldman projects that crude prices could firm further into 2027 as demand growth continues while supply capacity growth slows. Under this view, Brent and WTI prices could rise toward $65–$70 per barrel by the end of 2027, assuming current trends persist and geopolitical risk premiums evolve gradually.

This longer-term outlook reflects a common theme among major commodities analysts: the era of abundant, low-cost crude may be giving way to a market environment in which even moderate supply constraints have outsized price impacts. For investors and industry stakeholders, this reinforces the importance of strategic planning across portfolios, production cycles, and energy policy frameworks.

Why This Matters Now

Goldman’s updated forecast matters because it reshapes expectations for energy markets at a time of heightened investor attention and economic uncertainty. With inventories tighter than models predicted, markets now see less buffer against unexpected disruptions, making prices more responsive to news and policy developments.

For traders, producers, and consumers, this means a renewed focus on inventory data, OPEC+ production decisions, and geopolitical dialogues — all of which could swing prices more sharply than in a balanced or oversupplied market environment.

Goldman Sachs’ upward revision of oil price forecasts signals that global crude markets are becoming more responsive to inventory trends and geopolitical factors. While the bank still sees oversupply in 2026, tighter OECD stockpiles have prompted higher price expectations for the fourth quarter and beyond. Investors and energy analysts are watching these shifts closely, as they have real implications for refining margins, investment decisions, and broader economic planning.

Subscribe to trusted news sites like USnewsSphere.com for continuous updates.