The U.S. stock market is more than a collection of tickers and price charts—it is a real-time reflection of economic strength, corporate performance, investor psychology, and global capital flows. Every trading day, billions of dollars move based on expectations about inflation, interest rates, earnings growth, geopolitical developments, and technological innovation.

In today’s environment, market direction is shaped by a powerful combination of forces:

- Federal Reserve policy and interest rate expectations

- Inflation trends and labor market strength

- Corporate earnings performance and valuation levels

- Institutional capital flows and retail participation

- Global risks and commodity price movements

- Technological disruption, particularly artificial intelligence

Understanding the U.S. stock market requires connecting these moving parts into a single framework. Headlines may focus on daily volatility, but sustained market trends emerge from structural shifts in liquidity, productivity, and profitability.

Markets are forward-looking. They do not wait for economic data to confirm change—they price expectations in advance. This is why inflation momentum can matter more than inflation levels, and why earnings guidance can outweigh reported results. It is also why investor sentiment, technical structure, and capital positioning often reveal turning points before fundamentals fully shift.

This comprehensive outlook is designed to provide a complete roadmap:

- Where the market stands today

- What economic signals are driving the direction

- How corporate earnings and valuations shape opportunity

- What risks could trigger correction

- Why a bullish expansion scenario remains possible

- How short-term traders and long-term investors should position themselves

Whether you are a daily trader navigating volatility or a long-term investor building wealth for the next decade, understanding the interaction between macroeconomics, corporate performance, and market psychology is essential.

The U.S. market has historically rewarded disciplined investors who combine data-driven analysis with strategic risk management. But success does not come from reacting emotionally to headlines—it comes from understanding the structure behind the moves.

The pages ahead will break down that structure in detail, providing a balanced, forward-looking framework to navigate 2026 and beyond with clarity, discipline, and confidence.

1. Understanding the Current U.S. Stock Market Landscape

The U.S. stock market landscape is not just a collection of price charts—it is a real-time reflection of economic strength, corporate confidence, investor psychology, and global capital movement. Before forming any bullish or bearish opinion, investors must understand the structural condition of the market.

This section breaks down index performance, sector rotation, and sentiment signals in a way that connects price action with underlying economic forces. When you combine these elements, you move from guessing the market’s direction to understanding it.

1.1 Snapshot of Major Index Performance

A serious market outlook always begins with the four core U.S. indices because they represent different segments of the economy.

- S&P 500 – Represents 500 large-cap U.S. companies and acts as the primary benchmark for institutional investors.

- Dow Jones Industrial Average – Tracks 30 major blue-chip corporations, often reflecting traditional industrial strength.

- Nasdaq Composite – Heavy in technology and growth stocks, highly sensitive to interest rate changes.

- Russell 2000 – Focuses on small-cap companies, offering insight into domestic economic strength.

U.S. Stock Market: Daily, Weekly, Monthly, and YTD Performance

To make this section powerful, include:

- Daily percentage move (risk-on or risk-off signal)

- Weekly trend (momentum direction)

- Monthly performance (swing bias)

- Year-to-date return (structural strength)

Explain how divergence matters.

For example:

- If Nasdaq is outperforming while Russell 2000 lags → growth concentration risk.

- If small caps outperform → domestic economic optimism.

- If Dow leads → defensive or dividend rotation.

U.S. Stock Market Breadth: The Hidden Strength Indicator

Price alone can mislead investors. Breadth tells the truth.

Include:

- Advancers vs Decliners ratio

- Percentage of stocks above 50-day and 200-day moving averages

- New highs vs new lows

If indices rise but breadth weakens, it suggests concentration risk.

If breadth expands, the rally has durability.

Professional investors watch breadth before they increase exposure.

52-Week Highs and Lows

This data reveals structural strength.

- Rising 52-week highs → strong bull phase

- Expanding 52-week lows → early warning of correction

- Simultaneous expansion in both → volatile distribution phase

Highlight historical comparison. For example:

During strong bull cycles, 52-week highs consistently outnumber lows by 3:1 or more.

U.S. Stock Market Volume Trends: Institutional Footprint

Volume confirms conviction.

Include:

- Average daily volume vs 30-day average

- Accumulation days vs distribution days

- Volume spikes on breakouts

If price rises on low volume → weak participation.

If price rises on heavy volume → institutional buying.

Remind: retail traders move prices temporarily, institutions move markets structurally.

1.2 Sector Rotation and Capital Flow Trends

Markets do not rise evenly. Capital rotates between sectors based on economic expectations, interest rates, and earnings outlook.

The 11 S&P sectors to analyze:

- Technology

- Financials

- Healthcare

- Consumer Discretionary

- Consumer Staples

- Energy

- Industrials

- Materials

- Utilities

- Real Estate

- Communication Services

Identifying Outperformers and Underperformers

Show a table comparing:

- 1-week performance

- 1-month performance

- YTD performance

- Relative strength vs S&P 500

Explain what leadership means.

For example:

- Tech + Communication Services leading → AI or innovation-driven rally

- Energy leading → inflation or oil price pressure

- Utilities and Staples leading → defensive positioning

Sector leadership tells you what the market expects next.

U.S. Stock Market: ETF Flow Analysis

Track capital using major ETFs:

- SPY (S&P 500 exposure)

- QQQ (Nasdaq 100 exposure)

- IWM (Small-cap exposure)

- XLF (Financial sector)

- XLK (Technology sector)

Include:

- Net inflows/outflows

- Weekly fund flow changes

- Institutional positioning shifts

Heavy inflows into QQQ while SPY stagnates show narrow growth dominance.

Strong inflows into IWM (Small-cap exposure) signal improving economic confidence.

ETF flows are one of the clearest real-time indicators of money movement.

Defensive vs Cyclical Rotation

Explain:

Cyclical sectors:

- Technology

- Industrials

- Consumer Discretionary

- Financials

Defensive sectors:

- Utilities

- Consumer Staples

- Healthcare

If defensives outperform → risk-off environment.

If cyclicals outperform → expansion phase.

This part connects economic data with price behavior.

Growth vs Value Performance Gap

Measure:

- Growth ETF vs Value ETF performance

- Forward P/E premium

- Earnings growth differential

When growth dramatically outperforms value, valuations expand.

When value outperforms, markets are repositioning for stability or rate shifts.

1.3 Market Sentiment Indicators

Markets move not only on data, but on psychology.

Understanding sentiment helps predict turning points before they appear in price.

VIX Levels – The Fear Gauge

The CBOE Volatility Index (VIX) measures expected volatility.

General interpretation:

- Below 15 → complacency

- 15–20 → stable optimism

- 20–30 → elevated uncertainty

- Above 30 → panic phase

Low VIX during record highs may signal complacency risk.

Spiking VIX during pullbacks often creates buying opportunities.

Context is everything.

Put/Call Ratio

Measures options positioning.

- High ratio → excessive fear

- Low ratio → excessive optimism

Extremes often signal reversals.

Professional traders use this as a contrarian indicator.

CNN Fear & Greed Index

U.S. Stock Market: Break down its components:

- Momentum

- Stock price strength

- Breadth

- Options activity

- Junk bond demand

- Safe-haven demand

Explain that extreme greed near market highs can precede pullbacks.

Extreme fear during corrections often marks bottoms.

Retail vs Institutional Positioning

Include:

- Margin debt levels

- 13F institutional filings

- Hedge fund net exposure

- Dark pool activity

When retail aggressively buys while institutions reduce exposure, risk increases.

When institutions accumulate quietly during fear, opportunity emerges.

AAII Sentiment Survey

This weekly survey measures:

- Bullish percentage

- Bearish percentage

- Neutral positioning

Historical extremes:

- 50% bullish → overheated

- 45% bearish → potential bottom zone

These explain that markets often reverse when crowd consensus becomes one-sided.

2. Key Economic Signals Driving the Market

If price action tells you what the market is doing, economic signals tell you why.

Institutional investors do not allocate billions based on headlines—they react to monetary policy, inflation trajectories, labor conditions, and growth momentum.

Understanding these signals allows readers to interpret daily volatility within a broader structural framework. This section connects Federal Reserve policy, inflation trends, employment strength, and GDP growth directly to equity performance—because every major bull market and every major correction in U.S. history has been shaped by these forces.

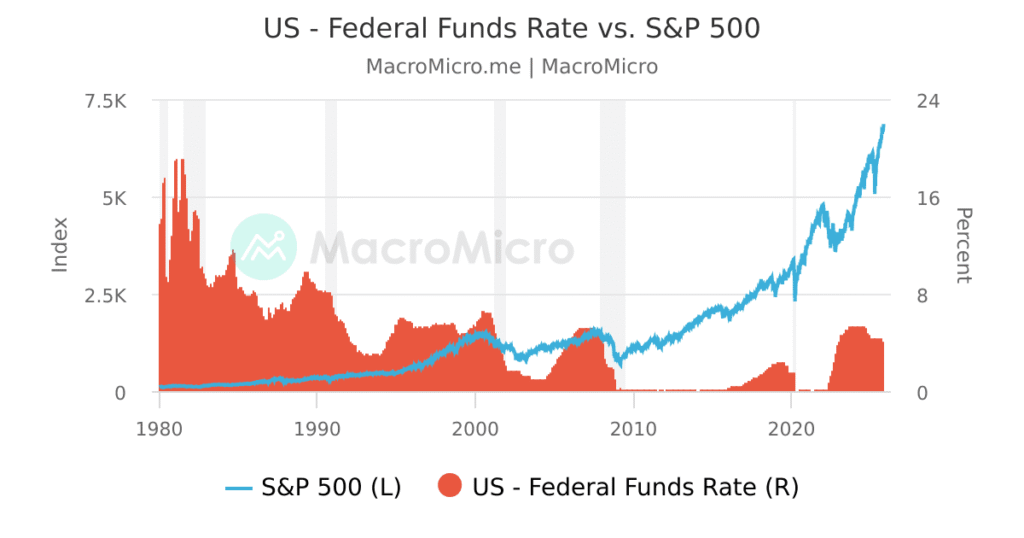

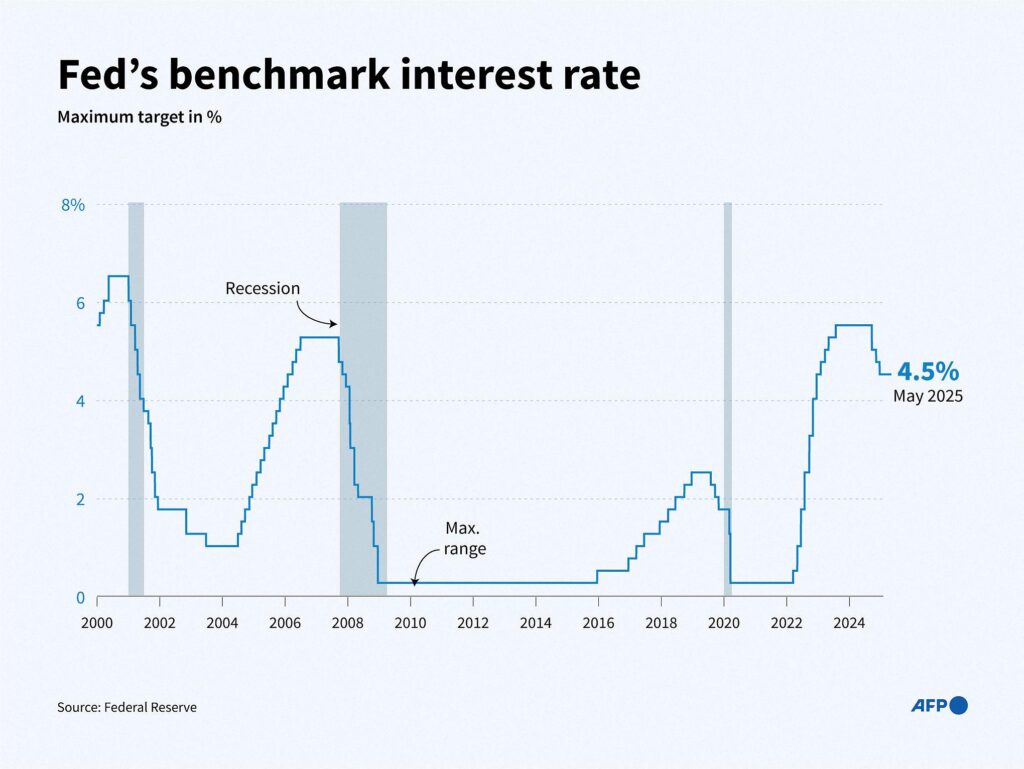

2.1 Federal Reserve Policy and Interest Rate Outlook

No single institution has more influence over U.S. equity markets than the Federal Reserve. Interest rates determine borrowing costs, corporate profitability, valuation multiples, liquidity conditions, and investor risk appetite.

Current Federal Funds Rate

Start by clearly stating:

- The current Fed Funds target range

- How it compares to the past 5–10 years

- Whether the policy is restrictive, neutral, or accommodative

Then explain why this matters:

Higher rates:

- Compress equity valuations (especially growth stocks)

- Increase bond yields, making fixed income more attractive

- Raise corporate borrowing costs

Lower rates:

- Expand P/E multiples

- Boost risk appetite

- Encourage leverage and capital investment

Context is critical. A 5% rate means something very different in a high-growth environment versus a slowing economy.

U.S. Stock Market: Dot Plot Expectations

The Fed’s “dot plot” reveals where policymakers expect rates to move in the coming years.

In your analysis, include:

- Median rate projection for the current year

- Projections for the next 2–3 years

- Long-run neutral rate estimate

Then explain divergence:

- If markets expect aggressive cuts but the dot plot signals fewer cuts → volatility risk.

- If markets are overly pessimistic and the Fed signals easing → upside catalyst.

Highlight how forward expectations drive markets more than current rates.

Commentary from the Federal Reserve

Summarize tone from official statements:

- Hawkish language → inflation concerns remain.

- Dovish language → growth risks rising.

- Data-dependent language → flexibility, but uncertainty.

Investors often react more to tone than policy itself.

Explain how subtle wording changes (for example, replacing “ongoing tightening” with “monitoring conditions”) can shift billions in capital flows within minutes.

Statements from Jerome Powell

The Fed Chair’s press conferences often move markets dramatically.

In this subsection:

Key Themes from Recent Federal Reserve Speeches

Recent speeches from Jerome Powell and other officials at the Federal Reserve have revolved around three dominant themes:

1. “Higher for Longer” Policy Bias

Officials have repeatedly emphasized that inflation remains above target and that policy must stay restrictive until there is sustained evidence of price stability. The phrase “premature easing” has appeared multiple times in commentary, reinforcing the idea that the Fed does not want to repeat the 1970s mistake of cutting rates too early.

2. Data-Dependent Decision Framework

Powell has consistently stated that future rate decisions will depend on incoming economic data, particularly inflation and labor market conditions. This shifts focus from fixed forward guidance to flexible response—making every CPI, payroll, and PCE release a potential volatility trigger.

3. Balancing Inflation Risk vs. Economic Slowdown

Recent remarks increasingly acknowledge the risk of overtightening. While inflation control remains the priority, officials have begun referencing “two-sided risks”—suggesting awareness that excessive restriction could weaken growth more than intended.

These themes collectively signal a Fed that is cautious, vigilant, and unwilling to declare victory prematurely.

Consistency vs. Shift in Messaging

A deeper analysis reveals subtle but important shifts.

Earlier Phase (Hawkish Emphasis):

- Strong focus on inflation persistence

- Minimal concern about growth slowdown

- Repeated commitment to further tightening

Recent Phase (Balanced Tone):

- Greater acknowledgment of cooling inflation trends

- Increased reference to lagged effects of policy

- Recognition that real rates are already restrictive

The shift is not dramatic, but tone matters.

Markets react to nuance:

- Replacing “additional hikes likely” with “prepared to adjust if necessary.”

- Acknowledging “disinflation progress.”

- Referencing improving supply chains

These incremental adjustments often signal that the tightening cycle is maturing—even if no official pivot has been announced.

Professional investors monitor language changes word by word because policy inflection points are usually communicated subtly before they are executed formally.

How Markets Responded Intraday

Intraday reactions to Powell’s speeches often follow a predictable pattern:

Phase 1: Immediate Algorithmic Reaction (First 5–10 Minutes)

High-frequency trading systems scan keywords like:

- “Inflation”

- “Persistent”

- “Restrictive”

- “Easing”

- “Balanced”

If tone appears hawkish:

- Treasury yields spike

- Nasdaq drops sharply

- Dollar strengthens

If tone appears dovish:

- Bond yields fall

- Growth stocks rally

- Small caps outperform

Phase 2: Human Reassessment (Next 1–2 Hours)

Institutional desks reassess the full context:

- Did Powell actually shift policy bias?

- Is this new information or reinforcement of prior guidance?

- Does this change terminal rate expectations?

This second wave often reverses the initial algorithm-driven move.

Phase 3: Closing Session Positioning

Large asset managers adjust positioning before the close:

- Hedging exposure

- Rolling options positions

- Adjusting sector allocation

If the speech signals a prolonged tight policy:

- Defensive sectors outperform

- Utilities and healthcare gain

- Growth underperforms

If the speech hints at policy easing:

- Technology rallies strongly

- Small caps see aggressive buying

- Financial conditions loosen rapidly

Why This Matters for Investors

Fed communication shapes:

- Liquidity expectations

- Valuation multiples

- Risk appetite

- Sector leadership

The most important takeaway:

Markets do not wait for rate cuts—they move on expectations.

The shift in tone often precedes the shift in policy.

By carefully tracking language consistency, subtle tone changes, and real-time market reactions, investors gain a forward-looking edge rather than reacting after the move has already occurred.

Powell’s credibility matters. If markets believe inflation is under control, equities stabilize. If confidence weakens, volatility rises.

Key Themes from Recent Federal Reserve Speeches

Recent speeches from Jerome Powell and other officials at the Federal Reserve reveal a clear and carefully balanced message. While headlines often focus on single phrases, the broader communication strategy shows a central bank that is firm on inflation control but increasingly aware of economic risks.

Three dominant themes stand out.

1. “Higher for Longer” Policy Bias

The Fed continues to emphasize that inflation remains above its 2% target. Powell has repeatedly warned against “premature easing,” signaling that cutting rates too early could reignite inflation pressures—similar to policy mistakes made during the 1970s.

In simple terms, this means:

- The Fed prefers to keep rates elevated longer than markets might expect.

- Officials want sustained proof that inflation is truly under control.

- A single soft inflation report is not enough to trigger policy easing.

For investors, this reinforces the idea that liquidity will not return quickly unless inflation clearly trends lower for several months.

2. Data-Dependent Decision Framework

Powell has consistently described policy decisions as “data dependent.” Instead of committing to a fixed path of hikes or cuts, the Fed now adjusts based on incoming economic information.

This shifts market focus toward:

- CPI (inflation data)

- PCE (the Fed’s preferred inflation gauge)

- Nonfarm payrolls

- Wage growth

Because of this approach, every major economic release becomes a potential volatility catalyst. Markets no longer rely on forward guidance alone—they respond to each data print in real time.

In practical terms, this means:

- Strong inflation data can delay rate cuts.

- Weak labor data can increase easing expectations.

- Mixed data creates uncertainty and higher volatility.

3. Balancing Inflation Risk vs. Economic Slowdown

More recently, speeches have begun acknowledging “two-sided risks.” While inflation remains the primary concern, officials are increasingly recognizing that keeping rates too high for too long could damage economic growth.

This subtle shift does not signal an immediate pivot—but it suggests awareness that policy is already restrictive.

Investors should pay attention to phrases such as:

- “Lagged effects of tightening”

- “Monitoring financial conditions.”

- “Balanced risks”

When these phrases appear more frequently, it often means the tightening cycle is approaching maturity.

Consistency vs. Shift in Messaging

To understand the full picture, it helps to compare earlier speeches with more recent ones.

Earlier Phase: Strongly Hawkish

In the earlier stage of the tightening cycle, communication was clear and firm:

- Heavy emphasis on persistent inflation.

- Little discussion of growth risks.

- Repeated commitment to further rate increases.

The goal at that time was credibility—convincing markets that inflation control was non-negotiable.

Recent Phase: More Balanced Tone

More recent remarks reflect subtle adjustments:

- Greater acknowledgment of moderating inflation trends.

- Increased discussion of the delayed impact of past rate hikes.

- Recognition that real interest rates are already restrictive.

The shift is not dramatic—but tone matters greatly in financial markets.

Replacing “additional hikes likely” with “prepared to adjust if necessary” may seem minor. However, to institutional investors, such language often signals that policy tightening is nearing its end—even if no formal pivot has been announced.

Professional investors analyze Fed communication word by word because major policy turning points are usually hinted at before they are officially declared.

How Markets Responded Intraday

Market reactions to Powell’s speeches typically unfold in three stages.

Phase 1: Immediate Algorithmic Reaction (First 5–10 Minutes)

High-frequency trading systems instantly scan for key terms such as:

- “Inflation”

- “Persistent”

- “Restrictive”

- “Easing”

- “Balanced”

If the tone appears hawkish:

- Treasury yields rise sharply.

- The Nasdaq Composite often falls quickly.

- The U.S. dollar strengthens.

If the tone appears dovish:

- Bond yields decline.

- Growth stocks rally.

- Small-cap stocks outperform.

This initial move is often fast and exaggerated because it is driven by automated systems.

Phase 2: Institutional Reassessment (Next 1–2 Hours)

After the initial reaction, human traders and institutional desks reassess:

- Did Powell truly change policy direction?

- Was the language new or consistent with previous guidance?

- Does this alter expectations for the terminal rate?

This second phase sometimes reverses the early move if the market overreacted to isolated wording.

Phase 3: Closing Positioning

Before the market closes, large asset managers adjust exposure based on the broader interpretation.

If the speech signals a prolonged tight policy:

- Defensive sectors such as utilities and healthcare tend to outperform.

- High-growth technology may lag.

- Bond yields remain elevated.

If the speech hints at easing:

- Technology and cyclical stocks often rally.

- Small caps may gain momentum.

- Financial conditions loosen as yields decline.

This closing session behavior often reveals how seriously institutional investors interpret the message.

Why This Matters for Investors

Federal Reserve communication directly influences:

- Liquidity conditions

- Valuation multiples

- Risk appetite

- Sector leadership

The most important lesson for readers is this:

Markets do not wait for actual rate cuts—they move on expectations.

Often, equity markets begin rallying months before the first rate cut if investors believe easing is coming. Conversely, markets can decline even without new hikes if investors fear rates will remain elevated longer than expected.

By tracking consistency, tone shifts, and real-time market reactions, investors gain a forward-looking advantage. Instead of reacting after policy changes are official, they position themselves ahead of them.

Understanding Fed communication is not about predicting exact rate moves. It is about recognizing when the narrative begins to change—because that is when markets usually begin to move.

Rate Cut / Hike Probabilities

Understanding where interest rates are today is important.

Understanding where markets believe rates are heading is far more powerful.

Equity markets are forward-looking. Prices move based on expectations, not current policy. That is why tracking rate cut and hike probabilities is essential for any serious market outlook.

CME FedWatch Probabilities

The most widely followed tool for rate expectations is the CME FedWatch Tool. It calculates the probability of future rate changes based on federal funds futures contracts.

In simple terms, it shows:

- The percentage chance of a rate cut at the next meeting

- The probability of rates staying unchanged

- The likelihood of multiple cuts or hikes over coming meetings

For example:

- If markets price a 70% probability of a rate cut in three months, equities may rally even before the cut happens.

- If probabilities shift suddenly from 60% chance of cuts to 30%, volatility can increase immediately.

These probabilities update in real time as bond traders reposition.

The key insight:

Markets do not wait for the Federal Reserve to act—they react to changes in probability.

Market-Implied Rate Expectations

Beyond individual meeting probabilities, investors track:

- Terminal rate expectations (the highest rate in the cycle)

- Total cuts priced in over the next 6–12 months

- Forward curve expectations

If markets expect:

- 4 rate cuts next year → growth stocks often outperform.

- Fewer cuts than previously priced → yields rise and equities may pull back.

When expectations shift, valuation models adjust quickly.

Lower expected rates increase the present value of future earnings—boosting stock prices, especially for high-growth companies.

This is why a single inflation report can change billions in market capitalization within hours.

Bond Market Yield Curve Interpretation

The yield curve is one of the clearest signals of rate expectations.

It compares yields on short-term bonds (2-year Treasury) with long-term bonds (10-year Treasury).

Three major scenarios matter:

- Inverted Yield Curve (2-year > 10-year)

- Signals expectations of slowing growth or future rate cuts

- Historically precedes recessions

- Often pressures financial stocks

- Steepening Yield Curve (10-year rising faster than 2-year)

- Suggests improving growth outlook

- Supports financial sector earnings

- Indicates easing recession fears

- Bull Steepening (Short-term yields falling faster than long-term)

- Usually happens when markets anticipate aggressive rate cuts

- Often boosts growth sectors

The bond market often predicts economic turning points before stock markets fully react.

How Rate Expectations Affect Sectors Differently

Interest rate expectations do not impact all sectors equally. This is where macro policy connects directly to sector rotation.

Technology – Highly Sensitive to Rate Expectations

Technology stocks depend heavily on future earnings growth.

When rates fall:

- Future profits are discounted at a lower rate.

- Valuations expand.

- Growth stocks rally strongly.

When rates rise or cuts are delayed:

- Valuation multiples compress.

- Nasdaq often underperforms.

This is why the Nasdaq Composite tends to react more aggressively than other indices during Fed-driven volatility.

Financials – Benefit from a Steep Yield Curve

Banks and financial institutions profit from the spread between short-term and long-term rates.

If the yield curve steepens:

- Banks can borrow short-term at lower rates.

- Lend long-term at higher rates.

- Net interest margins improve.

If the curve inverts:

- Profitability pressure increases.

- Lending slows.

- Financial stocks often underperform.

Thus, expectations of rate cuts that steepen the curve can benefit financials—if growth remains stable.

Utilities – Sensitive to Bond Competition

Utilities are often treated like bond substitutes because:

- They pay steady dividends.

- They offer stable earnings.

When bond yields rise:

- Investors may prefer safer Treasuries.

- Utilities can underperform.

When yields fall:

- Dividend-paying utilities become more attractive.

- Capital rotates back into defensive sectors.

Utilities often outperform in falling rate environments combined with economic uncertainty.

Why This Section Matters

Rate expectations drive:

- Valuation multiples

- Sector leadership

- Capital flows

- Risk appetite

Even before the Federal Reserve officially cuts or hikes rates, shifts in probabilities reshape portfolios across Wall Street.

By analyzing:

- CME FedWatch data

- Market-implied rate paths

- Yield curve behavior

You connect macro policy directly to sector rotation and index performance.

Historical Impact on Equities

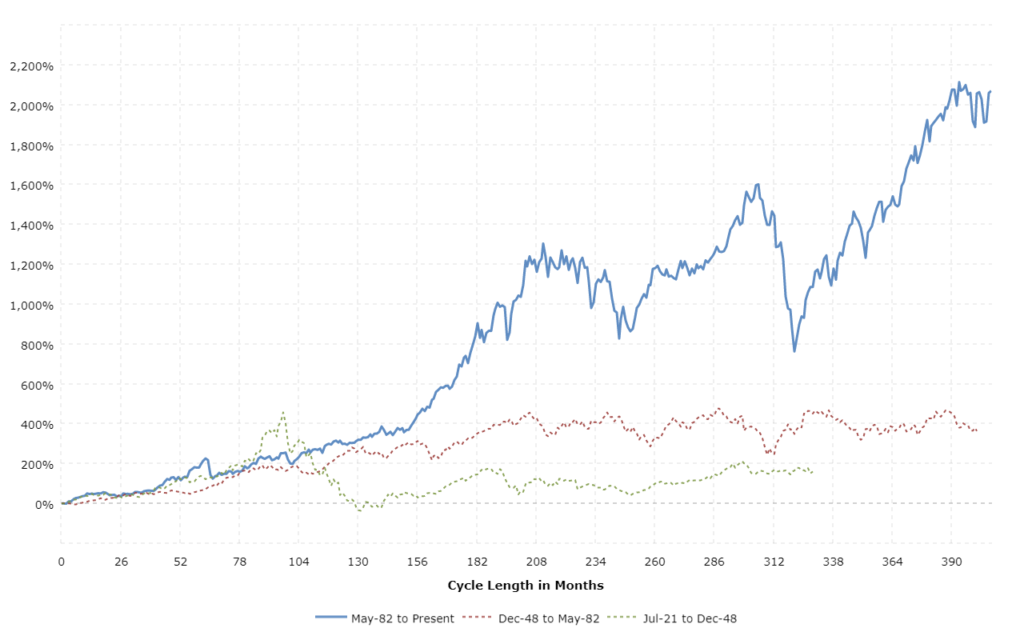

To truly understand how monetary policy shapes the stock market, investors must look beyond short-term headlines and study history. Every major bull market and every major correction in modern financial history has been influenced by interest rate cycles driven by the Federal Reserve.

The relationship between rates and equities follows clear historical patterns. While each cycle is unique, the structure of market reactions tends to repeat.

1. Rate Hiking Cycles Typically Compress Valuations

When the Federal Reserve raises interest rates, the cost of money increases across the economy. Borrowing becomes more expensive, liquidity tightens, and financial conditions become restrictive.

For equities, this primarily affects valuation multiples.

Stock prices are based on the present value of future earnings. When rates rise:

- The discount rate applied to future cash flows increases.

- The present value of long-term earnings decreases.

- Price-to-earnings (P/E) ratios contract.

This is why growth stocks—especially in technology—often underperform during aggressive hiking cycles. Their valuations depend heavily on profits expected years into the future.

Historical examples show:

- During the 2018 tightening cycle, equity multiples contracted sharply.

- In 2022, rapid rate hikes led to one of the fastest valuation compressions in decades, particularly in high-growth sectors.

It is important to understand:

Markets do not decline only because earnings fall. Often, they decline because valuations compress while earnings remain stable.

2. Early Easing Cycles Often Coincide with Economic Stress

Many investors assume that rate cuts are automatically bullish. History shows the reality is more nuanced.

In several cycles, the first rate cut occurred not during economic strength, but during emerging weakness.

For example:

- The Fed began cutting rates in 2001 as the economy entered recession.

- In 2007, cuts started as financial stress intensified.

- In early 2020, emergency cuts followed severe economic disruption.

In these situations:

- Markets may initially fall despite rate cuts.

- Investors worry that the Fed is responding to deeper economic problems.

- Earnings expectations decline rapidly.

Early cuts often signal that economic conditions have deteriorated enough to require policy support.

This is why understanding why the Fed is cutting matters more than the cut itself.

3. Markets Tend to Rally Before the First Rate Cut If Inflation Is Falling

One of the most important historical patterns is this:

Equities often begin rallying months before the first official rate cut—provided inflation is clearly trending lower.

Why?

Because markets are forward-looking.

If investors believe:

- Inflation is under control,

- Rate hikes are finished,

- Policy easing is coming,

They begin positioning ahead of the policy shift.

The rally often begins when:

- Bond yields peak.

- Rate hike probabilities collapse.

- Economic data stabilizes, even if still weak.

By the time the first rate cut is announced, a significant portion of the rally may already have occurred.

This pattern reflects anticipation, not reaction.

Equities Are Forward-Looking

The stock market typically bottoms before economic data improves.

Historically:

- Markets bottomed in March 2009, while unemployment continued rising for months afterward.

- Markets began recovering in late 2022 before inflation had fully returned to target.

- In prior recessions, equity indices turned upward several months before GDP growth resumed.

This happens because:

Markets price expectations of future earnings, not current conditions.

If investors believe:

- The worst is over,

- Policy tightening has ended,

- Liquidity conditions will improve,

They begin buying before the economic data confirms recovery.

By the time headlines turn positive, the opportunity is often partially priced in.

Why Policy Expectations Matter More Than Current Headlines

Daily headlines focus on:

- Current inflation prints

- Current unemployment rates

- Current GDP data

But markets focus on trajectory.

Is inflation accelerating or decelerating?

Are rate expectations rising or falling?

Is the yield curve stabilizing or worsening?

Shifts in expectations drive:

- Bond yields

- Valuation multiples

- Sector leadership

- Risk appetite

This is why a single speech from Jerome Powell can move markets more than a confirmed economic report.

The market moves when the narrative changes—not when the data confirms what everyone already knows.

The Core Insight for Investors

Understanding interest rate cycles is not about predicting the exact date of the next Federal Reserve decision. It is about understanding how policy shifts reshape valuations, liquidity, and investor psychology.

When you step back and study history, four powerful truths consistently emerge.

Hiking Cycles Pressure Valuations

When the Federal Reserve raises interest rates, the impact is not limited to borrowing costs. It changes how investors calculate the value of future earnings.

Higher rates mean:

- Future profits are discounted at a higher rate.

- Valuation multiples contract.

- Risk assets face tighter financial conditions.

Even if corporate earnings remain stable, stock prices can decline simply because the market is no longer willing to pay the same premium for growth.

This is why rate-hiking cycles often lead to:

- Lower price-to-earnings ratios

- Increased volatility

- Greater selectivity in sector performance

The pressure begins not when rates peak—but when investors believe they will continue rising.

Early Cuts Can Signal Stress

Rate cuts are often misunderstood as automatically bullish. In reality, the first cut frequently occurs because economic stress is emerging.

Historically, early easing phases have coincided with:

- Slowing economic growth

- Rising unemployment

- Credit market strain

When the Fed cuts aggressively, it can signal that conditions have deteriorated enough to require intervention.

Markets may initially react positively, but if earnings expectations are falling at the same time, equity gains can be limited or volatile.

The context behind the cut matters more than the cut itself.

Markets Often Rally Before Policy Officially Shifts

One of the most important patterns in financial history is this:

Markets move in anticipation.

Equities frequently begin rising:

- Before the first rate cut

- Before inflation returns fully to target

- Before the economic data clearly improves

Why?

Because markets price the future, not the present.

If investors believe inflation is declining and the tightening cycle is ending, capital begins flowing back into equities ahead of official confirmation.

By the time policy actually changes, much of the move may already be underway.

This forward-looking behavior explains why market bottoms often occur while economic headlines still look negative.

Expectations Drive Prices More Than Current Data

Financial markets are expectation machines.

A strong inflation report may not hurt stocks if investors expected worse.

A moderate jobs report can cause volatility if markets were pricing stronger growth.

Prices adjust to surprises—not simply to numbers.

This is why:

- Changes in rate cut probabilities move markets instantly.

- Subtle language shifts from Jerome Powell can trigger intraday volatility.

- Bond yield movements often precede equity direction.

Investors who focus only on current data risk reacting too late. Those who monitor shifts in expectations gain an advantage.

The Strategic Takeaway

Successful investing during rate cycles requires understanding the sequence:

- Inflation trends shift.

- Rate expectations adjust.

- Bond yields react.

- Valuations reprice.

- Sector leadership changes.

By the time headlines confirm the shift, markets have already moved.

The core insight is simple but powerful:

It is not the policy action itself that drives equities—it is the change in expectations about future policy.

Investors who track that change position themselves ahead of the crowd rather than behind it.

2.2 Inflation Trends (CPI, PPI, Core Inflation)

Inflation is the central driver of Federal Reserve policy. When inflation accelerates, tightening follows. When inflation moderates, easing becomes possible.

Understanding inflation components helps investors anticipate policy shifts before they occur.

Latest CPI Data

The Consumer Price Index (CPI) is one of the most influential economic reports in global financial markets. Released monthly, it measures the change in prices paid by consumers for goods and services—and it directly shapes expectations for Federal Reserve policy, bond yields, and equity valuations.

Serious investors do not just look at the headline number. They analyze CPI through three key lenses: month-over-month change, year-over-year change, and the multi-month trend.

Month-over-Month Change

The month-over-month (MoM) figure shows how much prices increased or decreased compared to the previous month.

This is the most sensitive measure because it reflects the most recent momentum in inflation.

For example:

- A 0.2% monthly increase suggests moderate price pressure.

- A 0.4% or higher monthly reading can signal re-acceleration.

- A 0.1% or flat reading may indicate cooling momentum.

Why this matters:

If inflation runs at 0.4% per month consistently, that annualizes to nearly 5%—well above the Federal Reserve’s 2% target. Even if the year-over-year number looks stable, accelerating monthly readings can alarm policymakers and markets.

Markets react quickly to MoM data because it signals whether inflation is gaining or losing speed right now—not six months ago.

Year-over-Year Change

The year-over-year (YoY) figure compares current prices to the same month one year earlier.

This is the most widely cited number in media coverage because it reflects the broader inflation environment.

However, YoY data has a lag effect:

- It can fall simply because high readings from the prior year are dropping out of the calculation.

- It may not fully reflect recent acceleration or deceleration.

For example:

- If YoY inflation falls from 4% to 3%, that appears positive.

- But if the last three monthly readings were accelerating, the improvement may be temporary.

Serious analysis compares both MoM and YoY to determine whether the headline decline is structurally meaningful or mathematically driven by base effects.

Trend Direction Over the Past Six Months

Single reports can mislead. Trend analysis provides clarity.

Investors should examine:

- Is the three-month average rising or falling?

- Is the six-month annualized rate above or below the Fed’s target?

- Are core components consistently cooling?

If the six-month trend shows steady moderation, markets gain confidence that inflation is moving sustainably toward the target.

If inflation fluctuates unpredictably—one soft report followed by a hot report—it creates uncertainty, which increases volatility.

Consistency builds market confidence. Instability increases risk premiums.

Is Inflation Re-Accelerating, Stabilizing, or Declining?

After reviewing the data, investors must classify the inflation environment.

Re-Accelerating Inflation

Signals:

- Rising month-over-month readings for consecutive months.

- Core inflation is trending higher.

- Sticky services inflation.

Implications:

- Rate cut expectations decrease.

- Bond yields rise.

- Growth stocks often face valuation pressure.

- Volatility increases.

Markets fear that the Federal Reserve may need to maintain restrictive policy longer than expected.

Stabilizing Inflation

Signals:

- MoM readings are fluctuating but not trending upward.

- YoY is gradually drifting lower.

- Core measures steady.

Implications:

- Rate expectations remain stable.

- Market volatility moderates.

- Sector leadership becomes more balanced.

This environment often supports range-bound equity markets rather than strong directional moves.

Consistently Declining Inflation

Signals:

- Multiple months of subdued MoM increases.

- Six-month annualized inflation is trending toward 2%.

- Broad-based cooling across goods and services.

Implications:

- Rate cut probabilities increase.

- Bond yields decline.

- Equity valuations expand.

- Risk appetite improves.

This is the most supportive scenario for sustained equity rallies—provided economic growth remains intact.

Why Markets React to Surprises, Not Just Numbers

One of the most misunderstood aspects of CPI reactions is this:

Markets move based on expectations versus reality—not absolute levels.

For example:

- If inflation comes in at 3%, but markets expected 3.3%, equities may rally.

- If inflation prints 2.8%, but expectations were 2.5%, stocks may fall.

The key driver is the “surprise factor.”

Bond traders, equity investors, and algorithmic systems compare actual data with consensus forecasts within seconds. If inflation is hotter than expected:

- Treasury yields spike.

- Rate cut probabilities decline.

- High-growth stocks sell off.

If inflation is cooler than expected:

- Yields fall.

- Risk assets rally.

- Financial conditions ease.

The magnitude of the surprise often matters more than the level itself.

The Bigger Strategic Picture

CPI data influences:

- Federal Reserve rate expectations

- Bond market positioning

- Sector rotation

- Equity valuation multiples

But the most important insight is this:

Markets do not react to inflation—they react to changes in inflation momentum and shifts in expectations.

If inflation is clearly trending lower and surprises are consistently soft, equities typically benefit even before official rate cuts begin.

If inflation shows signs of re-acceleration, markets quickly adjust for tighter policy—often before the Federal Reserve formally responds.

Understanding CPI analysis at this structural level allows investors to interpret market moves intelligently rather than emotionally.

Core vs Headline Inflation

To understand inflation properly, investors must distinguish between headline CPI and core CPI. Both numbers are released together, but they tell very different stories about the economy.

Markets often react within seconds of the CPI release—but professional investors look beyond the headline figure to understand what is truly happening beneath the surface.

What Is Headline CPI?

Headline CPI measures the total change in consumer prices across the economy. It includes all major categories of goods and services, including:

- Food

- Energy

Because it captures everything consumers pay for, headline CPI reflects the real-world cost pressures households experience.

If gasoline prices surge or grocery costs jump sharply, headline CPI will move higher—even if other components remain stable.

Headline CPI is important because:

- It affects consumer sentiment.

- It influences political and social discussions.

- It directly impacts household budgets.

However, it can be highly volatile month to month.

What Is Core CPI?

Core CPI removes the most volatile components:

- Food

- Energy

The reason for excluding these categories is simple: they fluctuate frequently due to factors outside monetary policy control, such as:

- Oil supply disruptions

- Weather conditions

- Geopolitical tensions

- Agricultural output swings

By excluding food and energy, core CPI aims to measure the underlying, persistent inflation trend across housing, services, healthcare, transportation, and other categories.

Core inflation typically moves more slowly and is less influenced by temporary shocks.

Why the Federal Reserve Focuses on Core Inflation

The Federal Reserve places greater emphasis on core measures because monetary policy works with a lag and cannot quickly offset short-term commodity swings.

There are two key reasons:

1. Core Better Reflects Underlying Inflation Trends

Core inflation shows whether pricing pressure is broad-based and persistent.

If core inflation is rising:

- Businesses are passing on higher costs.

- Wage growth may be fueling service inflation.

- Price increases are spreading across multiple sectors.

This type of inflation is harder to reverse and requires sustained policy action.

If core inflation is steadily declining:

- Disinflation is becoming embedded.

- Rate cuts become more plausible.

- Market confidence improves.

For policymakers, the durability of inflation matters more than short-term spikes.

2. Energy Spikes Can Distort Short-Term Data

Energy prices can swing sharply due to global events.

For example:

- Oil production cuts can lift gasoline prices.

- Natural disasters can disrupt supply chains.

- Geopolitical tensions can drive crude oil higher overnight.

These movements can temporarily push headline CPI higher—even if underlying inflation is stable or falling.

If policymakers reacted aggressively to every oil-driven spike, monetary policy would become unstable.

Core CPI helps filter out these distortions and focus on sustained price trends.

The Market Impact: When Headline and Core Diverge

The most important insight for investors is what happens when headline and core move in different directions.

Scenario 1: Headline Falls, Core Remains Sticky

This is one of the most challenging environments.

If gasoline prices decline and headline inflation drops, headlines may look positive. However, if core inflation remains elevated—particularly in services and shelter—policymakers may remain cautious.

In this case:

- Rate cut expectations may not increase significantly.

- Bond yields may remain elevated.

- Equity markets may struggle to sustain rallies.

Markets quickly realize that surface-level improvement does not necessarily mean policy relief.

Scenario 2: Both Headline and Core Decline Consistently

This is the most supportive scenario for equities.

When both measures show sustained moderation:

- Rate cut probabilities rise.

- Bond yields typically decline.

- Valuation multiples expand.

- Risk appetite improves.

Confidence grows that inflation is structurally under control.

Scenario 3: Headline Rises Due to Energy, Core Stable

If headline inflation rises because of oil prices but core remains stable:

- Markets may initially react negatively.

- However, bond markets often stabilize if core trends remain contained.

- Volatility may fade quickly.

Investors differentiate between temporary commodity shocks and structural inflation pressure.

The Strategic Takeaway

Headline CPI reflects what consumers feel.

Core CPI reflects what policymakers act on.

The Federal Reserve prioritizes core trends because they indicate whether inflation is embedded across the economy.

For investors, the key is not just whether inflation is high—but whether it is broad-based, persistent, and accelerating.

When core inflation shows consistent improvement, financial conditions can ease—even if headline numbers fluctuate.

When core remains stubbornly elevated, restrictive policy may persist longer than markets initially expect.

Understanding the distinction between headline and core inflation allows investors to interpret CPI releases with clarity rather than emotion—and that clarity often determines who reacts wisely and who reacts too late.

PCE Index

The Personal Consumption Expenditures (PCE) index is the Federal Reserve’s most closely watched measure of inflation. While headlines often focus on CPI, policymakers at the Federal Reserve rely more heavily on PCE—especially Core PCE—when determining interest rate decisions.

For serious investors, understanding PCE is critical because it shapes rate expectations, bond yields, and ultimately equity valuations.

What Is the PCE Index?

The PCE index measures changes in prices paid by consumers for goods and services. It is published monthly as part of the Bureau of Economic Analysis report and provides a broader and more flexible inflation measure compared to CPI.

Unlike CPI, PCE:

- Adjusts for changes in consumer behavior (substitution effect).

- Has different weighting methods.

- Typically runs slightly lower than CPI over long periods.

Because of these methodological differences, PCE is often viewed as a smoother and more policy-relevant inflation indicator.

Core PCE Trend

Core PCE excludes food and energy, similar to Core CPI. However, it uses a dynamic weighting system that reflects how consumers actually shift spending when prices change.

For example:

- If beef prices rise sharply, consumers may switch to chicken.

- PCE accounts for this substitution, whereas CPI uses more fixed weights.

This makes Core PCE particularly valuable for policymakers because it reflects real-world spending adjustments.

When analyzing Core PCE, investors should focus on:

- Month-over-month changes

- Year-over-year changes

- Three- and six-month annualized trends

A consistent decline in Core PCE signals that underlying inflation pressure is easing sustainably—not just temporarily.

If Core PCE stalls or re-accelerates, it signals persistent pricing power across the economy.

Comparison with CPI

Although both CPI and PCE measure inflation, there are key differences:

1. Weighting Differences

CPI focuses more heavily on shelter costs.

PCE gives broader weight to healthcare and services.

2. Substitution Effect

PCE accounts for consumer behavior changes when prices shift.

CPI does not adjust as dynamically.

3. Level Differences

Historically, PCE tends to run about 0.2–0.4 percentage points lower than CPI.

Because of these differences, a CPI reading of 3% might correspond to a PCE reading closer to 2.6–2.8%.

Markets watch CPI closely for volatility, but the Fed ultimately bases long-term policy decisions more heavily on PCE trends.

The 2% Target

The Federal Reserve’s official inflation target is 2%, measured using PCE—not CPI.

This distinction is crucial.

When Core PCE is:

- Above 2% and rising → policy remains restrictive.

- Above 2% but declining steadily → markets begin pricing future easing.

- Near 2% and stable → the tightening cycle is likely complete.

The 2% target anchors expectations across financial markets. Bond yields, equity valuations, and currency movements all adjust based on how close PCE is to that threshold.

Why Sustained PCE Decline Supports Equity Rallies

Equity markets respond positively when Core PCE shows sustained moderation toward 2%.

Here’s why:

- Rate cut probabilities increase.

- Bond yields tend to fall.

- Discount rates decline.

- Valuation multiples expand.

When investors gain confidence that inflation is structurally under control, capital flows back into risk assets—particularly growth and cyclical sectors.

Historically, major equity rallies often began once inflation momentum clearly turned downward, even before the first official rate cut.

Markets anticipate policy relief well in advance.

When PCE Remains Elevated

If Core PCE stays elevated—especially above 3%—markets begin to fear prolonged tight policy.

In this scenario:

- Rate cut expectations get pushed further out.

- Treasury yields may rise.

- Growth stocks face valuation pressure.

- Defensive sectors may outperform.

Persistent inflation increases uncertainty about how long restrictive policy must remain in place.

Even if economic growth is stable, elevated PCE keeps financial conditions tight, limiting upside potential for equities.

The Strategic Insight

For investors, PCE is not just another inflation metric—it is the Federal Reserve’s compass.

Markets may react sharply to CPI headlines, but longer-term positioning depends on PCE trajectory.

If Core PCE shows consistent movement toward 2%, equity markets often begin re-rating higher in anticipation of easing conditions.

If PCE stagnates or reverses upward, the path to policy normalization becomes uncertain—raising volatility and compressing valuations.

Understanding the PCE trend allows investors to look beyond daily noise and focus on the structural inflation path that ultimately drives monetary policy and long-term market direction.

Shelter Inflation Trends

Shelter inflation is one of the most powerful drivers of overall inflation in the United States. Within the Consumer Price Index (CPI), shelter typically accounts for roughly one-third of the total basket—making it the single largest component.

Because of its weight, even small changes in shelter costs can significantly influence headline and core inflation readings. For investors tracking macro trends and Federal Reserve policy, understanding shelter dynamics is not optional—it is essential.

Why Shelter Matters So Much

Shelter inflation primarily includes:

- Rent of primary residence

- Owners’ equivalent rent (OER)

- Lodging away from home

Owners’ equivalent rent is especially important. It estimates what homeowners would pay to rent their own home. This makes shelter inflation heavily influenced by rental market trends—even if home prices themselves are slowing.

When shelter inflation rises:

- Core CPI remains elevated.

- The Federal Reserve maintains a restrictive policy.

- Rate cut expectations get delayed.

When shelter inflation declines:

- Core inflation cools more sustainably.

- Policy flexibility increases.

- Equity markets gain confidence.

Because shelter carries so much weight, it often determines whether inflation appears “sticky” or decisively falling.

Rent Growth Data

Real-time rental data from private sources often moves months before official CPI shelter data reflects the change.

Investors should monitor:

- National rent growth rates

- Month-over-month rent increases

- Vacancy rates

- New lease versus renewal lease pricing

When rent growth slows or turns negative in real-time market data, it suggests that shelter inflation will likely ease in upcoming CPI releases.

If rent growth accelerates again:

- Core CPI may remain elevated.

- Rate cut probabilities could decline.

- Bond yields may rise.

Rental market trends act as an early signal for future inflation momentum.

Housing Supply Trends

Housing supply is one of the most important structural forces behind shelter inflation. Because shelter carries the largest weight in CPI, changes in housing availability can significantly influence the overall inflation trajectory.

When supply shifts, inflation eventually shifts with it.

Key Indicators to Monitor

To understand whether housing supply is expanding or tightening, investors should track four primary indicators:

- New housing starts – Measures how many new homes begin construction. Rising starts suggest future supply growth.

- Building permits – A forward-looking signal showing planned construction activity.

- Multifamily construction activity – Critical for rental markets, as apartment supply directly affects rent pricing.

- Apartment completion rates – Shows how quickly new units are entering the market and competing for tenants.

These metrics provide early insight into whether supply pressure will ease or intensify in the months ahead.

If Supply Increases Meaningfully

When construction activity rises, and more units enter the market:

- Competition for tenants increases.

- Landlords lose pricing power.

- Rent growth slows.

- Shelter inflation gradually cools.

In this environment, disinflation becomes more sustainable. As rent pressure declines, core CPI often follows lower with a lag. Markets may begin pricing softer inflation even before official data confirms it.

If Housing Supply Remains Tight

When supply remains constrained due to high mortgage rates, zoning limitations, or reduced construction:

- Rental demand stays elevated.

- Landlords maintain pricing leverage.

- Rent growth persists.

- Shelter inflation remains sticky.

Persistent supply shortages can keep core inflation elevated even if other categories cool.

Why Timing Matters

Housing supply does not impact CPI immediately. Construction takes time, leases renew gradually, and pricing adjustments flow slowly into official inflation data.

However, once supply expansion becomes meaningful, pricing pressure shifts across markets. The cooling effect on inflation may take months—but it is structurally powerful.

Strategic Insight

Housing supply trends are not just a real estate issue—they are a macroeconomic signal.

Expanding supply supports disinflation and increases the probability of policy easing.

Tight supply prolongs inflation persistence and delays rate relief.

Investors who monitor housing supply indicators gain early visibility into future inflation trends—often months before CPI reflects the change.

Mortgage Rate Impact

Mortgage rates sit at the intersection of monetary policy, housing demand, and inflation. Because housing is the largest component of CPI, shifts in mortgage rates ripple through both home prices and rental markets—ultimately influencing shelter inflation.

When Mortgage Rates Rise

Higher mortgage rates tighten financial conditions and reduce affordability.

As rates increase:

- Monthly payments rise sharply.

- Home affordability declines.

- Fewer buyers qualify for loans.

- More households remain in the rental market.

This dynamic increases rental demand, which can keep rent growth firm—even if home sales slow. Strong rental demand supports elevated shelter inflation and can delay broader inflation moderation.

In addition, higher rates often discourage existing homeowners from selling, further limiting housing supply and reinforcing price pressure.

When Mortgage Rates Decline

Lower mortgage rates ease financial pressure and stimulate demand.

As rates fall:

- Monthly payments become more manageable.

- Homeownership becomes more accessible.

- Some renters transition into buyers.

- Rental demand moderates.

Reduced rental pressure can slow rent growth, which eventually cools shelter inflation. At the same time, lower rates often revive housing activity and support construction incentives.

The Construction Link

Mortgage rates also shape builder behavior.

- Rising rates discourage new construction due to weaker demand and higher financing costs.

- Falling rates encourage development as demand improves and financing becomes more attractive.

Because construction decisions take time to materialize into completed housing units, today’s mortgage rate environment influences future housing supply conditions.

The Bigger Macro Picture

Mortgage rates influence:

- Housing demand today

- Rental market pressure

- Future housing supply

- Long-term shelter inflation trends

In short, mortgage rates do not just affect homebuyers—they shape the inflation outlook.

When rates stay high, shelter inflation can remain sticky.

When rates fall sustainably, rent growth and housing pressure often ease over time.

Understanding mortgage rate dynamics provides investors with a forward-looking view of how housing will impact overall inflation and monetary policy.

The Lag Effect: Why Shelter Inflation Moves Slowly

One of the most important aspects of shelter inflation is its lag.

CPI shelter data does not immediately reflect real-time rental market changes. Instead:

- Rental surveys capture existing lease contracts.

- Many leases are renewed annually.

- Price adjustments filter into official data gradually.

As a result, even if market rents decline today, CPI shelter inflation may continue rising for several months before turning lower.

This lag creates an opportunity for forward-looking investors.

If real-time rent data shows clear deceleration, markets may anticipate softer CPI prints ahead—even before official numbers confirm it.

Understanding this timing difference allows investors to position ahead of consensus expectations.

Why Rolling Shelter Inflation Changes Market Expectations

If shelter inflation begins to roll over consistently:

- Core CPI declines more sustainably.

- Core PCE follows with a lag.

- The Federal Reserve gains confidence that inflation is moderating structurally.

- Rate cut probabilities increase.

Equity markets often react positively once investors believe shelter inflation has peaked—even if broader inflation remains slightly above target.

Because shelter is so heavily weighted, its direction often determines whether inflation appears persistent or decisively cooling.

Strategic Insight for Investors

Shelter inflation is not just a housing story—it is a monetary policy story.

When rent growth slows, and supply expands:

- Inflation risk declines.

- Bond yields typically soften.

- Growth stocks benefit from an improved valuation outlook.

When shelter remains sticky:

- Policy stays restrictive.

- Financial conditions tighten.

- Market rallies face resistance.

By tracking rent trends, supply data, and mortgage rate dynamics, investors gain early visibility into the inflation path that will ultimately shape Federal Reserve decisions and equity market direction.

In macro investing, understanding shelter inflation is understanding the core engine behind long-term inflation momentum.

Wage Growth

Wage growth is one of the most important bridges between labor market strength and long-term inflation risk. Strong employment alone does not create inflation—but when wages accelerate persistently, pricing pressure can spread across the economy.

For policymakers at the Federal Reserve, wage trends help determine whether inflation is cooling sustainably or becoming embedded.

Average Hourly Earnings Growth

Average hourly earnings (AHE) measure how quickly workers’ pay is increasing month over month and year over year.

If earnings growth accelerates sharply:

- Businesses face higher labor costs.

- Companies may pass those costs to consumers.

- Services inflation tends to remain sticky.

If wage growth slows gradually:

- Cost pressures ease.

- Inflation risks decline.

- Markets gain confidence in policy normalization.

Investors closely monitor the three- and six-month wage trends, not just one data point.

Real Wage Growth (After Inflation)

Real wages adjust earnings for inflation.

- If wages rise faster than inflation, consumers gain purchasing power.

- If inflation outpaces wages, household budgets tighten.

Positive real wage growth supports consumer spending and economic resilience.

However, if real wage gains are too strong during high inflation, they may sustain demand-driven price pressure.

Balance is key.

Wage-Price Spiral Risk

A wage-price spiral occurs when:

- Workers demand higher pay due to rising prices.

- Businesses raise prices to offset higher wages.

- Inflation expectations become entrenched.

This cycle can make inflation persistent and harder to control.

Historically, the Federal Reserve reacts aggressively if signs of a wage-price spiral emerge.

The Critical Balance

If wages rise faster than productivity, companies must either:

- Accept lower profit margins, or

- Increase prices.

This creates ongoing inflation pressure.

However, if wage growth moderates while employment remains stable:

- Inflation risk declines.

- Economic growth continues.

- The Fed gains flexibility to ease policy.

That balance—strong employment with cooling wage growth—is often described as the ideal “soft landing” scenario.

Strategic Insight

Wage data is not just about paychecks—it signals whether inflation will persist or fade.

Accelerating wages can delay rate cuts.

Moderating wages with stable employment can unlock policy flexibility.

Understanding this nuance allows investors to assess whether labor strength is supportive—or inflationary—and position accordingly.

2.3 Labor Market Strength

The labor market is the backbone of the U.S. economy.

The labor market is the engine of the U.S. economy. Consumer spending represents roughly two-thirds of GDP, and employment stability determines whether households feel confident enough to spend, borrow, and invest.

For markets, labor data influences two critical forces at the same time:

- Economic growth expectations

- Inflation and Federal Reserve policy expectations

Understanding this balance is essential.

Nonfarm Payrolls

The monthly Nonfarm Payrolls report measures how many jobs were added or lost in the economy.

Serious analysis should include:

- Monthly job creation numbers – Are jobs being added at a healthy pace?

- Comparison to expectations – Did the data surprise markets?

- Three-month moving average – Is hiring accelerating or slowing?

Markets respond not just to strength or weakness—but to deviations from forecasts.

Strong payrolls:

- Support economic growth outlook.

- Strengthen consumer spending expectations.

- But can raise inflation fears if wage pressure rises.

Weak payrolls:

- Signal a potential economic slowdown.

- May increase the probability of rate cuts.

- But can hurt corporate earnings expectations.

The ideal scenario for markets is balanced job growth—strong enough to avoid recession, but not so strong that it fuels inflation.

Unemployment Rate

The unemployment rate measures the percentage of the labor force actively seeking work but unable to find it.

Investors should examine:

- Current unemployment level

- Comparison to historical averages

- The Sahm Rule recession indicator (which flags recession risk when unemployment rises sharply from recent lows)

Very low unemployment suggests economic strength—but it can also create wage pressure if labor supply is tight.

Historically, sustained increases in unemployment often precede recessions. Markets closely watch for trend changes rather than single-month spikes.

Participation Rate

The labor force participation rate shows how many working-age individuals are either employed or actively seeking work.

This metric adds depth to unemployment analysis.

If unemployment rises because more people are entering the workforce, that is healthier than unemployment rising due to layoffs.

A stable or rising participation rate suggests:

- Structural resilience

- Improved labor supply

- Reduced wage pressure

Participation trends often determine whether rising unemployment signals expansion or contraction.

Average Hourly Earnings

Wage growth connects labor strength to inflation risk.

If wage growth accelerates:

- Consumer purchasing power increases.

- Demand remains strong.

- Inflation risk may rise if productivity does not keep pace.

If wage growth moderates while employment remains stable:

- Inflation pressure eases.

- The Federal Reserve gains policy flexibility.

- A “soft landing” becomes more achievable.

This dynamic often shapes market narratives following jobs reports.

Jobless Claims Trend

Weekly initial jobless claims provide one of the earliest warning signals of labor weakness.

- Rising claims trend → Early signs of layoffs and potential slowdown.

- Stable or declining claims → Continued labor resilience.

Markets frequently react to inflection points in claims data before larger economic indicators confirm change.

Because claims are released weekly, they offer faster insight than monthly payroll data.

Strategic Takeaway

Labor market data drives both growth expectations and monetary policy direction.

Strong labor supports earnings—but excessive strength may delay rate cuts.

Weak labor increases easing probability—but raises recession concerns.

The market’s preferred environment is equilibrium:

steady job growth, moderating wage pressure, stable participation, and controlled inflation risk.

Understanding these dynamics allows investors to interpret labor data not emotionally—but strategically.

2.4 GDP Growth and Economic Momentum

Gross Domestic Product (GDP) measures the total value of goods and services produced in the economy. But for investors, the level of GDP matters less than its momentum—whether growth is accelerating, stabilizing, or slowing.

Markets price future earnings. And earnings depend on the direction of economic momentum, not just the last reported number.

Latest Quarterly GDP

When analyzing the most recent GDP report, focus on structure—not just the headline growth rate.

Key elements to assess:

- Annualized growth rate – Is the economy expanding above trend, at trend, or below trend?

- Key contributors – How much came from:

- Consumer spending

- Business investment

- Government spending

- Inventory adjustments – Were companies building inventory (temporary boost) or drawing it down?

If GDP is strong because of inventory buildup, growth may slow next quarter.

If GDP is moderate but driven by stable consumer demand and investment, expansion may be more sustainable.

Strong GDP with weakening forward indicators can signal temporary strength.

Moderate GDP with improving forward signals often indicates durable expansion.

Structure matters more than the headline.

Leading Indicators

Leading indicators help investors anticipate turning points before GDP confirms them.

Key measures include:

- Conference Board Leading Economic Index (LEI) – Tracks forward-looking components such as new orders and credit conditions.

- Yield curve slope – Inversions often precede economic slowdowns.

- Manufacturing orders – Signal future production demand.

- Housing starts – Reflect confidence and construction momentum.

Leading indicators typically turn before GDP does.

Persistent declines in these indicators have historically preceded recessions by several months. Markets often react to these signals well before official GDP data reflects the slowdown.

ISM Manufacturing & Services

The ISM surveys measure business activity using a diffusion index:

- Above 50 → Expansion

- Below 50 → Contraction

Manufacturing and services can diverge.

Because services dominate the U.S. economy, the Services PMI carries greater weight in assessing overall growth.

If manufacturing contracts while services remain strong, it may indicate sector rotation rather than a broad recession.

However, if both fall below 50 and trend downward, economic momentum is likely deteriorating.

Consumer Spending Trends

Consumer activity drives the majority of U.S. GDP.

Key indicators include:

- Retail sales growth – Measures spending momentum.

- Credit card spending trends – Reflect near-term consumption patterns.

- Savings rate – Shows financial cushion strength.

- Delinquency levels – Indicate financial stress.

Strong consumer spending supports corporate revenues and earnings growth.

Weakening spending, rising delinquencies, and falling savings rates increase recession risk.

Because consumer behavior shifts before GDP data confirms a change, markets closely track spending trends for early signals.

Strategic Takeaway

GDP confirms where the economy has been.

Leading indicators, PMI data, and consumer trends suggest where it is heading.

Strong momentum supports earnings and equity valuations.

Slowing momentum increases volatility and shifts sector leadership.

Investors who focus on direction—not just data points—gain a forward-looking edge in assessing market risk and opportunity.

3. Corporate Earnings and Valuation Analysis

If economic data explains the environment, corporate earnings explain the reality. In the long run, stock prices follow earnings growth. Liquidity and sentiment can move markets temporarily—but sustained bull markets require rising profits.

This section connects earnings strength, valuation levels, and corporate financial health to determine whether the market’s current pricing is justified or stretched.

3.1 Earnings Season Trends

Earnings season is the most data-rich period for investors. Every quarter, companies reveal not only what they earned—but how they see the future.

To evaluate earnings season properly, investors must look beyond headlines.

Beat/Miss Ratios

The beat/miss ratio measures how many companies report earnings above analyst expectations versus those that fall short.

However, context matters:

- If 75% of companies beat estimates, that sounds strong.

- But if analysts lowered expectations aggressively before the quarter, the “beat” may not signal true strength.

Investors should analyze:

- How many companies beat by (magnitude of surprise)

- Whether revenue also beat expectations

- How stocks reacted after reporting

If companies beat earnings but stocks fall, it may indicate that expectations were already priced in.

Strong earnings seasons typically show:

- High beat rates

- Revenue growth

- Positive stock reactions

- Upward revisions

Forward Guidance Revisions

Forward guidance often matters more than past results.

Investors should ask:

- Are companies raising full-year revenue outlooks?

- Are they warning about demand slowdown?

- Are margins expected to improve or contract?

Markets are forward-looking. If companies lower guidance—even after beating current-quarter numbers—stocks may decline.

Upward guidance revisions often signal:

- Strong demand visibility

- Pricing power

- Confidence in macro stability

Widespread downward revisions may indicate emerging economic stress.

Revenue Growth vs Margin Compression

Earnings can grow for two reasons:

- Revenue expansion

- Margin expansion

Revenue growth reflects demand strength.

Margin expansion reflects efficiency and pricing power.

In inflationary environments:

- Companies may maintain revenue growth.

- But rising labor or input costs compress margins.

Margin compression across sectors often signals cost pressure building in the economy.

If revenue slows and margins shrink simultaneously, earnings risk increases.

Mega-Cap Earnings Impact

A handful of mega-cap companies now drive a significant portion of index performance, especially within the S&P 500 and Nasdaq.

Pay close attention to earnings from:

These companies influence:

- Index-level earnings growth

- AI investment trends

- Cloud demand

- Consumer spending patterns

If mega-cap earnings are strong while the broader market weakens, rallies may become narrow and concentrated.

Broad-based earnings strength across sectors is healthier and more sustainable than leadership concentrated in a few names.

3.2 Valuation Metrics Investors Are Watching

Valuations determine how much investors are willing to pay for earnings. Even strong profits can lead to weak stock performance if valuations are stretched.

Forward P/E Ratio

The forward price-to-earnings ratio compares current stock prices to expected earnings over the next 12 months.

- Rising forward P/E → investors expect strong growth or falling rates.

- Falling forward P/E → risk premium increasing.

Compare current P/E levels to:

- 5-year average

- 10-year average

- Prior cycle peaks

High valuations can be justified in low-rate environments with strong growth.

They become vulnerable when rates rise or earnings slow.

CAPE Ratio

The cyclically adjusted P/E (CAPE) smooths earnings over a 10-year period.

It helps answer: