Michael Burry Sounds Alarm: Why Fannie Mae & Freddie Mac IPO Delays Signal Bigger Risks Ahead is quickly becoming one of the most important financial narratives shaping the US housing and credit markets in 2026. As mortgage rates surge to multi-month highs and affordability continues to decline across major US cities, renewed attention is turning to government-backed mortgage giants and the broader risks embedded in the financial system.

Recent discussions among analysts and institutional investors suggest that the long-anticipated public offerings of Fannie Mae and Freddie Mac may not happen until at least 2027. This delay is not just a timing issue—it reflects deeper structural concerns about housing market stability, regulatory uncertainty, and the long-term sustainability of the US mortgage system.

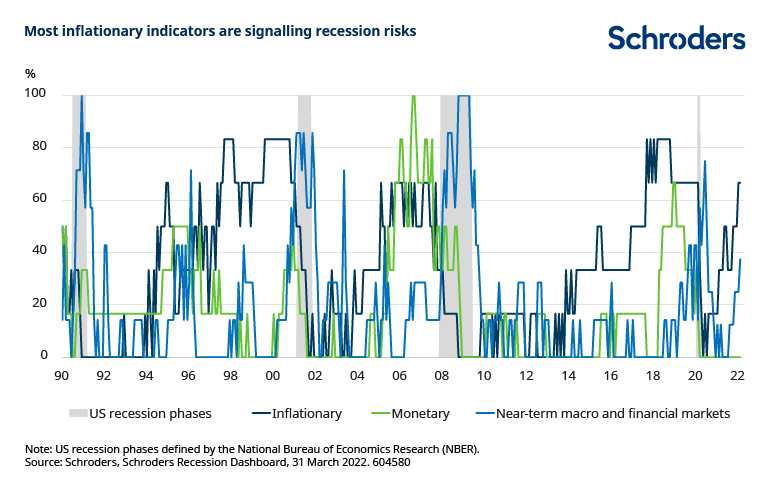

At the same time, macroeconomic pressures such as rising energy prices, geopolitical tensions, and persistent inflation risks are creating a fragile environment where any disruption in housing finance could ripple across the entire economy.

The Role of Fannie Mae and Freddie Mac in the US Economy

Fannie Mae and Freddie Mac are central pillars of the US housing market. These institutions do not directly lend money to homebuyers. Still, they play a crucial role by purchasing mortgages from lenders, packaging them into securities, and ensuring liquidity in the housing system.

This structure allows banks to continue issuing loans, which keeps the housing market functioning efficiently. Without these entities, mortgage availability would shrink significantly, making it harder for Americans to buy homes.

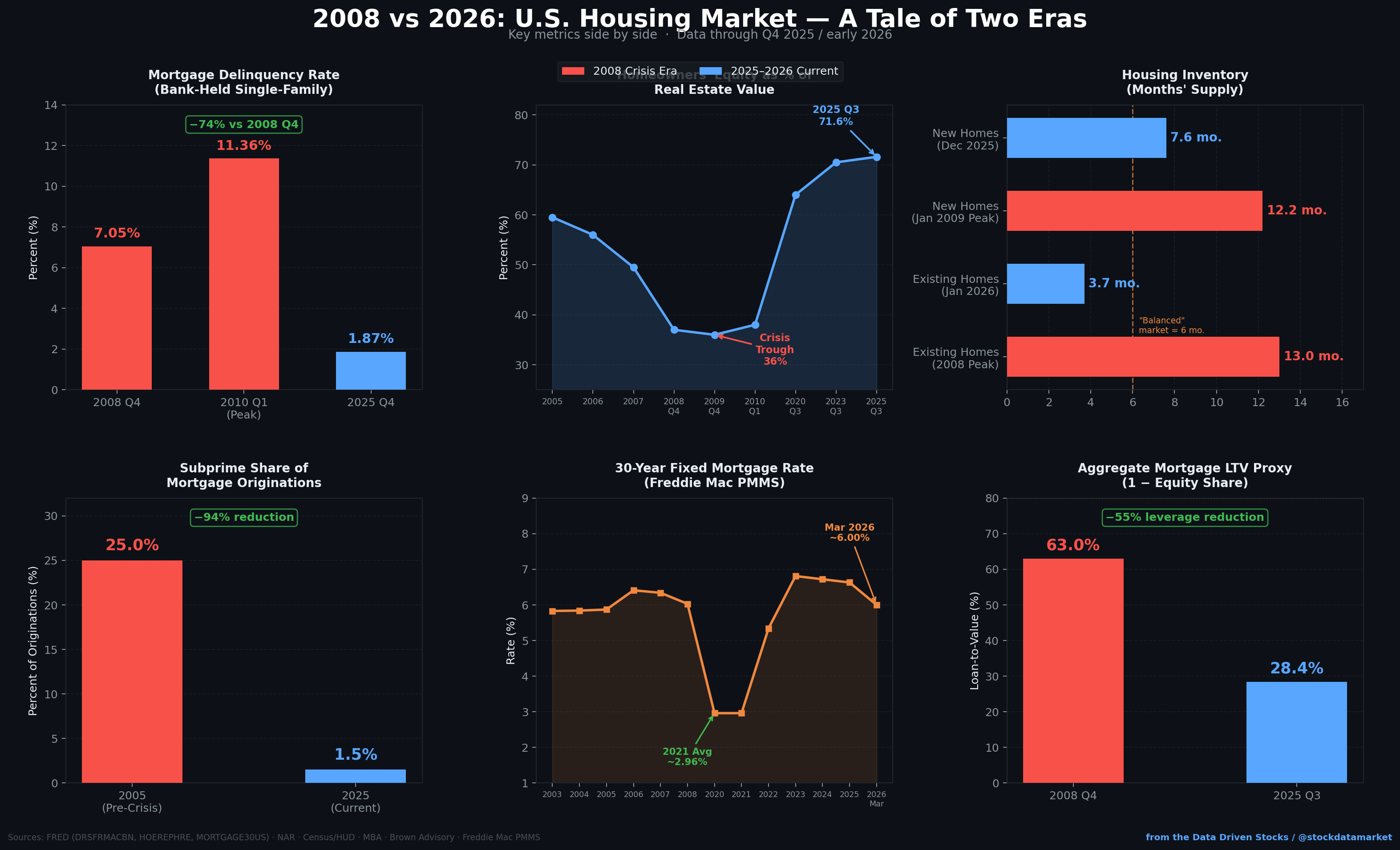

However, since the 2008 financial crisis, both institutions have remained under government conservatorship. While they continue to support the housing market, their unresolved status raises concerns about long-term stability and investor confidence.

The delay in their potential IPOs suggests that policymakers are still grappling with how to balance risk, regulation, and market participation.

Why Michael Burry’s Warning Is Gaining Attention

Michael Burry, widely known for predicting the 2008 housing crash, has once again raised concerns about systemic risks within the financial system. His warning about the delayed IPOs of Fannie Mae and Freddie Mac is being interpreted as a signal that deeper issues may be present beneath the surface.

The concern is not just about the IPO timeline—it’s about what the delay represents. When large-scale financial reforms are postponed, it often indicates unresolved risks or disagreements among regulators and policymakers.

Investors are paying attention because history has shown that delays and uncertainty in financial systems can precede significant market disruptions. Burry’s perspective adds weight to these concerns, especially as current market conditions already reflect heightened volatility.

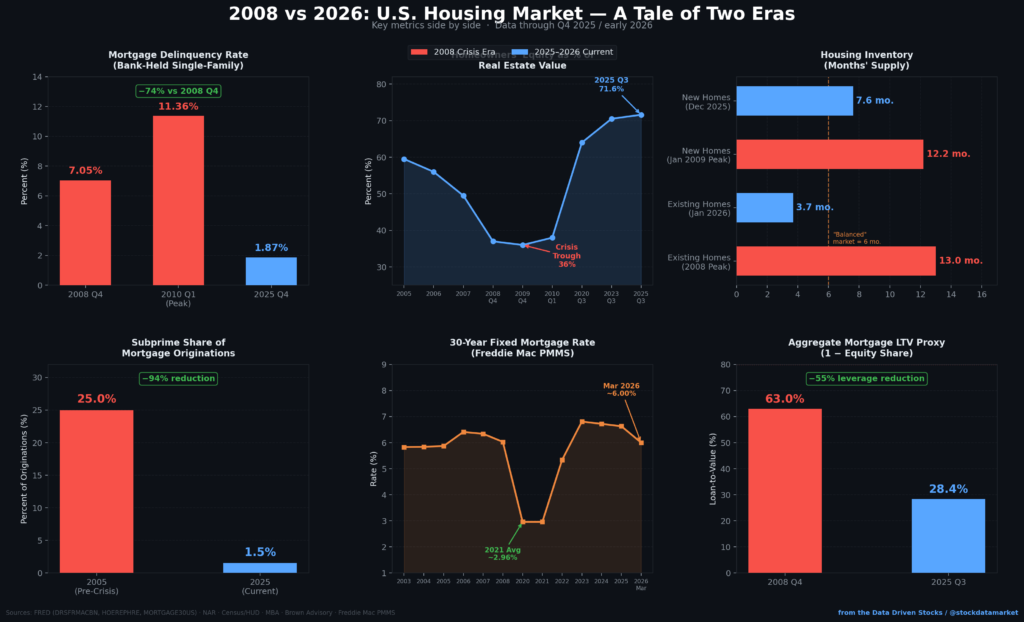

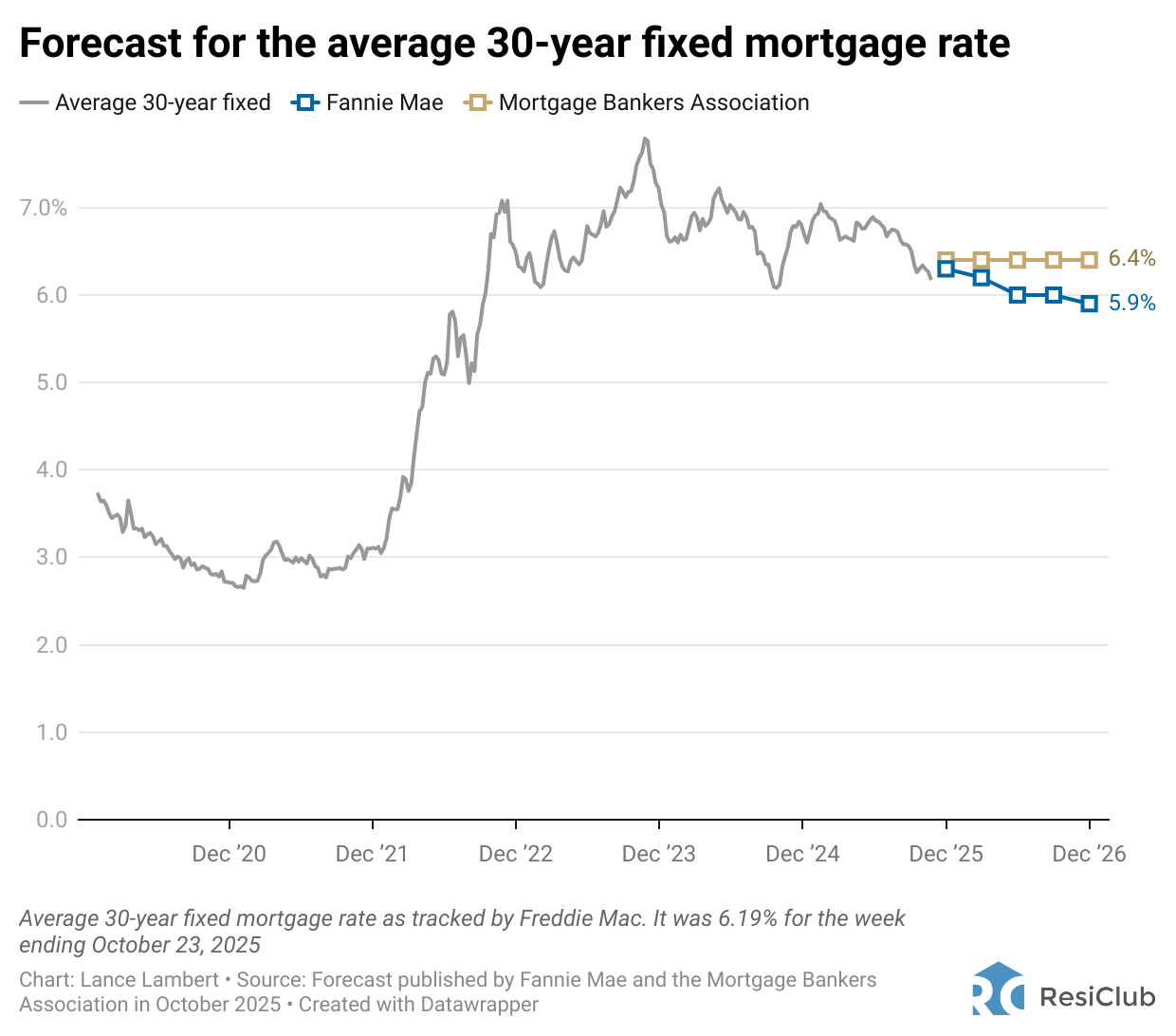

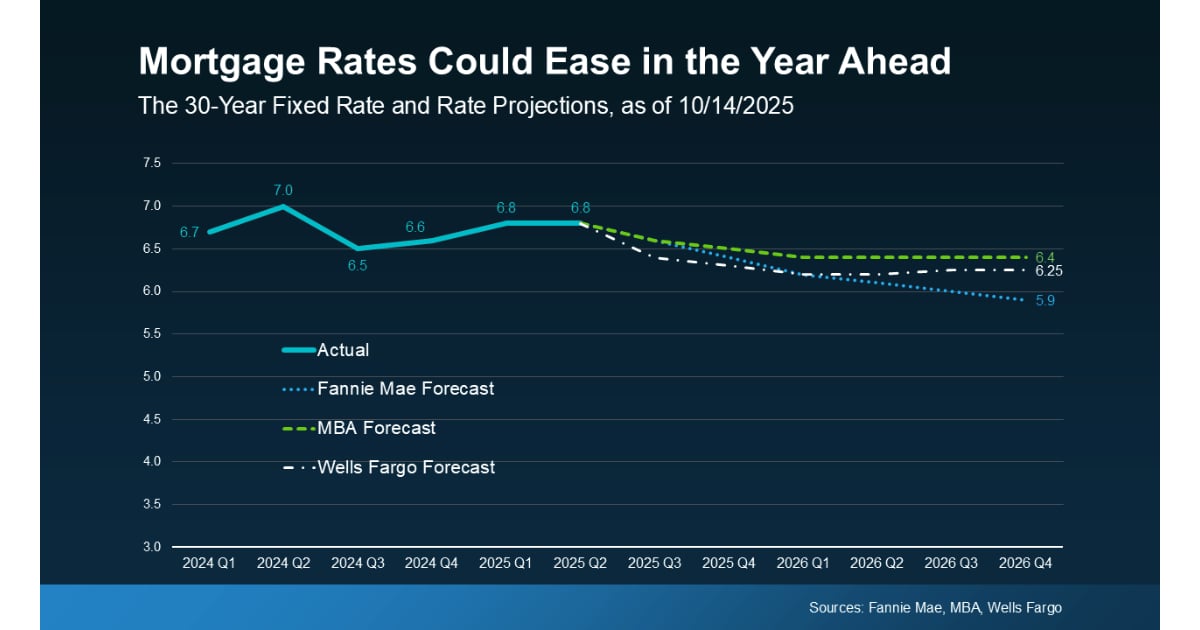

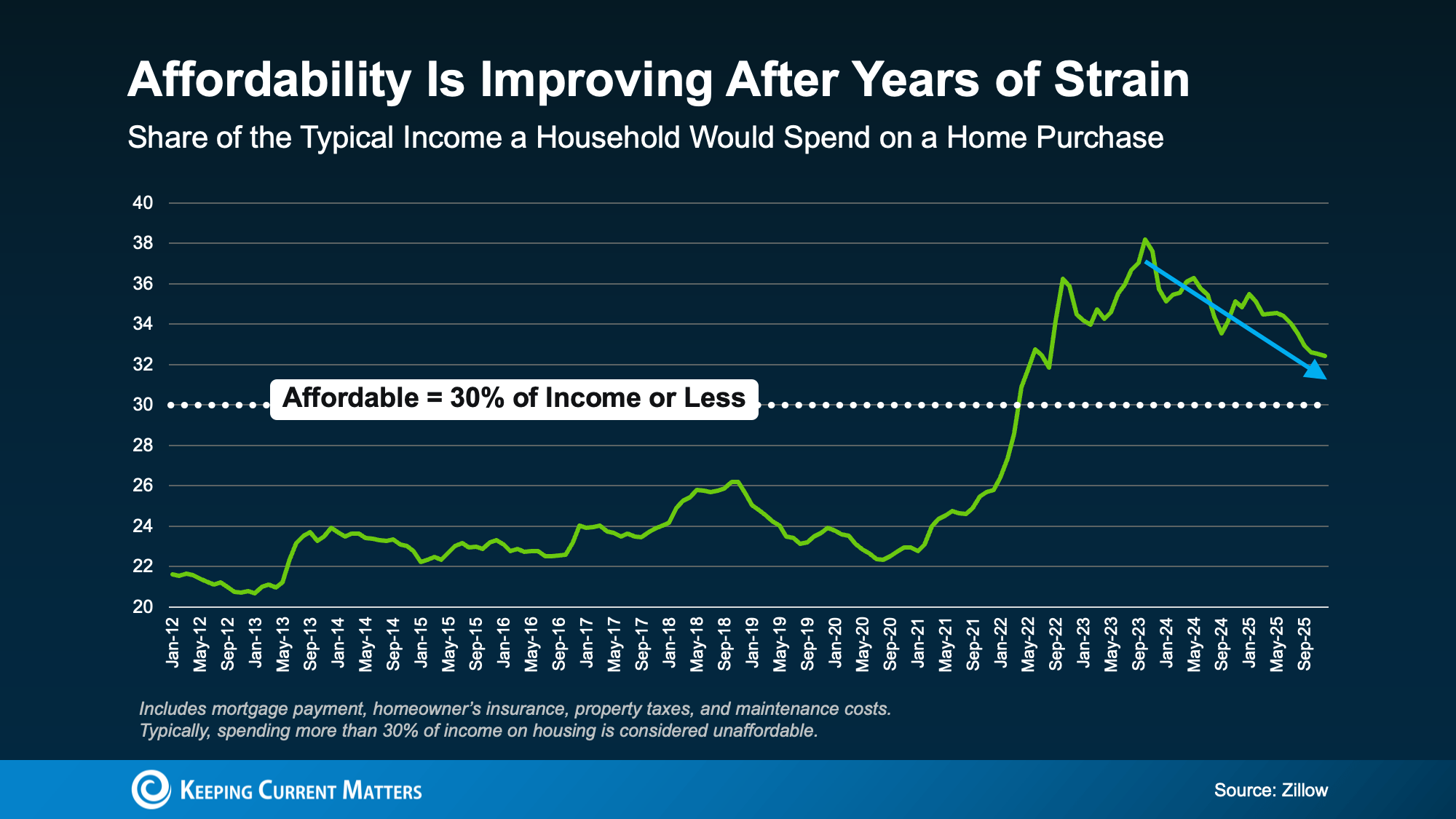

Mortgage Rates Surge and Housing Affordability Crisis

One of the most immediate pressures on the housing market is the sharp increase in mortgage rates. Recent data shows rates climbing to their highest levels in several months, significantly increasing monthly payments for homebuyers.

For many Americans, this has made homeownership increasingly out of reach. Affordability metrics indicate that a growing percentage of households can no longer qualify for traditional mortgages under current conditions.

This slowdown in demand is already impacting housing activity, with fewer home sales and longer listing times. If this trend continues, it could lead to price corrections in certain regions.

The connection between rising rates and delayed IPOs is critical. A weak housing market makes it more difficult to restructure or privatize major mortgage institutions, further complicating the financial landscape.

What IPO Delays Signal About Financial System Risks

The postponement of Fannie Mae and Freddie Mac IPOs raises important questions about the health of the broader financial system. IPOs are typically pursued when market conditions are favorable, and investor confidence is strong.

A delay suggests that current conditions may not support a successful transition to public markets. This could be due to regulatory challenges, valuation concerns, or underlying risks within the mortgage portfolios.

Another key factor is global uncertainty. With geopolitical tensions affecting energy prices and economic stability, policymakers may be hesitant to introduce additional variables into an already complex system.

The risk is that prolonged uncertainty could reduce investor confidence and limit capital flows into the housing market, creating a feedback loop that further weakens economic growth.

Market Outlook: What Investors Should Watch Closely

Looking ahead, several key indicators will determine how this situation unfolds. Mortgage rate trends remain the most important factor, as they directly influence housing demand and affordability.

Investors should also monitor policy decisions related to housing finance reform. Any updates on the status of Fannie Mae and Freddie Mac could significantly impact market sentiment.

Additionally, broader economic signals such as inflation data, employment trends, and consumer confidence will play a role in shaping the outlook.

While some analysts believe the housing market may stabilize, others warn of potential corrections if current pressures persist. This divergence of opinion highlights the level of uncertainty in today’s environment.

Strategic Insights: How Investors Can Position Themselves

In uncertain times, investors must focus on risk management and strategic allocation. Diversification across asset classes remains one of the most effective ways to reduce exposure to specific risks.

Real estate investments should be approached cautiously, especially in markets with high price-to-income ratios. Investors may consider alternative opportunities such as dividend-paying stocks, commodities, or sectors benefiting from current trends like energy and technology.

Monitoring credit markets is also essential. Any signs of stress in mortgage-backed securities or lending activity could indicate broader financial risks.

Long-term investors should focus on fundamentals rather than short-term fluctuations. While volatility may create challenges, it also presents opportunities for disciplined investors to build positions at attractive valuations.

A Warning Sign Investors Should Not Ignore

The delay in Fannie Mae and Freddie Mac IPOs is more than a technical issue—it is a reflection of deeper uncertainties within the US financial system. Combined with rising mortgage rates and affordability challenges, it highlights the fragile balance between growth and risk in today’s economy.

Michael Burry’s warning serves as a reminder that systemic risks often develop quietly before becoming visible to the broader market. Investors who stay informed and proactive will be better positioned to navigate these challenges.

As 2026 unfolds, the intersection of housing finance, interest rates, and global economic conditions will remain a critical area to watch. Understanding these dynamics is essential for making informed investment decisions and protecting long-term wealth.

Subscribe to trusted news sites like USnewsSphere.com for continuous updates.