1. What the Federal Reserve Is and How It Works

Understanding the Federal Reserve System is the foundation for understanding interest rates, inflation, borrowing costs, stock market movements, and the overall U.S. economy. Before analyzing rate hikes, recessions, or market reactions, readers must clearly understand what the Federal Reserve is, how it is structured, and how it makes decisions.

This section builds that foundation in simple language, supported by real data and institutional facts.

1.1 What Is the Federal Reserve?

The Federal Reserve — often called “the Fed” — is the central bank of the United States. It manages the nation’s monetary system and influences how expensive or affordable borrowing money becomes across the entire economy.

The Fed was created in 1913 after a series of financial crises, especially the Panic of 1907, exposed weaknesses in the U.S. banking system. Congress passed the Federal Reserve Act to create a more stable financial structure.

At its core, the Fed has three primary responsibilities:

- Set short-term interest rates

- Maintain stable prices (control inflation)

- Promote maximum sustainable employment

It is important to clarify that the Federal Reserve is not the same as the U.S. Treasury.

The U.S. Department of the Treasury manages government spending, collects taxes, and issues government debt. The Federal Reserve manages monetary policy and regulates the banking system. One controls fiscal policy (government budgets), the other controls monetary policy (money and interest rates).

As of the most recent data:

- The Federal Funds Rate target range reflects current monetary tightening or easing.

- Inflation (measured by CPI and PCE) shows whether price stability is being maintained.

- The unemployment rate reflects labor market strength.

These three indicators together define the Fed’s operating environment.

1.2 The Structure of the Federal Reserve System

The Federal Reserve is not a single institution located in one building. It is a system composed of multiple parts designed to balance regional and national economic interests.

There are three core components:

Board of Governors (Washington, D.C.)

The Board consists of seven members appointed by the U.S. President and confirmed by the Senate. Each member serves a 14-year term, designed to reduce political pressure and ensure independence.

The Chair of the Federal Reserve plays a central leadership role and represents the institution publicly. The Chair oversees policy direction and leads press conferences following interest rate decisions.

12 Regional Federal Reserve Banks

The country is divided into 12 Federal Reserve districts, including major cities such as:

- New York

- Chicago

- Dallas

- San Francisco

- Atlanta

- Boston

Each regional bank gathers economic data from its district, supervises banks, and contributes regional insights into national policy discussions. The New York Fed has a particularly important role because it conducts open market operations that implement interest rate decisions.

Federal Open Market Committee (FOMC)

The Federal Open Market Committee is the body that sets interest rates. It includes:

- The 7 Board of Governors members

- The President of the New York Fed

- 4 rotating presidents from the remaining regional banks

The FOMC meets eight times per year to evaluate economic data and vote on rate changes.

Board of Governors

The Board of Governors is the central governing body of the Federal Reserve System and serves as the core decision-making authority behind U.S. monetary policy. Located in Washington, D.C., the Board provides national oversight of the entire Federal Reserve structure and plays a leading role in setting interest rates, supervising banks, and maintaining financial stability.

The Board consists of seven members, known as Governors. Each Governor is nominated by the President of the United States and confirmed by the U.S. Senate. Governors serve staggered 14-year terms, which are intentionally long to protect the Federal Reserve from short-term political pressure. This structure ensures continuity and independence in monetary policy decisions.

One of the seven Governors is appointed as Chair of the Federal Reserve for a renewable four-year term. The Chair is the most visible leader of the Federal Reserve and serves as the primary spokesperson during press conferences, congressional testimony, and financial crises. The Chair also leads meetings of the Federal Open Market Committee (FOMC), which sets interest rate policy.

Another Governor is designated as Vice Chair, also serving a renewable four-year term. The Vice Chair supports the Chair and often leads initiatives related to financial regulation and stability.

There is also a Vice Chair for Supervision, a role created after the 2008 financial crisis to strengthen oversight of large financial institutions. This position focuses specifically on bank regulation, stress testing, capital requirements, and systemic risk monitoring.

Key Responsibilities of the Board of Governors:

Monetary Policy Leadership

All seven Governors are permanent voting members of the FOMC. This means they vote on every interest rate decision and policy action. Their collective votes heavily influence the direction of the Federal Funds Rate and overall monetary policy.

Banking Supervision and Regulation

The Board oversees large bank holding companies, supervises financial institutions, and sets regulatory standards. It establishes capital requirements, liquidity rules, and stress testing frameworks to ensure the stability of the U.S. banking system.

Financial Stability Oversight

The Board monitors risks within financial markets, including credit markets, asset bubbles, and systemic vulnerabilities. During crises, it can authorize emergency lending programs to stabilize markets.

Payment System Oversight

The Board supervises key national payment systems to ensure smooth financial transactions across the country.

Research and Data Analysis

The Board relies on extensive economic research, data modeling, and forecasting to guide decisions. Staff economists analyze inflation trends, labor markets, GDP growth, credit conditions, and global economic developments.

Independence and Structure

The staggered 14-year terms are one of the most important design features of the Board. Because only one term expires every two years, no single president can immediately reshape the entire Board. This reduces political influence and supports long-term economic stability.

Although Governors serve 14-year terms, the Chair and Vice Chair serve renewable four-year leadership terms within their broader tenure as Governors.

Governors cannot be removed for policy disagreements. They can only be removed for cause, which further strengthens institutional independence.

Geographic and Economic Representation

By law, the composition of the Board must reflect a broad representation of the U.S. economy, including agriculture, commerce, industry, services, and labor interests. This ensures decisions are not overly influenced by one region or sector.

Compensation and Funding

The Federal Reserve is self-funded. It does not receive appropriations from Congress. Instead, it earns income from interest on government securities and other assets. This funding structure further supports operational independence.

Why the Board of Governors Matters for Markets

Because all Governors vote at every FOMC meeting, their views on inflation, employment, and financial stability can strongly influence interest rate decisions. Markets closely watch speeches, testimony, and policy statements from Board members for signals about future rate hikes or cuts.

Investors analyze:

- Tone of public speeches

- Voting patterns

- Dissents during rate decisions

- Forecast changes in economic projections

A shift in Board leadership or vacancies can influence policy direction, making this body critically important for understanding future interest rate trends.

12 Regional Federal Reserve Banks

The 12 Regional Federal Reserve Banks are the operational arms of the Federal Reserve System. While the Board of Governors provides national leadership from Washington, D.C., the regional banks connect monetary policy to local economies across the United States.

When the Federal Reserve was created in 1913, lawmakers wanted to prevent financial power from being concentrated in one city. The result was a decentralized structure: twelve regional banks spread across different economic centers of the country. This ensures that monetary policy reflects conditions in manufacturing hubs, agricultural regions, energy-producing states, financial centers, and technology corridors.

The 12 Federal Reserve Districts and Their Head Offices:

- Boston

- New York

- Philadelphia

- Cleveland

- Richmond

- Atlanta

- Chicago

- St. Louis

- Minneapolis

- Kansas City

- Dallas

- San Francisco

Federal Reserve Districts and Their Key Economic Sectors

| District | Federal Reserve Bank (Head City) | States / Major Coverage | Key Economic Sectors |

|---|---|---|---|

| 1 | Boston | New England (MA, CT, RI, VT, NH, ME) | Education, Healthcare, Biotechnology, Financial Services, Technology |

| 2 | New York | NY, Northern NJ, Puerto Rico, U.S. Virgin Islands | Global Finance, Investment Banking, Media, Real Estate, International Trade |

| 3 | Philadelphia | Eastern PA, Southern NJ, Delaware | Pharmaceuticals, Healthcare, Chemicals, Manufacturing, Financial Services |

| 4 | Cleveland | Ohio, Western PA, Eastern KY, Northern WV | Manufacturing, Automotive Parts, Steel, Healthcare |

| 5 | Richmond | VA, MD, NC, SC, DC, WV | Banking, Government Services, Agriculture, Manufacturing, Ports & Logistics |

| 6 | Atlanta | AL, FL, GA, Parts of TN, MS, LA | Tourism, Aerospace, Agriculture, Logistics, Consumer Services |

| 7 | Chicago | IL, IN, IA, WI, MI | Manufacturing, Agriculture, Automotive, Machinery, Financial Markets |

| 8 | St. Louis | MO, AR, Parts of IL, IN, KY, MS, TN | Agriculture, Food Processing, Transportation, Healthcare |

| 9 | Minneapolis | MN, MT, ND, SD, Parts of WI, MI | Agriculture, Energy, Mining, Banking, Manufacturing |

| 10 | Kansas City | CO, KS, NE, OK, WY, NM, Western MO | Energy (Oil & Gas), Agriculture, Aerospace, Transportation |

| 11 | Dallas | TX, Northern LA, Southern NM | Energy, Technology, International Trade (Mexico), Manufacturing |

| 12 | San Francisco | CA, OR, WA, AZ, NV, UT, ID, AK, HI | Technology, Venture Capital, Entertainment, Trade with Asia, Real Estate |

The economic diversity across the 12 Federal Reserve districts ensures that U.S. monetary policy reflects the realities of technology-driven West Coast growth, Midwest manufacturing strength, Southern energy production, and Northeast financial markets. This decentralized structure allows regional economic data to influence national interest rate decisions.

Each regional bank serves a specific geographic district that includes multiple states. These districts reflect historical trade patterns rather than state boundaries.

Role and Core Responsibilities of Regional Federal Reserve Banks

Economic Research and Regional Intelligence

Each regional bank gathers economic data from businesses, community leaders, banks, and labor markets within its district. This “ground-level” information is shared with the Federal Open Market Committee (FOMC) before interest rate decisions.

For example:

- Manufacturing output in Chicago

- Agricultural activity in Kansas City

- Technology sector trends in San Francisco

- Energy production in Dallas

Current Presidents of the 12 Regional Federal Reserve Banks

| District | Federal Reserve Bank | Current President |

|---|---|---|

| 1 | Federal Reserve Bank of Boston | Susan M. Collins |

| 2 | Federal Reserve Bank of New York | John C. Williams |

| 3 | Federal Reserve Bank of Philadelphia | Patrick T. Harker |

| 4 | Federal Reserve Bank of Cleveland | Loretta J. Mester |

| 5 | Federal Reserve Bank of Richmond | Thomas I. Barkin |

| 6 | Federal Reserve Bank of Atlanta | Raphael W. Bostic |

| 7 | Federal Reserve Bank of Chicago | Austan D. Goolsbee |

| 8 | Federal Reserve Bank of St. Louis | Alberto G. Musalem |

| 9 | Federal Reserve Bank of Minneapolis | Neel Kashkari |

| 10 | Federal Reserve Bank of Kansas City | Jeffrey R. Schmid |

| 11 | Federal Reserve Bank of Dallas | Lorie K. Logan |

| 12 | Federal Reserve Bank of San Francisco | Mary C. Daly |

The President of the New York Fed (John C. Williams) serves as a permanent voting member of the Federal Open Market Committee (FOMC), while the remaining regional presidents rotate voting responsibilities annually.

This real-time feedback ensures policy decisions are not based solely on national averages but also reflect regional economic conditions.

Bank Supervision and Regulation

Regional Fed banks supervise and regulate member banks within their districts. They examine financial institutions to ensure they meet capital, liquidity, and risk management standards.

They also conduct stress testing, coordination, and monitor financial stability risks within their jurisdictions.

Financial Services to Banks and the Government

Regional banks provide essential services such as:

- Processing checks and electronic payments

- Distributing and collecting U.S. currency

- Managing government accounts

- Operating components of the national payments infrastructure

They act as the “bank for banks,” helping ensure liquidity flows smoothly through the financial system.

Implementation of Monetary Policy

While the FOMC sets policy, regional banks help implement it.

The most important operational role belongs to the Federal Reserve Bank of New York. Through its trading desk, it conducts open market operations — buying and selling U.S. Treasury securities to maintain the target federal funds rate.

Because of this responsibility, the President of the New York Fed is a permanent voting member of the FOMC.

Leadership Structure of Regional Banks

Each regional bank has:

- A President

- A Board of Directors

The President of each regional bank participates in FOMC meetings. However, only five regional presidents vote at any given time:

- The New York Fed President (permanent voter)

- Four other regional presidents (rotate annually)

This rotation system ensures geographic balance in monetary policy decisions.

Funding Structure

Regional Federal Reserve Banks are not funded by taxpayer dollars. Like the broader Federal Reserve System, they generate income primarily from interest on government securities and other financial assets.

After covering operating expenses, surplus earnings are transferred to the U.S. Treasury.

Why Regional Banks Matter for Interest Rates and Markets

Financial markets pay close attention to speeches and economic commentary from regional Fed presidents. Their public statements often signal future policy direction.

For example:

- A “hawkish” regional president may signal support for rate hikes to fight inflation.

- A “dovish” president may signal support for rate cuts to stimulate growth.

These signals can move:

- Stock markets

- Bond yields

- Currency markets

- Commodity prices

The Beige Book

One important contribution of regional banks is the Beige Book — a report published eight times per year summarizing economic conditions in each district. This report provides qualitative insights on:

- Consumer spending

- Wage pressures

- Hiring conditions

- Supply chain issues

- Credit demand

The Beige Book is widely followed by economists, investors, and policymakers because it reflects real-time economic sentiment.

Economic Diversity Across Districts

Each district represents a different economic strength:

- New York: Finance and global banking

- Chicago: Manufacturing and agriculture

- Dallas: Energy production

- San Francisco: Technology and innovation

- Atlanta: Transportation and logistics

This diversity ensures monetary policy decisions reflect the complexity of the U.S. economy.

Federal Open Market Committee (FOMC)

The Federal Open Market Committee (FOMC) is the body within the Federal Reserve System that makes official decisions about U.S. monetary policy — including whether interest rates go up, go down, or stay the same. When people hear that “the Fed raised rates” or “the Fed cut rates,” that decision was made by the FOMC.

The FOMC is the most powerful monetary policy committee in the world because its decisions directly influence borrowing costs, inflation, employment levels, stock markets, bond yields, currency strength, and global capital flows.

What the FOMC Actually Does

The FOMC’s primary responsibility is to set the target range for the Federal Funds Rate — the benchmark short-term interest rate that influences nearly every other rate in the U.S. economy.

However, its responsibilities go beyond just rate decisions. The FOMC:

- Sets the Federal Funds Rate target range

- Oversees open market operations (buying and selling U.S. Treasury securities)

- Directs quantitative easing (QE) or quantitative tightening (QT) programs

- Evaluates inflation, employment, and financial stability

- Provides forward guidance to financial markets

- Publishes economic projections and policy outlooks

In short, the FOMC controls the direction of U.S. monetary conditions.

Composition of the FOMC

The FOMC consists of 12 voting members:

- The 7 members of the Board of Governors

- The President of the Federal Reserve Bank of New York (permanent voter)

- 4 of the remaining 11 Regional Federal Reserve Bank presidents (rotating annually)

Although only 12 members vote, all 19 participants (7 Governors + 12 Regional Presidents) attend meetings and contribute to discussions.

This structure balances national oversight with regional economic input.

How the FOMC Makes Decisions

The FOMC meets eight times per year on a scheduled calendar. Emergency meetings can also occur during financial crises.

Before each meeting:

- Regional banks gather economic data from businesses, banks, labor markets, and industries in their districts.

- Staff economists prepare detailed reports analyzing inflation, GDP, employment, financial markets, and global conditions.

- The Beige Book is distributed, summarizing regional economic conditions.

During the meeting:

- Members review data.

- Economic forecasts are presented.

- Risks are debated (inflation risk vs recession risk).

- Members vote on policy actions.

Decisions are made by majority vote.

If there is disagreement, dissenting votes are recorded publicly. Financial markets pay close attention to dissents because they signal internal policy divisions.

Key Tools Directed by the FOMC

Federal Funds Rate Target

The FOMC sets a target range (for example, 5.25%–5.50%). The New York Fed then conducts operations to keep the actual rate within that range.

Open Market Operations

The FOMC authorizes the buying and selling of U.S. Treasury securities to manage liquidity in the banking system.

Quantitative Easing (QE)

During economic downturns, the FOMC may authorize large-scale asset purchases to inject liquidity into financial markets.

Quantitative Tightening (QT)

To reduce inflation or normalize policy, the FOMC may allow its balance sheet to shrink by not reinvesting maturing securities.

Forward Guidance

The FOMC provides signals about future policy direction through official statements and press conferences. Phrases such as “data dependent” or “higher for longer” can move markets significantly.

Economic Projections and Transparency

Four times per year, the FOMC releases the Summary of Economic Projections (SEP). This includes:

- Inflation forecasts

- GDP growth projections

- Unemployment expectations

- Federal Funds Rate projections (Dot Plot)

The “Dot Plot” shows each voting member’s expectations for future interest rates. Markets analyze the median projection to anticipate future rate moves.

After each meeting, the FOMC releases:

- A policy statement

- A vote breakdown

- An explanation of economic conditions

- A press conference by the Fed Chair

Meeting minutes are published three weeks later, providing deeper insight into policy debates.

Why the FOMC Matters for Financial Markets

Every FOMC decision can impact:

Stock Market

Higher rates often pressure growth stocks due to higher discount rates. Lower rates tend to support equities.

Bond Market

Bond prices move inversely to interest rate expectations. A rate hike typically pushes yields higher and bond prices lower.

Mortgage Rates

Changes in rate expectations influence 10-year Treasury yields, which affect mortgage rates.

U.S. Dollar

Higher rates often strengthen the dollar because global investors seek higher returns.

Commodities and Gold

Gold prices often move inversely with real interest rates.

Historical Importance of the FOMC

Over the decades, the FOMC has:

- Raised rates aggressively to fight 1980s inflation

- Cut rates to near zero during the 2008 financial crisis

- Launched quantitative easing programs

- Cut rates to zero during the 2020 pandemic

- Rapidly rising rates during the 2022–2024 inflation surge

These actions reshaped global markets and economic cycles.

Voting Rotation System

The President of the New York Fed votes permanently because that bank implements open market operations.

The other regional presidents rotate voting annually in groups, ensuring geographic diversity.

Even when not voting, non-voting presidents still participate in discussions and influence policy direction.

How Investors Monitor the FOMC

Professional investors track:

- Changes in policy statement language

- Economic forecast revisions

- Dot Plot shifts

- Dissents

- Tone during press conferences

- Balance sheet policy adjustments

Even a small wording change in the FOMC statement can trigger major stock and bond market reactions.

Current FOMC Voting Members (2026 Update)

Each year, the Federal Open Market Committee updates which regional Federal Reserve Bank presidents will have voting rights in addition to the Board of Governors and the permanent New York Fed vote. Voting membership for 2026 was determined at the first regularly scheduled FOMC meeting of the year.

For 2026, the FOMC voting members include:

The Federal Open Market Committee (FOMC) consists of 12 voting members. These members are responsible for setting the Federal Funds Rate and directing U.S. monetary policy. The voting structure combines national leadership with regional representation.

Chair: Jerome H. Powell

Vice Chair: Philip N. Jefferson

Vice Chair for Supervision: Michael S. Barr

Board Governors:

• Michelle W. Bowman

• Lisa D. Cook

• Adriana D. Kugler

• Christopher J. Waller

President of the Federal Reserve Bank of New York (Permanent Voting Member):

• John C. Williams

Rotating Regional Federal Reserve Bank Presidents Voting in 2026:

- Federal Reserve Bank of Cleveland – Loretta J. Mester

- Federal Reserve Bank of Dallas – Lorie K. Logan

- Federal Reserve Bank of Minneapolis – Neel Kashkari

- Federal Reserve Bank of Philadelphia – Patrick T. Harker

All other Regional Federal Reserve Bank presidents attend FOMC meetings and participate in policy discussions, but do not vote in 2026. The voting rotation changes annually at the first scheduled FOMC meeting of the year.

Key Information for Readers

- Current FOMC voting members and leadership roles

- Upcoming FOMC meeting calendar (eight scheduled meetings per year)

- Annual regional voting rotation schedule

Permanent FOMC Voters

These members vote every year because of their roles:

- All seven Board of Governors members

- President of the Federal Reserve Bank of New York (permanent regional voter)

Rotating Regional Fed Presidents (2026)

Four additional regional bank presidents rotate in each year. For 2026, the voting regional presidents are:

- President, Federal Reserve Bank of Cleveland

- President, Federal Reserve Bank of Dallas

- President, Federal Reserve Bank of Minneapolis

- President, Federal Reserve Bank of Philadelphia

Non-voting Participants

All other Regional Fed presidents participate in policy discussions and economic analysis at FOMC meetings, but do not cast a vote in 2026.

How the Rotation Works

- The president of the Federal Reserve Bank of New York is always a voting member.

- Of the remaining 11 regional Fed presidents, four receive voting rights each year, rotating on a scheduled cycle to ensure geographic representation.

- This rotation changes annually at the first regularly scheduled FOMC meeting (usually January).

2026 Rotating In (Voting This Year)

- Cleveland Fed President

- Dallas Fed President

- Minneapolis Fed President

- Philadelphia Fed President

2026 Rotating Out (Non-voting This Year)

Presidents not voting in 2026 include those from:

Kansas City

Boston

Chicago

St. Louis

1.3 The Fed’s Dual Mandate

The foundation of U.S. monetary policy rests on what is called the “dual mandate.” This mandate was given to the Federal Reserve System by Congress and defines the two core objectives that guide every interest rate decision, policy adjustment, and economic forecast.

In simple terms, the Federal Reserve has two main goals:

- Maximum Employment

- Stable Prices

Every FOMC meeting, every rate hike or rate cut, and every economic projection is evaluated through the lens of these two objectives.

Maximum Employment: What It Really Means

Maximum employment does not mean zero unemployment. In a dynamic economy, some level of unemployment is normal and even healthy. People change jobs, relocate, graduate from school, or temporarily leave the workforce. Economists refer to this as “frictional unemployment.”

The Fed aims for what is often called the “natural rate of unemployment” — the lowest level of unemployment the economy can sustain without causing excessive inflation.

If unemployment is too high:

- Consumer spending slows

- Business revenues fall

- Economic growth weakens

If unemployment is too low:

- Labor shortages emerge

- Wages rise rapidly

- Inflation pressures increase

The Fed’s challenge is to keep the labor market strong without allowing it to overheat.

Key Labor Market Indicators You Should Include

Unemployment Rate

This measures the percentage of people actively seeking work but unable to find jobs. It is one of the most closely watched economic indicators.

Nonfarm Payroll Growth

Released monthly, this measures how many jobs were added or lost in the economy, excluding farm workers.

Labor Force Participation Rate

This shows the percentage of working-age individuals either employed or actively looking for work. A declining participation rate can signal structural labor issues.

Job Openings (JOLTS Data)

The Job Openings and Labor Turnover Survey shows how many positions employers are trying to fill. High job openings often indicate strong labor demand.

Average Hourly Earnings

Wage growth is critical. Rapid wage increases can boost consumer spending but may also create inflationary pressure.

By analyzing these data points together, the Fed determines whether the labor market is balanced, overheating, or weakening.

Stable Prices: Controlling Inflation Without Stopping Growth

The second part of the dual mandate is price stability — keeping inflation under control.

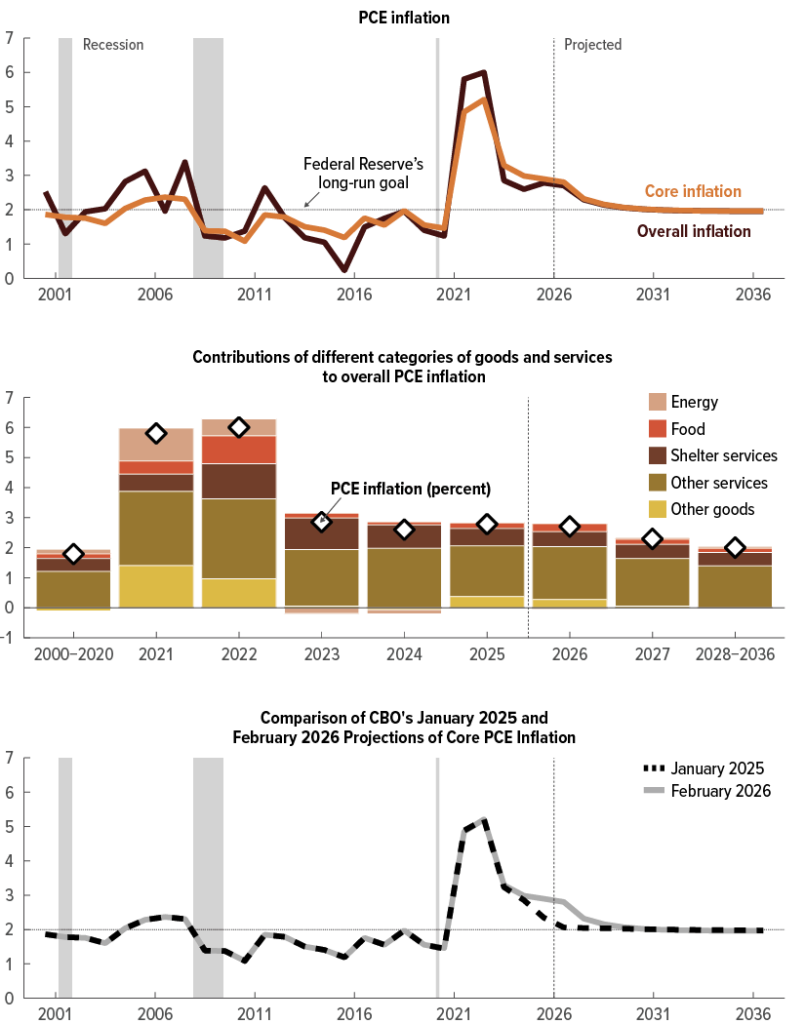

The Federal Reserve has defined its long-term inflation target as 2 percent. This target is measured primarily using the Personal Consumption Expenditures (PCE) price index.

Why 2 percent and not 0 percent?

Zero inflation may sound ideal, but mild inflation supports economic growth. A small, predictable level of inflation:

- Encourages consumer spending

- Supports wage growth

- Prevents deflation (a sustained decline in prices)

Deflation can be dangerous because it encourages people to delay purchases, which slows economic activity and investment.

If inflation rises well above 2 percent:

- Purchasing power declines

- Consumer confidence falls

- Interest rates often rise

If inflation falls too low:

- Economic growth can stall

- Businesses reduce investment

- Wages stagnate

Important Inflation Indicators You Should Include

Consumer Price Index (CPI)

Measures price changes for a basket of goods and services. Often used in media reports.

Core CPI

Excludes food and energy prices, which can be volatile.

PCE Inflation

The Fed’s preferred inflation measure. It adjusts for changes in consumer behavior and provides a broader view of spending patterns.

Core PCE

Excludes food and energy, offering a clearer view of underlying inflation trends.

Markets pay close attention to whether inflation readings are above or below the 2 percent target, as this heavily influences interest rate decisions.

How the Dual Mandate Shapes Interest Rate Decisions

When inflation rises above target and unemployment is low, the Fed may raise interest rates to cool demand and prevent overheating.

When unemployment rises, and inflation is stable or falling, the Fed may lower interest rates to stimulate economic growth.

This balancing act is often described as achieving a “soft landing” — slowing inflation without causing a recession.

However, policy trade-offs exist. Tightening policy too aggressively can push the economy into recession. Acting too slowly can allow inflation to become entrenched.

Dual Mandate Snapshot (Latest U.S. Data)

Inflation (PCE)

- Current Level: 2.8%

- Fed Target: 2.0%

- 10-Year Average: ~2.2%

- Status: Above Target

Core PCE Inflation

- Current Level: 2.8%

- Fed Target: 2.0%

- 10-Year Average: ~2.2%

- Status: Above Target

Unemployment Rate

- Current Level: 4.3%

- Fed Estimated Natural Rate: ~4.0%–4.5%

- 10-Year Average: ~5.0%

- Status: Near Balanced

Wage Growth (Average Hourly Earnings)

Status: Moderate Growth

Current Level: ~$31.95/hour

Stable Growth Range: Aligned with ~2% inflation

10-Year Average: ~$31/hour

This table immediately shows readers whether the economy is running “hot,” “cool,” or near equilibrium.

Why the Dual Mandate Matters for Small Businesses, Consumers, and Investors

For Small Businesses

Higher interest rates increase borrowing costs and can slow demand. Lower rates reduce financing costs but may increase wage pressures.

For Consumers

Interest rate changes affect mortgages, credit cards, car loans, and savings returns.

For Investors

Stock valuations, bond yields, and currency markets respond directly to expectations about inflation and employment trends.

Final Perspective

The dual mandate is the compass guiding all Federal Reserve policy decisions. Understanding maximum employment and stable prices gives readers the framework to interpret future rate hikes, cuts, and economic projections.

Every policy decision ultimately answers one question:

Is the economy too hot, too cold, or balanced?

The Federal Reserve’s job is to adjust monetary conditions until those two goals — strong employment and stable prices — move back into alignment.

1.4 How Monetary Policy Actually Works

Monetary policy may sound complex, but at its core, it relies on a few key tools that the Federal Reserve System uses to influence borrowing costs, liquidity, and economic activity in the United States. Each tool affects the economy through different channels — from the cost of loans to banks’ willingness to lend, to the amount of money circulating in financial markets.

Federal Funds Rate

The Federal Funds Rate is the central interest rate that banks charge each other for overnight loans of reserve balances. It is the most visible monetary policy tool because it sets the baseline cost for short-term borrowing in the economy. The Federal Open Market Committee (FOMC) sets a target range for this rate at every scheduled meeting.

As of the January 2026 FOMC meeting, the target range for the federal funds rate is 3.50% to 3.75% — unchanged from the previous meeting after a series of rate changes in the last few years aimed at balancing inflation and growth.

When the Fed raises the Federal Funds Rate:

- Mortgage rates tend to rise

- Credit card interest rates go up

- Business borrowing costs increase

- Overall borrowing slows

This typically cools consumer spending and business investment.

When the Fed lowers the Federal Funds Rate:

- Borrowing becomes cheaper

- Businesses may expand

- Consumers are more likely to finance purchases

- Economic activity is stimulated

This is why central banks often cut rates during slowdowns and raise them when inflation pressures rise.

Open Market Operations

Open Market Operations (OMOs) are the Fed’s most frequently used tool for implementing its monetary policy target. The Federal Reserve buys or sells U.S. Treasury securities in financial markets to influence the supply of money and the level of interest rates.

- Buying securities injects money into the banking system, increasing liquidity and generally lowering interest rates.

- Selling securities removes money from the system, tightening liquidity and placing upward pressure on interest rates.

The New York Fed conducts these operations on behalf of the FOMC to ensure the effective federal funds rate stays within its target range.

Discount Rate

The discount rate is the interest rate charged by the Federal Reserve when commercial banks borrow directly from the Fed’s discount window. This tool is primarily used as a safety valve for bank liquidity. The discount rate is typically set above the federal funds rate to encourage banks to seek funding from other banks first and to use the discount window only when necessary.

Reserve Requirements

Banks are historically required to hold a certain percentage of their deposits on reserve — either as cash in vaults or as deposits with the Federal Reserve. These reserve requirements affect how much money banks can lend. While this tool is rarely changed in day-to-day policy today, it remains part of the Fed’s toolkit for adjusting overall credit in the system.

Quantitative Easing (QE) and Quantitative Tightening (QT)

When interest rates were already near zero in past crises, the Federal Reserve turned to Quantitative Easing (QE) — large-scale purchases of Treasury securities and mortgage-backed securities — to inject liquidity and support financial markets and borrowing conditions. Over time, these QE programs expanded the Fed’s balance sheet dramatically. For example, the balance sheet grew from under $1 trillion before 2008 to around $4 trillion after QE programs in the early 2010s.

During the COVID-19 pandemic, the Fed again expanded its balance sheet significantly, leading to a peak total assets figure nearing $9 trillion in 2022 before policy normalization began.

In contrast, Quantitative Tightening (QT) is the process by which the Fed reduces its balance sheet by allowing securities to mature without reinvesting the proceeds. Starting from its historic peaks following the pandemic, the Fed has allowed much of this portfolio to shrink, bringing total assets down to around $6.6 trillion by late 2025 as part of policy normalisation.

These large asset purchases (QE) and runoff programs (QT) change the amount of reserves in the banking system and thereby affect market interest rates, credit conditions, and long-term borrowing costs beyond the federal funds rate alone.

Putting It All Together: A Flow Diagram

Here’s the basic transmission mechanism for monetary policy:

Fed decision → Change in cost of bank funding → Change in interest rates for businesses & consumers → Spending & investment reaction → Impact on inflation & employment

For example:

- When the Fed tightens policy (“hawkish”), credit becomes more expensive, slowing demand and putting downward pressure on inflation, but possibly slowing job growth.

- When the Fed loosens policy (“dovish”), borrowing becomes cheaper, stimulating spending and investment, potentially boosting jobs — but too much can push inflation above target.

This framework shows how the Fed’s policy tools — from the federal funds rate to QE/QT — operate through financial markets and the real economy to steer growth, inflation, and labor markets in line with its dual mandate.

1.5 Key Economic Indicators the Fed Watches

The Federal Reserve is fundamentally data-driven. Every interest rate decision, policy pivot, or forward-guidance statement depends on measurable economic indicators that signal the health of the U.S. economy. Policymakers do not guess — they evaluate hard data on inflation, jobs, growth, and financial stability before acting.

Below are the most important indicators the Fed watches closely, along with recent figures to give your readers context.

Inflation Indicators

Inflation measures changes in the prices consumers and businesses pay for goods and services. The Fed’s policy decisions are heavily influenced by whether inflation is above, near, or below the long-term target of 2 percent.

Consumer Price Index (CPI)

- CPI tracks a broad basket of goods and services out-of-pocket by consumers.

- Latest reading (Dec 2025): 3.4% year-over-year (U.S. Bureau of Labor Statistics) — above the Fed’s 2% target.

Core CPI (excludes food and energy)

- Often used to strip out volatile items.

- Latest reading (Dec 2025): 3.7% y/y — shows underlying inflation pressures.

Personal Consumption Expenditures (PCE) Price Index

- The Fed’s preferred inflation measure is the one that reflects consumer spending patterns in greater detail.

- Latest PCE inflation (Nov 2025): 2.8% y/y (Bureau of Economic Analysis).

Core PCE (excludes food and energy)

- This sub-measure is watched most closely at the Fed — it lines up closely with policy goals.

- Latest Core PCE (Nov 2025): 2.8% y/y.

Together, these inflation gauges show that price pressures remain above the Fed’s 2% goal, which informs decisions to slow the pace of rate cuts or maintain higher policy rates longer.

Employment Indicators

Strong employment is a central part of the Fed’s dual mandate. The Fed tracks multiple labor market metrics to separate healthy job growth from overheating or weakening conditions.

Nonfarm Payrolls

- Measures monthly job gains and losses across most sectors (excludes farm workers).

- Latest data (Jan 2026): +182,000 jobs added — moderate job growth.

Unemployment Rate

- Percentage of people actively seeking but unable to find work.

- Jan 2026: 4.3% (Bureau of Labor Statistics) — historically low, near full employment.

Wage Growth (Average Hourly Earnings)

- Wage growth signals labor market tightness.

- Latest: 4.1% y/y — moderate wage increases, but not at historic highs.

Labor Force Participation Rate

- The percentage of working-age people either working or looking for work.

- Latest: 62.6% — still below pre-COVID levels, suggesting some slack in the labor market.

These indicators help the Fed evaluate whether the labor market is too tight (which can fuel inflation) or too weak (which can drag on growth).

Growth Indicators

Growth metrics help the Fed determine whether the economy is expanding, slowing, or at risk of recession.

Gross Domestic Product (GDP)

- The broadest measure of economic activity.

- Latest real GDP growth estimate (Q4 2025): ~2.1% annualized — moderate growth.

Retail Sales

- Tracks consumer spending, which accounts for about two-thirds of GDP.

- Latest monthly retail sales growth: 0.3% — steady consumer demand.

Industrial Production

- Measures output in manufacturing, mining, and utilities.

- Latest: 0.1% increase month-over-month — stable industrial activity.

Together, these indicators help the Fed assess whether economic growth is broad-based or uneven.

Financial Stability Indicators

Monetary policy also considers risks within financial markets that could disrupt credit, lending, or liquidity.

Yield Curve (2-Year vs 10-Year Treasury Spread)

- The yield curve shows the relationship between short-term and long-term interest rates.

- When the 2-year rate exceeds the 10-year rate (an inversion), it has historically signaled recession risk.

- As of early 2026, the yield curve remains slightly inverted, which signals cautious market sentiment.

Credit Spreads

- The difference between corporate bond yields and Treasury yields.

- Widening spreads signal greater risk aversion in markets.

Bank Lending Standards

- Collected through the Fed’s Senior Loan Officer Opinion Survey (SLOOS).

- Tighter standards indicate banks are less willing to lend — a sign of financial contraction.

These indicators are not part of the dual mandate but are critical for detecting emerging stress in the financial system.

Why These Indicators Matter

When inflation remains above the Fed’s target, and the labor market is strong, policymakers may delay cutting rates or hold rates steady to prevent the economy from overheating.

If inflation eases while job growth slows, the Fed may be more comfortable reducing rates to support growth.

Financial stability measures (like the yield curve) add another layer — signaling when markets may be pricing in a recession, which can prompt pre-emptive policy action.

2. How Interest Rates Are Set and Why They Change

2.1 What Is the Federal Funds Rate?

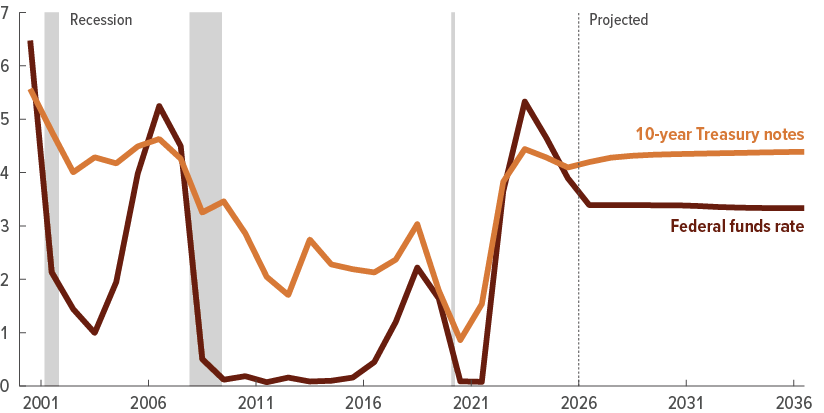

The Federal Funds Rate is the most influential short-term interest rate in the U.S. financial system. It is the interest rate at which depository institutions (banks, credit unions, savings institutions) lend reserve balances to each other overnight. This rate influences borrowing costs across the economy — including mortgages, auto loans, credit card rates, and business lending — making it one of the Fed’s primary policy tools.

The Federal Funds Rate is the rate at which banks lend reserve balances (their cash held at Federal Reserve banks) to other banks with short-term funding needs. Because banks must maintain certain reserve levels, when they are short on reserves, they borrow from other institutions that have excess.

The Federal Open Market Committee (FOMC) does not set the actual rate directly. Instead, it establishes a target range for the rate and uses market operations to guide the effective rate toward that target.

Target Range Explanation

Instead of announcing a single fixed rate, the Fed announces a target range for the Federal Funds Rate. For example:

- At the January 2026 FOMC meeting, the target range was set at 3.50%–3.75%.

- This range reflects the Federal Reserve’s current stance on monetary policy — balancing inflation control and economic growth.

The Federal Reserve uses tools like open market operations to ensure that the effective federal funds rate stays within the target range. If the actual rate moves too far outside the range, the Fed intervenes to bring it back in line.

Effective Rate vs. Target Rate

- Target Range: This is the goal set by the FOMC. It represents the range within which the Fed wants the overnight rate to trade. It is forward-looking and reflects monetary policy intent.

- Effective Federal Funds Rate: This is the actual rate at which banks transact with each other in the market. It may be slightly above or below the target range on a given day, but generally stays very close.

For example:

- FOMC Target Range (Jan 2026): 3.50% – 3.75%

- Effective Federal Funds Rate (latest): ~3.60% (Federal Reserve Economic Data – FRED)

The closeness of the effective rate to the target range signals that the Fed’s policy tools are working as intended.

Why This Matters for the Economy

Because many other interest rates are priced off the Federal Funds Rate:

- Mortgage rates tend to move higher when the Fed tightens policy

- Auto loans and personal credit become more expensive

- Business borrowing costs rise, potentially slowing investment

- Savings yields can increase, benefiting savers

Conversely, when the Fed cuts the target range:

- Borrowing becomes cheaper

- Economic activity often accelerates

- Consumers may take on more loans

- Businesses may expand operations or hire more workers

Real-World Context & Recent Data

After a period of aggressive rate increases between 2022 and 2023 to curb high inflation, the Fed maintained elevated rates in 2024 and early 2025 as inflation pressures remained above target. By the start of 2026, with inflation showing signs of easing but still above the Fed’s 2% goal, the Federal Funds Rate target range settled at 3.50%–3.75%.

This higher rate environment reflects the Fed’s ongoing effort to balance price stability with labor market strength.

Quick Comparison: Past Rate Cycles

| Period | Target Rate | Economic Context |

|---|---|---|

| 2008 (Financial Crisis) | Near 0% | Emergency easing |

| 2018 | 2.25% – 2.50% | Pre-pandemic tightening |

| 2020 (Pandemic) | 0% – 0.25% | Crisis response |

| 2023–2025 | 4.25% – 5.25% | Inflation fight |

| 2026 | 3.50% – 3.75% | Easing stabilization |

(Actual rates and ranges sourced from Federal Reserve historical releases and FRED.)

The Federal Funds Rate is the bedrock of U.S. monetary policy — and understanding it is essential to interpreting interest rates, financial markets, and economic cycles. It tells readers not only what the Fed is targeting but why those targets matter for everyday financial decisions.

2.2 How the FOMC Decides on Rate Hikes or Cuts

The Federal Open Market Committee (FOMC) does not adjust interest rates at random. Every change — whether a hike, a cut, or holding steady — is the outcome of a deliberate, scheduled process that incorporates economic data, projections, and forward guidance. Understanding this process gives readers a clear view of why the Federal Reserve acts when it does.

Meeting Schedule — 8 Times per Year

The FOMC meets regularly to review economic conditions and decide whether to adjust monetary policy. These meetings occur eight times per year on a pre-announced schedule, typically every six to eight weeks.

For 2026, the FOMC meeting calendar is:

| Meeting | Dates (Tentative / Official) |

|---|---|

| 1 | January 27–28, 2026 |

| 2 | March 17–18, 2026 |

| 3 | April 28–29, 2026 |

| 4 | June 9–10, 2026 |

| 5 | July 28–29, 2026 |

| 6 | September 22–23, 2026 |

| 7 | November 3–4, 2026 |

| 8 | December 15–16, 2026 |

(Source: Federal Reserve official FOMC calendar)

At each meeting, policymakers assess inflation data, labor market metrics, financial conditions, global developments, and various economic forecasts. After discussion and debate, the committee votes on the policy statement and the target range for the Federal Funds Rate.

Most meetings conclude with a policy statement — explaining any changes and the reasoning behind them — and, four times per year, the Fed releases detailed economic forecasts.

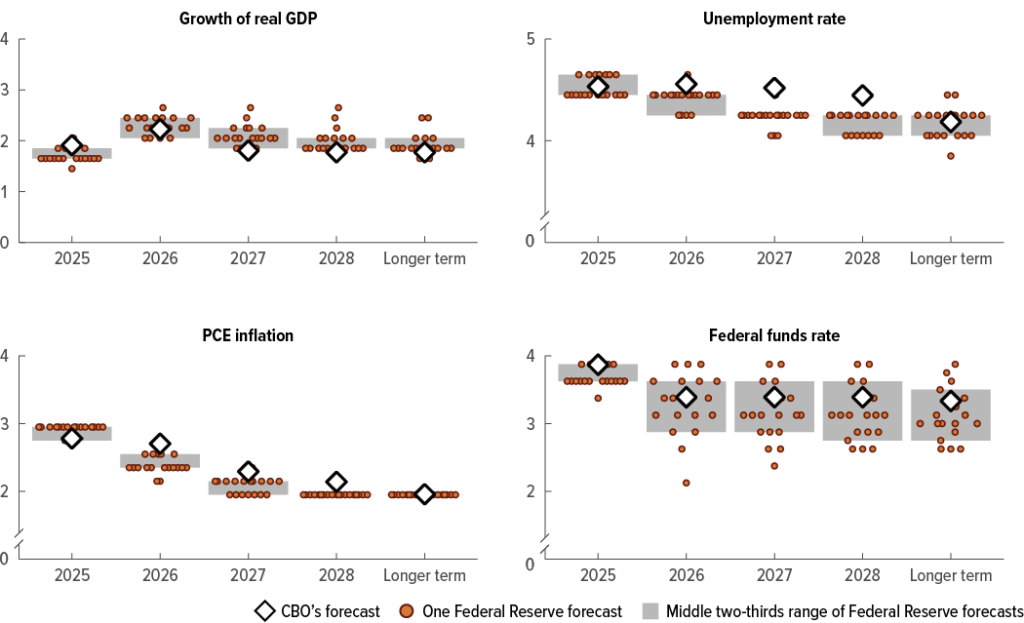

Economic Projections (SEP)

One of the most important releases from the FOMC is the Summary of Economic Projections (SEP), which accompanies four meetings per year (typically in March, June, September, and December).

The SEP includes:

- GDP Growth forecasts

- Unemployment rate projections

- Inflation projections (both overall and core measures)

- Federal Funds Rate forecasts (expressed in the “dot plot”)

By providing these forecasts, the Fed offers transparency about where its voting members expect the economy to be in the near future. Investors, businesses, and economists use the SEP to anticipate future rate moves based on evolving economic conditions.

For example, the December 2025 SEP showed a median projection that many Fed officials expect inflation to move closer to the 2% long-run target over the next couple of years without requiring additional aggressive rate hikes. This type of guidance influences how traders price interest rate–sensitive assets.

Dot Plot — What It Is and How to Read It

The “Dot Plot” is arguably the most widely analyzed part of the SEP.

What the Dot Plot Shows:

Each dot represents an individual FOMC participant’s view of where the Federal Funds Rate should be at the end of each calendar year and at the long-run equilibrium.

- Each participant places a dot on a chart for each year ahead.

- The median of the dots is often used as the market’s expected path of interest rates.

Why It Matters:

The Dot Plot translates policymakers’ expectations into a visual forecast. Unlike a formal policy decision, it reflects opinions about where rates should go under current economic conditions.

For example:

- If many dots cluster above the current rate, it suggests the committee expects future rate hikes.

- If most dots cluster below, it suggests future rate cuts.

- A mostly horizontal cluster suggests rates may remain steady.

2025–2026 Dot Plot Insight:

In the most recent Dot Plot, the median projection indicated that many policymakers expect the Federal Funds Rate to stay near current levels through 2026, with gradual adjustments dependent on incoming economic data — especially inflation and labor market trends.

This doesn’t guarantee future decisions, but it offers guidance on how policymakers think about the future path of rates.

Putting It All Together

Here’s how the decision process unfolds:

- Before the Meeting:

• Staff economists and regional Fed banks prepare detailed economic reports.

• The Beige Book — a compilation of regional economic conditions — is distributed.

• FOMC members review inflation, GDP growth, jobs, and financial stability data. - During the Meeting:

• Policymakers discuss economic conditions and downside/upside risks.

• They debate whether the data support hiking, cutting, or holding rates.

• They consider global economic developments (e.g., energy prices, trade policy, financial stress). - Decision and Communication:

• The policy statement is released, outlining the decision and economic reasoning.

• Four times per year, the SEP and Dot Plot accompany the statement.

• The Fed Chair holds a press conference to explain the decision.

Why This Matters for Markets and Businesses

Every part of this process — from the meeting schedule to the Dot Plot — influences expectations in financial markets:

- Stock markets react to perceived future rate paths.

- Bond markets adjust yields based on expected interest rates.

- Currency markets (USD) move with global rate differentials.

- Businesses and consumers adapt plans based on economic guidance.

By understanding how the FOMC decides on rate hikes or cuts, your readers will better interpret Fed decisions and anticipate their impact on borrowing costs, investment decisions, and economic growth.

2.3 Rate Hikes vs Rate Cuts: What They Signal

One of the most important ways the Federal Reserve communicates its views on the economy is through changes in the Federal Funds Rate. When the Federal Open Market Committee (FOMC) raises or cuts rates, it is signaling its assessment of economic conditions — particularly inflation, job markets, and financial stability.

Below is a detailed explanation of what rate hikes and cuts typically signal, why they are used, and how real economic data supports these interpretations.

Inflation Control — Why Rate Hikes Are Used

Rate hikes — increases in the Federal Funds Rate — are primarily used when inflation is rising faster than the Federal Reserve considers healthy for the economy.

What Higher Rates Do

When the Fed raises interest rates:

- Borrowing becomes more expensive for consumers and businesses

- Consumer spending slows (e.g., fewer big-ticket purchases like homes and cars)

- Business investment slows due to higher loan costs

- Demand in the economy decreases, which reduces price pressures

Higher interest rates generally cool economic activity, which in turn helps control rising prices.

Real Data: Inflation Context

For much of 2022–2024, the U.S. experienced inflation well above the Federal Reserve’s 2% target. At its peak in mid-2022:

- CPI inflation reached 9.1% year-over-year (June 2022)

- Core CPI (excluding food and energy) topped 6.0%+

These elevated inflation rates prompted the Fed to raise rates aggressively, moving the Federal Funds Rate from near 0% in early 2022 to a range above 5.00% by early 2023.

By late 2025 and early 2026:

- PCE inflation eased but remained above target at ~2.8% y/y, showing inflation pressures were still present but moderating.

- Core inflation measures similarly stayed above 2%.

Rate hikes in this environment signaled the Fed’s commitment to controlling inflation even as prices began to slow. Markets interpreted these hikes as necessary to anchor inflation expectations.

Signal Summary:

Rate hikes signal the Fed is prioritizing inflation control.

Economic Slowdown Support — Why Rate Cuts Are Used

Interest rate cuts — reductions in the Federal Funds Rate — are used when economic growth slows significantly, unemployment rises, or financial stress threatens broader economic activity.

What Lower Rates Do

When the Fed cuts interest rates:

- Borrowing becomes cheaper (encourages consumer and business loans)

- Mortgage and auto loan rates typically fall

- Investment becomes more attractive

- Liquidity increases in financial markets

These conditions support economic activity by making credit more accessible and affordable.

Real Data: Growth and Slowdown Indicators

Economic slowdowns often feature:

- Declining GDP growth

- Rising unemployment

- Falling consumer spending

During the 2008 financial crisis, the Fed quickly cut rates to near 0% to combat severe contraction.

Similarly, in March 2020, the Fed cut rates aggressively as COVID-19 economic shutdowns stalled growth, bringing the Federal Funds Rate down to the 0%–0.25% range.

Signal Summary:

Rate cuts signal the Fed is trying to support the economy amid slowing growth or recession risks.

Financial Stability Concerns — The Third Signal

In addition to inflation and growth, rate decisions can also reflect concerns about financial stability — that is, the health and smooth functioning of financial markets.

Elevated Financial Risk

Sometimes the Fed may adjust policy not strictly because of inflation or GDP data, but to prevent or respond to market disruptions.

For example:

- Market volatility spikes (e.g., stock markets plunging)

- Credit markets freeze (banks reluctant to lend)

- Liquidity dries up in key markets

During the 2008 crisis and in the early pandemic period, the Fed didn’t just cut rates — it took extraordinary measures (like quantitative easing and emergency lending) to stabilize markets.

Rate decisions in this context signal that policymakers are concerned about instability that could spill over into the real economy.

Signal Summary:

Policy moves due to financial stability concerns indicate the Fed is acting to prevent systemic risk.

Putting It All Together — Signals and Market Interpretation

| Policy Action | Primary Signal | Typical Economic Context |

|---|---|---|

| Rate Hikes | Inflation control | Rising prices above target |

| Rate Cuts | Economic support | Slowing growth, recession risk |

| Policy Adjustments for Stability | Financial market health | Market stress, liquidity concerns |

Market Reaction to These Signals

Financial markets interpret Fed policy not just on the basis of the rate level, but on what the rate signal suggests about future economic conditions:

- Equities tend to perform better when rate cuts are anticipated because cheaper borrowing supports corporate earnings.

- Bonds may rally (yields fall) when cuts are expected.

- The U.S. dollar often strengthens on rate hikes (higher rates attract foreign capital) and weakens on cuts.

2.4 Historical Interest Rate Cycles (Data Section)

To understand why the Federal Reserve sets interest rates where it does today, it helps to look back at key historical cycles where monetary policy played a pivotal role in steering the U.S. economy. Below are four major monetary policy eras, with real data showing how aggressively the Fed responded to economic conditions.

1. 1980s Inflation Fight

In the late 1970s and early 1980s, the United States faced double-digit inflation, eroding purchasing power and undermining economic stability. To bring inflation under control, the Fed — led by Chairman Paul Volcker — raised the Federal Funds Rate to historically high levels.

Key Facts:

- Peak Federal Funds Rate: ~20% (June 1981)

- Inflation (CPI) exceeded 13% in 1979–1980

- The high interest rates led to two short recessions (1980 and 1981–1982), but successfully broke the back of runaway inflation.

This period is the gold standard for a dramatic inflation-fighting strategy. By accepting short-term economic pain (recessions), the Fed restored price stability that underpinned long-term growth.

2. 2008 Financial Crisis

The global financial crisis of 2007–2008 led to one of the most severe economic downturns since the Great Depression. Mortgage defaults, bank failures, and collapsing markets pushed the Federal Reserve to slash interest rates and introduce unconventional policy tools.

Key Facts:

- Peak Federal Funds Rate prior to crisis: 5.25% (mid-2007)

- Fed cut to 0.00%–0.25% by December 2008

- Introduced Quantitative Easing (QE) — large-scale asset purchases of Treasury and mortgage-backed securities.

The near-zero rate policy stayed in place for several years as the Fed worked to support a fragile recovery. This era marked the beginning of unconventional central bank tools in modern monetary policy.

3. 2020 Pandemic Response

As COVID-19 spread in early 2020, economic activity plunged due to lockdowns, job losses, and supply disruptions.

The Fed acted quickly to cushion the blow.

Key Facts:

- Federal Funds Rate cut from 1.75% to 0.00%–0.25% in March 2020

- Unemployment spiked to 14.8% in April 2020 (the highest since the Great Depression)

- Fed launched massive QE programs, purchasing trillions of dollars in Treasury and mortgage-backed securities to support liquidity.

This response helped stabilize markets and provided breathing room for fiscal stimulus to work.

4. 2022–2024 Inflation Tightening Cycle

Following the pandemic, supply chain disruptions, fiscal stimulus, and strong consumer demand pushed inflation well above target.

From early 2022, the Federal Reserve began one of the most aggressive rate-hike cycles in decades to quell inflation.

Key Facts:

- Federal Funds Rate (start of 2022): 0.00%–0.25%

- Peak Federal Funds Rate (2023–2024): 5.25%–5.50%

- Inflation (CPI) hit 9.1% year-over-year in June 2022, the highest in 40 years

- By late 2025, inflation had eased but remained above target (PCE ~2.8%)

This tightening cycle was designed to slow demand, re-anchor inflation expectations, and bring price growth closer to the Fed’s 2% goal.

Comparing Peak Federal Funds Rates by Cycle

For easy comparison, use the following table to show how dramatic rate shifts have been across major economic cycles:

| Policy Cycle | Peak Federal Funds Rate | Reason for Policy Action | Outcome / Context |

|---|---|---|---|

| 1980s Inflation Fight | ~20% (1981) | Break double-digit inflation | Inflation fell; deep recessions |

| Pre-2008 / Financial Crisis | 5.25% (2007) | Normal monetary stance pre-crisis | Crisis triggered near-zero cuts |

| 2008 Crisis & Recovery | 0.00%–0.25% (2008–2015) | Combat financial meltdown | Supported recovery, low rates persisted |

| 2020 Pandemic Response | 0.00%–0.25% (2020) | Halt economic collapse | QE + fiscal support |

| 2022–2024 Tightening Cycle | 5.25%–5.50% | Fight post-pandemic inflation | Inflation fell towards target |

What This Tells Us

- 1980s: High-rate discipline was necessary to restore price stability.

- 2008: Zero rates and QE were needed to prevent systemic collapse.

- 2020: Swift easing stabilized markets during unprecedented shutdowns.

- 2022–2024: A rapid rate-hiking cycle was employed to manage inflation.

These historical comparisons help readers understand that interest rate policy is not static — it adapts to the greatest economic challenges of each era. Using real data clarifies the trends and reinforces why the Fed’s current policy stance matters.

2.5 Real Interest Rates vs Nominal Rates

When discussing interest rates, economists and policymakers distinguish between nominal rates and real rates.

Understanding this distinction is essential because real interest rates reflect the true cost of borrowing after adjusting for inflation, which is often more meaningful for businesses, consumers, and investors.

1. Nominal Interest Rates — The Face Value

Nominal interest rates are the rates you see quoted publicly — such as the Federal Funds Rate, mortgage rates, or bond yields. These rates do not account for inflation.

For example:

- The current Federal Funds Rate target range in 2026 is 3.50%–3.75%.

- A 30-year fixed mortgage rate might be around 6.5%–7% (varies weekly with market conditions).

These are nominal figures — the stated rates without adjustment for the changing value of money over time.

2. Real Interest Rates — Adjusting for Inflation

Real interest rates are calculated by subtracting inflation from nominal interest rates. This tells you the true purchasing power cost of borrowing or the actual return on an investment after inflation erodes value.

Formula:

Real Interest Rate = Nominal Interest Rate − Inflation Rate

Example with Real Data (2026 Context):

- Nominal Federal Funds Rate (mid-2026): ~3.60%

- Inflation (PCE, Fed’s preferred measure): ~2.8%

- Real Fed Funds Rate ≈ 3.60% − 2.80% = 0.80%

This means that after adjusting for inflation, the actual cost of holding cash or short-term assets is closer to 0.8% in real terms, not the 3.6% face value.

3. Why Real Rates Matter More Than Nominal Rates

Real rates offer a clearer picture of monetary policy’s stance and its effect on economic behavior:

A. True Cost of Borrowing

Borrowers make decisions based on real costs.

If inflation is high, even moderately high nominal rates may feel cheap in real terms.

Example:

- A business may view a nominal rate of 6.5% on a loan as expensive — but if inflation is 4%, the real rate is just 2.5%, which might still encourage investment.

B. Investment Decisions

Investors look at real returns to evaluate whether an investment actually earns money above inflation.

Example:

- A bond yielding 5% with inflation at 3% generates a real return of 2%.

C. Monetary Policy Implications

Central bankers focus heavily on real rates because they reflect the tightness or ease of monetary policy.

- When real rates are positive and rising, monetary policy is relatively tight — borrowing is expensive in inflation-adjusted terms.

- When real rates are negative or low, monetary policy is accommodative — encouraging borrowing and spending.

D. Economic Growth and Savings Behavior

Real rates influence savings vs. spending decisions:

- Higher real rates encourage saving and reduce spending.

- Lower or negative real rates discourage saving and stimulate consumption.

4. Historical Real Rate Context

Looking at real rates over time helps illustrate economic cycles:

| Era | Nominal Rate (Fed Funds) | Inflation Rate | Real Rate |

|---|---|---|---|

| 1981 Inflation Fight | ~20% | ~12% | ~8% |

| 2008 Crisis Era | 0.25% | ~3% | −2.75% |

| 2020 Pandemic | 0.25% | ~1.4% | −1.15% |

| 2026 Context | ~3.60% | ~2.8% | ~0.80% |

This table shows:

- Real rates were extremely high in the early 1980s — a deliberate choice to combat severe inflation.

- During crisis periods (2008, 2020), real rates were negative, stimulating economic activity by making borrowing cheap in inflation-adjusted terms.

- In 2026, real rates are positive but relatively moderate — signaling a balanced stance where inflation is being addressed without excessively tightening financial conditions.

3. Why the Fed Changes Policy (Economic Reasoning Behind Decisions)

3.1 Controlling Inflation

Inflation — the general rise in prices of goods and services over time — is one of the Federal Reserve’s most important policy targets. The Federal Reserve aims for a long-run inflation rate of 2 percent, a level seen as consistent with price stability and sustainable economic growth. To understand how the Fed fights inflation, it’s critical to explore what causes inflation, the difference between headline and core measures, and why inflation expectations matter.

Causes of Inflation: Demand vs. Supply

Inflation can be driven by two broad forces: demand-pull and cost-push (supply-side) inflation.

1. Demand-Pull Inflation

Demand-pull inflation occurs when aggregate demand in the economy outpaces aggregate supply. Simply put, when consumers, businesses, and governments want more goods and services than the economy can produce at full capacity, prices rise.

Examples of demand-pull drivers:

- Strong consumer spending

- Government fiscal stimulus

- Filling labor shortages

- Rapid credit growth

Real Data Context:

In 2021–2022, the U.S. economy experienced unusually strong demand as:

- COVID-19 restrictions eased

- Fiscal stimulus packages exceeded $5 trillion combined

- Consumer spending rebounded rapidly

This surge in demand contributed to high inflation, with CPI hitting 9.1% year-over-year in June 2022 — the highest in over 40 years.

2. Cost-Push (Supply-Side) Inflation

Cost-push inflation happens when the cost of production rises, and producers pass that cost onto consumers. These pressures can come from:

- Rising energy prices

- Supply chain bottlenecks

- Labor shortages

- Import price increases (tariffs, exchange rate shifts)

Real Data Context:

In 2021–2022, global supply chain disruptions, semiconductor shortages, and elevated shipping costs contributed to price pressures even as supply struggled to keep up with demand.

Core vs. Headline Inflation

Understanding the difference between core and headline inflation helps explain how policymakers interpret price pressures.

Headline Inflation

This measures the overall rate of inflation, including all consumer prices — food, energy, housing, transportation, medical care, and more.

- Headline inflation can be volatile because energy and food prices move frequently.

- For example, a sudden spike in gasoline prices can push headline CPI higher even if other prices are stable.

Core Inflation

Core inflation excludes food and energy because their prices often fluctuate due to short-term supply shocks unrelated to broader economic trends.

Why this matters:

- Core inflation offers a clearer view of underlying inflation pressures.

- Policymakers watch core measures to distinguish between temporary price movements and systemic inflation.

Real Data Comparison (Dec 2025)

- Headline CPI: ~3.4% y/y

- Core CPI: ~3.7% y/y

This indicates that even after removing volatile food and energy costs, underlying price pressures remained robust.

Inflation Expectations

Inflation expectations are how households, businesses, and markets anticipate future inflation. These expectations influence real economic behavior:

- If consumers expect prices to rise faster, they may spend more today, increasing demand and fueling further inflation.

- If businesses expect higher input costs, they may raise prices pre-emptively.

The Federal Reserve pays close attention to inflation expectations as a leading indicator:

Market-Based Measures:

5-Year, 5-Year Forward Inflation Expectation Rate (derived from Treasury Inflation-Protected Securities – TIPS)

- Recently, this measure has hovered near 2.3%–2.4%, indicating markets expect inflation to moderate close to the Fed’s long-run target.

Survey Measures:

University of Michigan Consumer Sentiment Survey tracks consumer inflation expectations:

- 1-year expectations have varied between 3%–4%, signaling that households still anticipate above-target inflation in the short run.

Stable expectations near the Fed’s 2% target help anchor inflation over the long term because they reduce the incentive for wage–price spirals and aggressive pricing behavior.

Why the Fed Focuses on Inflation

When inflation is persistently above target (e.g., >3% for multiple months), it signals that price pressures may be broadening beyond temporary factors. To address this, the Fed may raise interest rates or tighten monetary conditions to cool economic activity.

Conversely, if inflation falls significantly below the 2% target, it may signal weak demand and potential slow-growth conditions, prompting policy easing.

Real Impact on Policy Decisions

For example:

- 2021–2022: Inflation surged due to demand-pull conditions and supply disruptions. The Fed responded by raising interest rates rapidly to cool demand and slow price increases.

- 2025–2026: Inflation moderated, but core inflation remained above target, signaling underlying pressures that have yet to fully dissipate. This has encouraged policymakers to maintain a cautious stance on rate cuts.

Key Takeaways

- Demand-pull inflation comes from too much demand chasing too few goods.

- Supply-side inflation arises when production costs rise.

- Headline inflation captures all price changes, while core inflation strips out volatile food and energy prices for a more stable trend.

- Inflation expectations shape consumer and business behavior — and influence monetary policy itself.

Understanding these dynamics helps readers grasp why the Fed acts aggressively during inflationary spikes and what metrics it uses to judge whether inflation is temporary or entrenched.

3.2 Preventing Recession

One of the Federal Reserve’s secondary goals is to sustain economic growth and prevent or soften recessions. A recession — a significant decline in economic activity lasting months or more — can trigger rising unemployment, falling incomes, weaker corporate profits, and financial stress. To avoid severe downturns, the Fed watches several leading economic indicators that tend to signal weakening growth before it appears in headline GDP numbers.

Below are the primary indicators the Fed uses — along with current or recent data — to assess recession risk.

Leading Indicators of Economic Slowdown

Leading indicators are economic variables that tend to change before the overall economy begins to contract. They give policymakers and investors early warning signals.

Key leading indicators include:

- Yield Curve

- Consumer Spending Trends

- Business Investment

- Manufacturing Activity

- Labor Market Signals

Among these, two of the most closely watched by the Federal Reserve are yield curve inversion and consumer spending patterns.

Yield Curve Inversion — A Classic Warning Sign

The yield curve plots interest rates across different maturities of U.S. Treasury securities — from short-term bills to long-term bonds.

When the curve is normal, long-term rates are higher than short-term rates. This reflects expectations that the economy will grow and inflation will rise over time.

However, when the yield curve inverts, short-term rates exceed long-term rates — signaling that investors expect weaker growth in the future.

Why It Matters:

Yield curve inversions have historically preceded recessions — sometimes by 6–24 months — making them one of the most reliable recession predictors.

Recent Data (2025–2026):

- In early 2025, the 2-year Treasury yield exceeded the 10-year Treasury yield, creating a slightly inverted yield curve.

- As of late 2025, the 2-year yield traded above the 10-year yield by a narrow margin, suggesting market expectations of slower growth ahead.

For example:

- 2-Year Treasury Yield: ~4.50%

- 10-Year Treasury Yield: ~4.30%

- This inversion reflects investor caution about future growth.

An inverted yield curve suggests that markets are pricing in lower growth or future rate cuts, often before economic data confirms a slowdown.

Consumer Spending Slowdown — A Key Demand Signal

Consumer spending accounts for roughly two-thirds of U.S. Gross Domestic Product (GDP). When consumers slow down on spending — particularly on big-ticket items — it often signals weakening confidence and slower economic growth.

The Fed monitors consumer spending through trends in retail sales, disposable income, credit usage, and service sector activity.

Recent Consumer Spending Trends (2025):

- Retail sales have continued to grow, but at a moderating pace compared with the post-pandemic rebound.

- Recent monthly data showed retail sales growth slowing to around 0.3%–0.4% per month, below the stronger pace seen in earlier economic expansions.

Slower consumer spending growth can indicate that households are becoming cautious — potentially due to higher borrowing costs, inflation pressures, or labor market uncertainty.

Other Leading Indicators the Fed Watches

While yield curve inversion and consumer spending are critical signals, the Fed also watches:

- Manufacturing data (PMI / ISM indices) — contraction can signal broader economic weakness

- Business investment levels — lower investment suggests cautious business confidence

- Jobless claims — increases in weekly unemployment claims can precede broader layoffs

- Building permits and housing starts — a cooling housing market signals weaker economic activity

For example, if the ISM Manufacturing PMI falls below 50, it indicates contraction — a warning bell for broader economic slowdown.

How the Fed Responds to Recession Risks

When multiple leading indicators turn negative, the Federal Reserve may:

- Cut interest rates to make borrowing cheaper

- Increase liquidity in financial markets

- Lower reserve requirements for banks

- Use forward guidance to assure markets of policy support

Rate cuts reduce borrowing costs, stimulate consumer and business spending, and cushion economic slowdowns.

For instance, during the 2020 COVID-19 recession, the Fed cut the Federal Funds Rate to 0.00%–0.25% and implemented large-scale asset purchases to support financial markets and credit flows.

Similarly, during the 2008 Financial Crisis, sharp rate cuts were used in conjunction with quantitative easing to combat severe contraction.

What Recession Signals Tell Policymakers

| Indicator | Signal | Why It Matters |

|---|---|---|

| Yield Curve Inversion | The market expects slower growth | Historically precedes recessions |

| Consumer Spending Slowdown | Falling demand | Reduced GDP growth impact |

| Manufacturing Contraction | Lower output | Signals broader economic weakness |

| Rising Unemployment Claims | Labor market weakening | The market expects slower growth |

3.3 Stabilizing the Financial System

One of the less-visible but critically important responsibilities of the Federal Reserve System is maintaining financial stability. Beyond inflation and employment goals, the Fed must ensure that the U.S. financial system operates smoothly — especially during times of stress. When markets seize up or banks face solvency pressures, the Fed acts to prevent a localized problem from cascading into a full-blown crisis.

Below are the main ways the Fed intervenes when financial stability is threatened: banking stress monitoring, liquidity support, and emergency lending programs — explained with real examples and recent data.

Banking Stress: What It Is and How the Fed Monitors It

Banking stress refers to periods when financial institutions face solvency or liquidity pressure. It can show up as:

- Rising non-performing loans on bank balance sheets

- Sharply declining bank stock prices