Mortgage rates in the U.S. have fallen below 6 percent for the first time in nearly four years, offering potential relief for homebuyers and homeowners looking to refinance existing loans while significantly lowering borrowing costs. This drop — driven by movement in Treasury yields, changing economic expectations, and data showing slowing inflation — marks one of the most noteworthy shifts in the mortgage market since the rate surge of late 2023 and 2024. Lower costs are already pushing refinancing activity sharply higher and improving affordability, although housing supply constraints still temper overall market growth.

This shift matters now because it directly affects monthly mortgage payments, mortgage-eligibility thresholds, and decisions by millions of Americans contemplating home purchases or refinancing this spring and summer.

Why Mortgage Rates Dropped Below 6 Percent

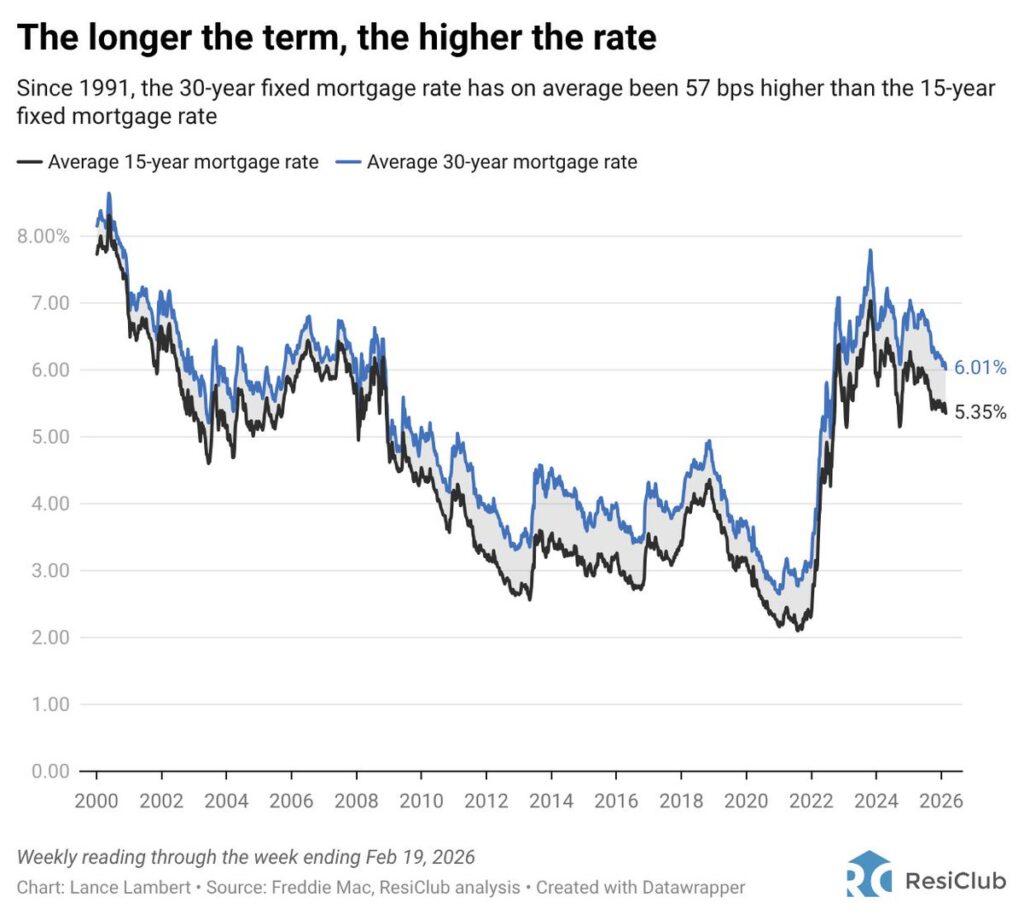

U.S. mortgage rates have cooled significantly over recent weeks, with the average 30-year fixed mortgage rate dipping around 5.99 percent to 6.01 percent, according to multiple weekly surveys and financial data services. This puts rates at their lowest level since late 2022, a notable turnaround from the historically high rates above 7 percent seen in early 2025.

Several key forces are driving rates lower:

- Treasury yields, especially the 10-year, have retreated as investors anticipate slower economic growth and easing inflation pressures. Mortgage rates tend to follow these long-term bond yields closely.

- Federal Reserve rate decisions remain influential. While the Fed has paused aggressive cuts, past rate reductions and expectations for future policy shifts still help nudge mortgage costs downward.

- Market psychology and investor demand for mortgage-backed securities have also supported downward pressure on borrowing rates.

This decline is not just a rounding error — it’s a meaningful shift that affects borrowing costs for home purchases, refinances, and overall affordability.

Who Benefits Most from the Rate Decline

Refinancing Homeowners:

Homeowners who secured mortgages when rates were significantly higher — especially between 7 percent and 8 percent — now have the potential to refinance into much cheaper debt. Refinancing at sub-6 percent rates could slash monthly payments by hundreds of dollars for many borrowers, depending on loan size, term length, and fees.

First-Time and Move-Up Buyers:

Lower rates improve home affordability in a measurable way. On a typical 30-year loan, even a full percentage point drop in interest can make home ownership more accessible for buyers near affordability limits. Combined with modest wage growth and cooling price gains in some markets, borrowing becomes a little less expensive than last year’s peak period.

Lenders and Refinancing Services:

Mortgage lenders now see a surge in refinancing inquiries and applications, as borrowers seek to take advantage of favorable pricing before potential future rate volatility disrupts this trend.

Why This Matters Now: Market Impact & Economic Context

Falling mortgage rates can improve purchasing power, reduce monthly payments, and encourage refinancing — all of which help stimulate housing market activity. Yet, despite more affordable financing, pending home sales have not jumped sharply, highlighting that loan costs are only one piece of broader housing conditions that include supply shortages and high home prices.

Economists caution that:

- Housing inventory remains low, which limits how much sales can rise even when rates fall.

- Inflation and labor market resilience still influence the Fed’s caution on further cuts, meaning that the recent rate drop may not deepen rapidly without additional economic data supporting inflation slowing further.

This timing matters because spring and summer traditionally see the most homebuying activity, and 2026’s early rate declines could set the stage for a more active season than the year before.

How Mortgage Rate Trends Are Forecasted

Most experts expect mortgage rates to stay in the mid-6 percent range for much of 2026, with the possibility of dipping slightly lower if economic indicators continue to ease inflationary pressures. Some forecasts project that by year-end, rates could settle near or slightly below 6 percent — but not precipitously lower — due to enduring inflation concerns and overall market uncertainty.

Even if rates fluctuate slightly, they remain attractive compared with recent peaks, and for many borrowers the current environment still represents a rare window to secure a favorable long-term loan.

What Homeowners and Buyers Should Consider Now

If you’re thinking about buying a home or refinancing an existing mortgage:

- Compare multiple lenders: Rates can vary significantly between lenders and loan products.

- Consider your long-term goals: Short-term savings must be balanced with long-term investment and homeownership plans.

- Look beyond rate headlines: Fees, closing costs, and loan terms all affect the real cost of borrowing.

Taking action now — while rates are at a relative low — may yield benefits, especially before any future market shifts.

Mortgage Market Remains Dynamic

Mortgage rates falling below 6 percent is a meaningful development in the U.S. housing and financial landscape. It presents real opportunities for savings on monthly payments and greater refinancing participation. However, housing supply constraints and broader economic influences, like inflation and Fed policy, mean this trend should be monitored carefully. Still, the improved affordability window is a compelling story for homebuyers and investors alike.

Subscribe to trusted news sites like USnewsSphere.com for continuous updates.