Banking Sector Under Pressure: How Higher Rates and Regulation Are Reshaping US Financial Stability is one of the most critical financial themes in 2026 as rising interest rates, tighter regulations, and shifting economic conditions begin to redefine how banks operate, lend, and manage risk across the United States. Investors, policymakers, and consumers are all watching closely as the financial system adapts to a higher-rate environment that is testing resilience in ways not seen in over a decade.

Why the US Banking Sector Is Facing Renewed Pressure in 2026

The US banking sector entered 2026 with a fundamentally different landscape compared to the low-interest-rate era that defined the previous decade. After aggressive rate hikes aimed at controlling inflation, banks are now operating in a high-cost capital environment where borrowing is more expensive, and credit demand is evolving.

Recent financial data suggests that while large banks remain relatively stable, regional and mid-sized banks are experiencing increased pressure. Deposit flows have become more volatile as consumers and businesses seek higher yields in money market funds and other alternatives. This shift has forced banks to offer more competitive interest rates, squeezing their margins.

At the same time, loan growth is slowing. Higher borrowing costs are reducing demand for mortgages, business loans, and consumer credit. This combination of rising funding costs and slowing lending activity is creating a challenging environment for profitability across the sector.

The Impact of Higher Interest Rates on Bank Profitability and Risk

Higher interest rates typically benefit banks through increased net interest margins—the difference between what banks earn on loans and what they pay on deposits. However, in 2026, the situation is more complex.

While banks initially benefited from rate hikes, the prolonged period of elevated rates is now starting to create risks. Borrowers are feeling the pressure of higher repayment costs, leading to concerns about potential increases in loan defaults, particularly in sectors like commercial real estate and small business lending.

Additionally, the value of long-term assets such as bonds held by banks has been affected by rising yields. This has created unrealized losses on balance sheets, a factor that investors are closely monitoring. Although these losses may not immediately impact operations, they can influence market confidence and stock valuations.

Regulatory Changes Are Tightening the Financial System

In response to recent financial instability and ongoing economic uncertainty, regulators in the United States are taking a more cautious approach. New and proposed regulations are aimed at strengthening the resilience of the banking system, but they also introduce additional challenges for financial institutions.

Capital requirements are becoming stricter, particularly for mid-sized banks that were previously subject to lighter regulation. Stress testing is expanding, and compliance costs are rising as banks invest in systems to meet new regulatory standards.

These changes are designed to prevent systemic risks, but they also impact profitability. Banks must balance regulatory compliance with the need to maintain competitive returns for shareholders. This tension is shaping strategic decisions across the industry.

Regional Banks vs Big Banks: A Growing Divide

One of the most notable trends in 2026 is the widening gap between large national banks and smaller regional institutions. Large banks benefit from diversified revenue streams, global operations, and stronger capital buffers, making them more resilient in volatile conditions.

In contrast, regional banks often rely more heavily on specific sectors, such as commercial real estate or local business lending. This concentration can increase risk, especially when economic conditions shift.

Recent market movements indicate that investors are favoring large banks, viewing them as safer investments during periods of uncertainty. Meanwhile, regional banks are facing greater scrutiny, with stock prices reflecting concerns about liquidity, asset quality, and exposure to rate-sensitive sectors.

What This Means for Consumers, Businesses, and Investors

The changes in the banking sector are not just a concern for financial institutions—they have direct implications for consumers and businesses. Higher interest rates mean more expensive loans, affecting everything from home purchases to business expansion plans.

For consumers, this could translate into higher mortgage rates, increased credit card interest, and tighter lending standards. For businesses, especially small and medium-sized enterprises, access to credit may become more limited or costly.

Investors, on the other hand, need to reassess their strategies. Bank stocks, once seen as stable income-generating assets, are now subject to increased volatility. Understanding which institutions are best positioned to navigate this environment is becoming increasingly important.

Market Outlook: Stability or Stress Ahead for US Banks?

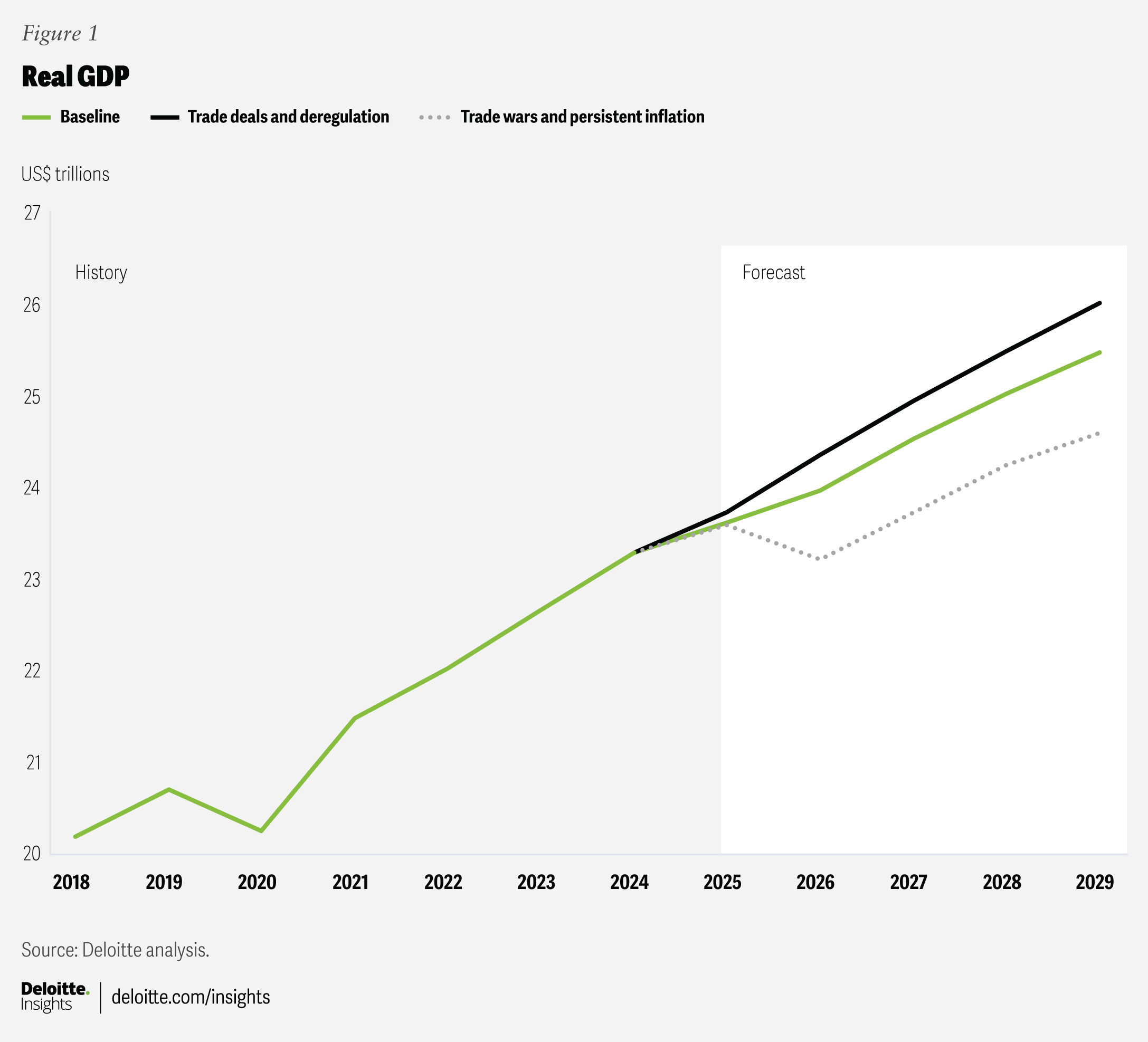

Looking ahead, the outlook for the US banking sector in 2026 will depend on several key factors. If inflation continues to moderate and interest rates stabilize, banks may find a more balanced operating environment.

However, if rates remain elevated for an extended period, pressure on borrowers and financial institutions could intensify. This scenario may lead to increased defaults, tighter credit conditions, and continued market volatility.

Experts suggest that the sector is likely to undergo structural changes, including consolidation among smaller banks and increased investment in technology to improve efficiency. Digital transformation and risk management will play critical roles in shaping the future of banking.

A Defining Moment for the US Banking System

The US banking sector is navigating one of its most challenging periods in recent history. Higher interest rates, evolving regulations, and shifting economic conditions are forcing banks to adapt quickly to maintain stability and profitability.

For readers, investors, and businesses, understanding these dynamics is essential. The decisions made today—by policymakers, financial institutions, and market participants—will shape the future of the financial system for years to come.

As uncertainty remains a key theme in 2026, staying informed and prepared is the best strategy in an ever-changing financial landscape.

Subscribe to trusted news sites like USnewsSphere.com for continuous updates.