Crypto Meets Housing: Fannie Mae’s New Mortgage Move Could Change US Real Estate Forever is rapidly becoming one of the most talked-about developments in both the financial and real estate sectors. As digital assets gain legitimacy and institutional backing, the possibility of using cryptocurrency in mortgage underwriting signals a major shift in how Americans may buy homes in the near future. This evolving trend is not just hype—it reflects bigger changes in wealth storage, lending standards, and financial inclusion.

Recent discussions and emerging pilot frameworks suggest that major housing finance entities are exploring ways to consider crypto holdings—such as Bitcoin and Ethereum—as part of borrower financial profiles. This could unlock a new class of homebuyers, particularly younger, tech-savvy investors who have built significant wealth in digital assets but lack traditional income documentation.

Crypto Meets Housing: Why Fannie Mae’s Crypto Move Matters Right Now

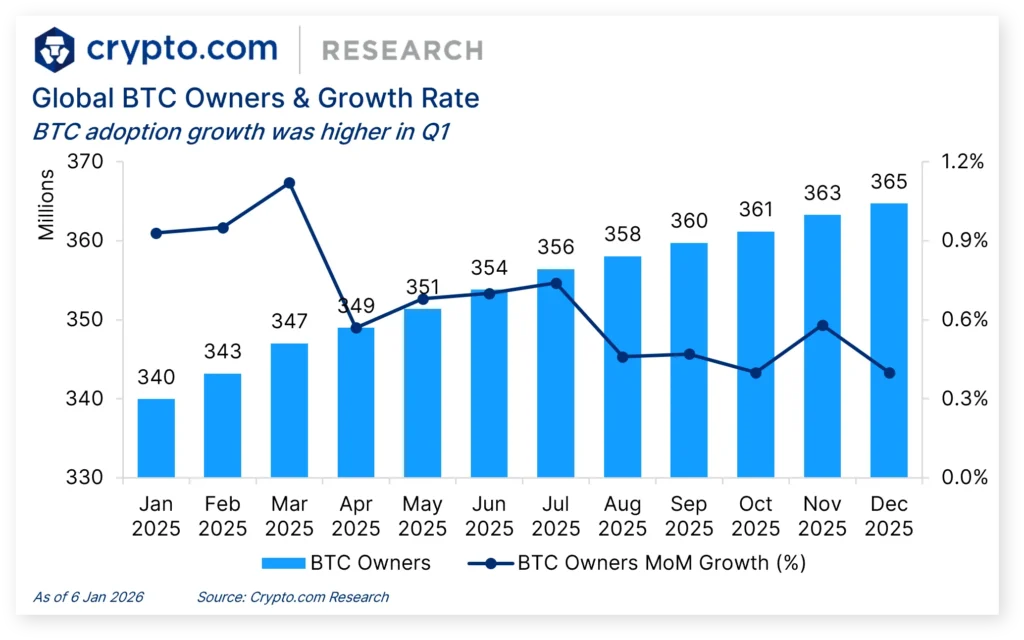

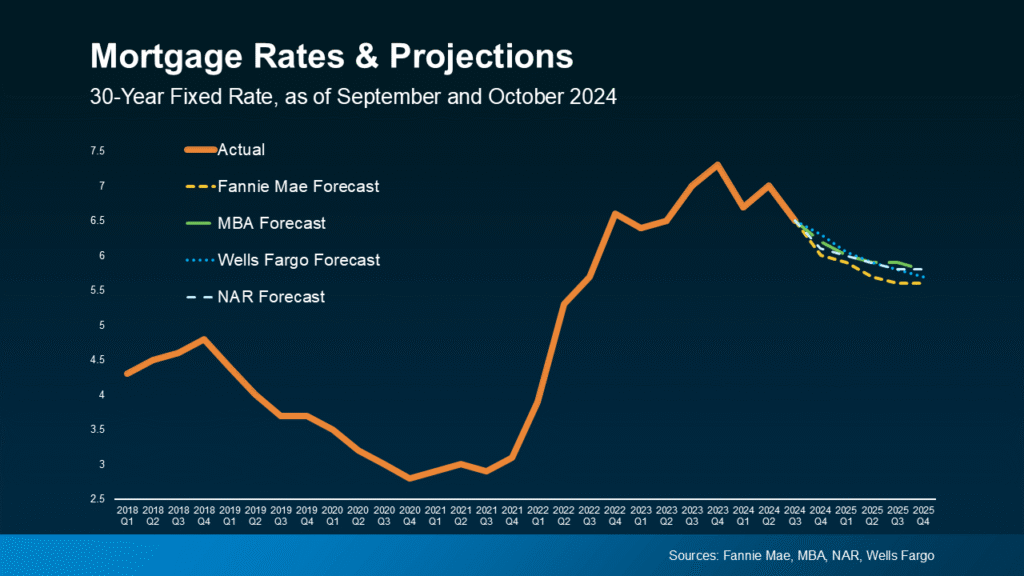

The US housing market is at a crossroads. Mortgage rates have fluctuated between 6% and 7.5% over the past year, affordability remains strained, and first-time buyers are struggling to enter the market. At the same time, cryptocurrency adoption has surged globally, with over 420 million crypto users worldwide as of 2025.

Fannie Mae’s exploration into crypto-backed mortgage considerations represents a potential bridge between these two worlds. By recognizing digital assets as part of a borrower’s net worth, lenders could expand eligibility criteria and create new pathways to homeownership.

This shift is especially relevant for millennials and Gen Z buyers. Many of these individuals have accumulated wealth through crypto investments rather than traditional savings accounts. However, current mortgage systems often fail to recognize this wealth unless it is converted into fiat currency, which can trigger taxes and reduce overall purchasing power.

How Crypto Could Be Used in Mortgage Approval

The concept of integrating cryptocurrency into mortgage underwriting is still evolving, but early models suggest several possible approaches. One of the most discussed methods is allowing crypto assets to be counted as reserves or collateral, similar to stocks or bonds.

In this model, borrowers would not necessarily need to liquidate their crypto holdings. Instead, lenders could evaluate the value of these assets—often with a discount to account for volatility—and include them in the borrower’s financial profile. This could improve debt-to-income ratios and increase loan eligibility.

Another potential approach involves crypto-backed loans, where borrowers use their digital assets as collateral to secure mortgage financing. This method is already used in decentralized finance (DeFi) platforms and could be adapted for traditional housing finance with proper regulation and risk management.

However, volatility remains a key concern. Bitcoin, for example, has experienced price swings of over 50% within a single year. To mitigate this risk, lenders may apply conservative valuation methods or require higher reserves.

Market Impact: What This Means for US Real Estate

If implemented at scale, crypto-integrated mortgages could significantly impact the US housing market. One immediate effect would be an increase in demand, particularly in urban and tech-driven regions where crypto adoption is highest.

Cities like Miami, Austin, and San Francisco—already known for their tech ecosystems—could see a surge in buyers who previously could not qualify for traditional mortgages. This could drive property prices higher in these areas, while also increasing transaction volumes.

On a broader level, this move could modernize the mortgage industry. Traditional underwriting models have remained largely unchanged for decades, relying heavily on W-2 income and credit scores. Incorporating digital assets introduces a more holistic view of wealth, aligning lending practices with the realities of the modern economy.

Data from recent housing reports indicates that nearly 12% of first-time homebuyers in the US have invested in cryptocurrency. If even a fraction of these individuals gain access to mortgage financing through crypto recognition, the market could experience a noticeable shift in buyer demographics.

Risks and Challenges Behind Crypto Mortgages

Despite the potential benefits, the integration of cryptocurrency into mortgage lending comes with significant risks. The most obvious is price volatility. Unlike traditional assets, crypto values can change dramatically in short periods, posing challenges for both lenders and borrowers.

Regulatory uncertainty is another major hurdle. While the US government has taken steps toward clearer crypto regulations, the framework is still evolving. Lenders must ensure compliance with federal housing policies, anti-money laundering laws, and consumer protection standards.

There is also the issue of asset verification. Unlike traditional bank accounts, crypto holdings are stored in digital wallets, which can vary in transparency and security. Lenders will need robust systems to verify ownership and assess risk accurately.

Cybersecurity is another concern. As digital assets become part of mortgage processes, the risk of hacking and fraud increases. Financial institutions will need to invest heavily in secure infrastructure to protect both themselves and their customers.

Expert Insights and Industry Reactions

Financial experts are divided on the long-term impact of crypto mortgages. Some view it as a necessary evolution, while others warn of potential instability.

Proponents argue that recognizing crypto assets is a logical step in a digital-first economy. They believe it could democratize homeownership and provide opportunities for individuals who have been overlooked by traditional financial systems.

Critics, however, caution that integrating highly volatile assets into long-term financial commitments like mortgages could increase systemic risk. They point to past financial crises as examples of what can happen when lending standards become too flexible.

Industry leaders in fintech and real estate are closely monitoring these developments. Several startups are already offering crypto-based home financing solutions, indicating strong market demand. If established institutions like Fannie Mae fully embrace this model, it could accelerate adoption across the entire industry.

Future Outlook: A New Era of Home Financing

The intersection of cryptocurrency and housing finance represents a broader transformation in how wealth is defined and utilized. As digital assets continue to gain acceptance, their role in major financial decisions—such as buying a home—is likely to expand.

Over the next five years, we could see the emergence of hybrid mortgage products that combine traditional income verification with digital asset evaluation. This would create a more flexible and inclusive lending environment, catering to a diverse range of financial profiles.

Technological advancements, including blockchain-based verification systems, could further streamline the process. These systems would allow for secure, transparent, and efficient assessment of crypto holdings, reducing risk for lenders.

At the same time, regulatory clarity will be crucial. Clear guidelines from federal agencies will help standardize practices and build trust among both lenders and borrowers.

A Transformational Shift in the Housing Market

Fannie Mae’s exploration into crypto-integrated mortgages signals a potentially transformative moment for the US real estate market. By bridging the gap between digital assets and traditional finance, this move could redefine how Americans achieve homeownership.

While challenges remain—particularly around volatility, regulation, and security—the potential benefits are substantial. Increased access to financing, modernization of lending practices, and alignment with the digital economy all point toward a more dynamic housing market.

As this trend continues to evolve, it will be essential for both buyers and investors to stay informed. The integration of crypto into mortgages is not just a niche development—it could become a cornerstone of future financial systems.

For those watching the intersection of technology and real estate, one thing is clear: the rules of homeownership are changing, and the impact could be felt for decades to come.

Subscribe to trusted news sites like USnewsSphere.com for continuous updates.